Bubble.ai

Bubble.ai

Audio Recording by George Hahn

Note: This newsletter is not investment advice.

Five years ago, Nvidia was a second-tier semiconductor company known for giving Call of Duty better resolution. Today it’s the third-most-valuable company on Earth, with a dominant 80% share in AI chips, the processers underpinning the largest, fastest creation of value in history ($8 trillion). Since fellow AI supernova OpenAI released ChatGPT in October 2022, Nvidia’s value has increased by $2 trillion, or about the value of Amazon. This week, Nvidia reported monster quarterly earnings — its core business, selling chips to data centers, was up 427% year over year.

Last year, at Cannes, Jensen Huang introduced himself to me and said “I love your videos.” Not recognizing him, I asked if he’d like a photo. He said yes, we took the snap, and I kept walking. Since then, his company has added $1.3 trillion in value. I did Ketamine therapy, stopped drinking for 17 days, and installed a router with only the help of YouTube. It’s been a big year for both of us.

There is near-universal agreement on the AI market’s revolutionary potential, a historic consensus that explains the upward trajectory of AI stocks. In sum, everyone is barking up the same tree … which makes us stupid. It also inspires a question: Are we in a bubble?

Bubble Psychology

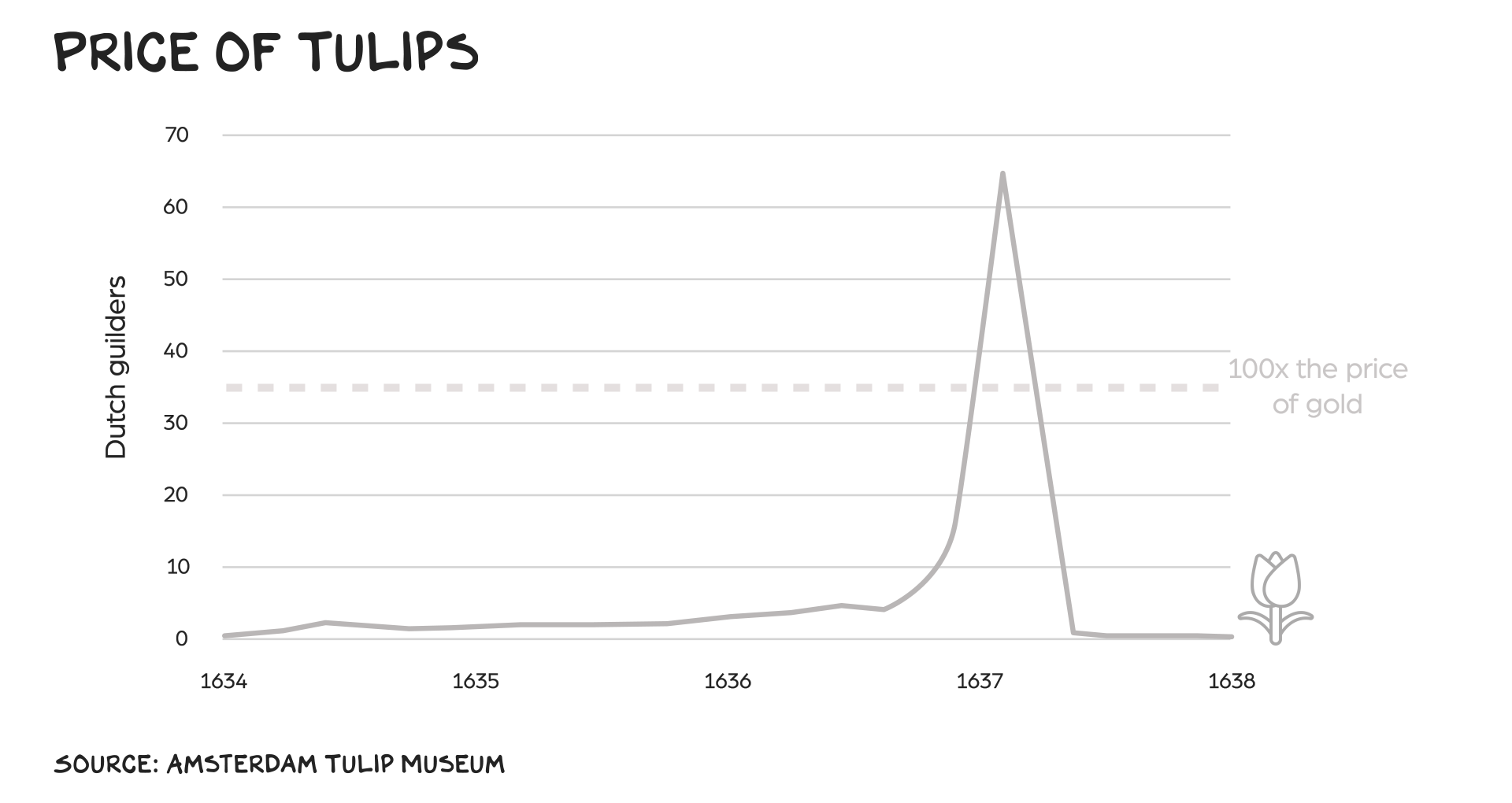

In the 1630s, tulips were not getting any prettier or more useful, but people bid them up because they believed they’d be able to sell them to someone else at an even higher price. Aka the “greater fool” theory. Meme stocks could best be defined as the greatest fool theory, as many buyers are convinced they are part of a movement. Pro tip: If someone tells you to “stick it to the man,” you are usually the stick. These kinds of bubbles are fragile, and they rarely get large in terms of the broader economy or last very long.

Bubbleicious

Multitrillion-dollar, economy-distorting bubbles occur when pure bubble psychology overlaps with real economic potential. This manifests as a self-propulsion machine — stock price increases validate assumptions and encourage more aggressive projections, which draws more speculators, who don’t want to miss out, and so on, and so on. Exogenous factors including low interest rates (i.e. cheap money) can fuel them, but bubbles typically have an economic growth engine and an enduring technology at their core:

- The dot-com bubble of the late 90s was predicated on a thesis that proved out: The internet was the most transformative technology of this millennium, poised to create unprecedented value. That did happen, and several of the companies that appeared wildly overvalued turned out to have been bargains.

- The housing market bubble of the 2000s was a function of low interest rates, financialization, and other external factors, but under all that was a correct thesis: Land is finite, houses are essential, and we don’t have enough of them. Nearly two decades later, we still don’t.

- Crypto was a bubble largely fueled by psychological nonsense — the Bored Apes should have been called Bored Tulips. But blockchain technology made a case for providing real benefit, and the resilience of Bitcoin indicates it likely will endure as a store of value.

The Bubble This Time

The financial media will digress to one of its favorite games, “Is this a bubble or is AI for real?” The answer is yes. AI’s economic promise feels real, obvious even. And that is what makes a bubble inevitable. Bubbles emerge in unexpected ways, for unpredictable reasons. Big bubbles inflate in similar ways. A transformative innovation emerges, capital rushes in, valuations increase, speculators add fuel, the atmosphere heats, the bubble grows, the cheap capital supercharges growth, and the wheel turns.

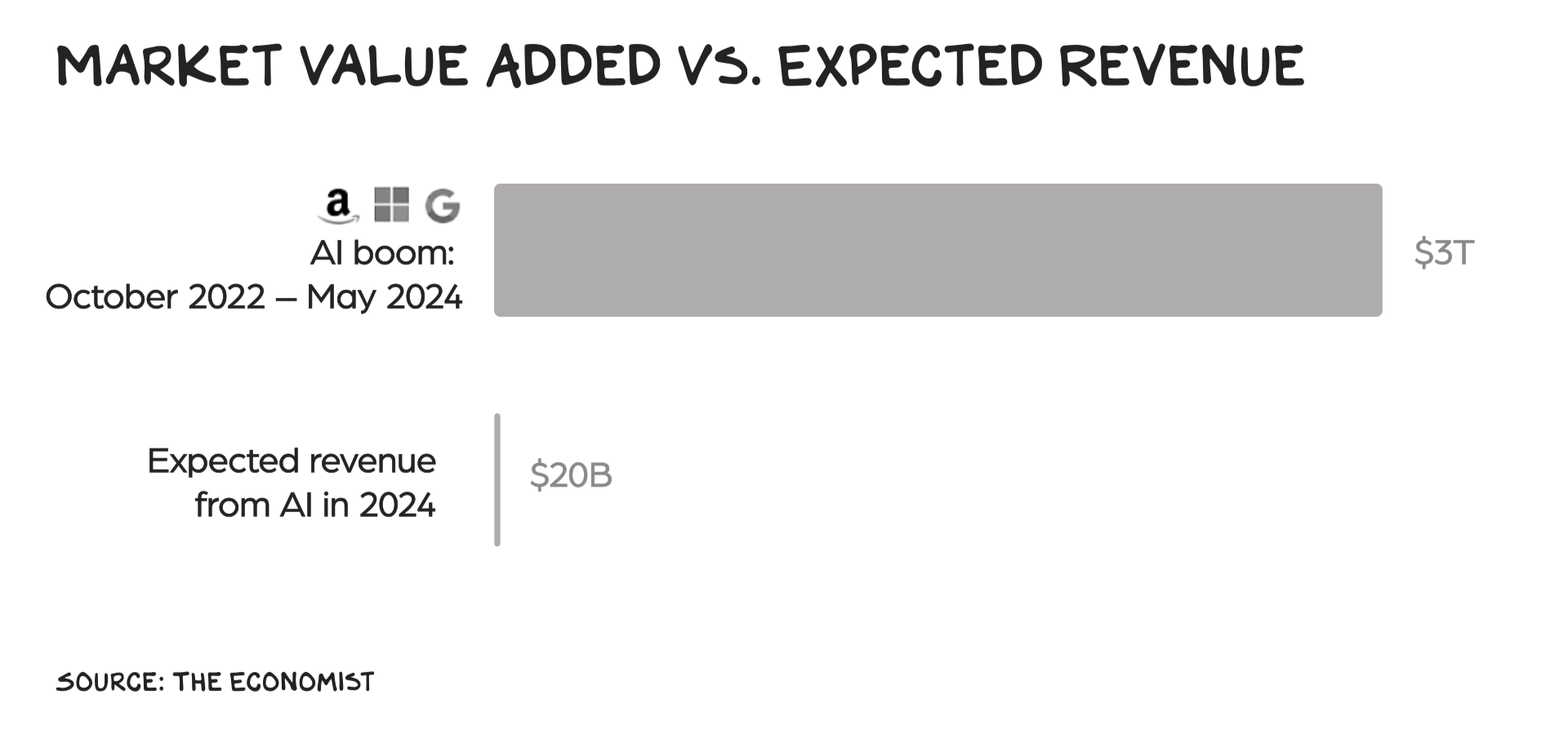

Of course we are in a bubble now — how could we not be after the mind-blowing debut of ChatGPT? AI is amazing, but the bubble-multiplier effect is very much in play. According to the Economist:

The combined market value of Alphabet, Amazon, and Microsoft has jumped by $2.5trn during the ai boom. [This value creation] is 120 times the $20bn in revenue that generative AI is forecast to add to the cloud giants’ sales in 2024.

That was in March. Now it’s $3 trillion. So the market is valuing AI revenue at 150x. Pre-AI, Microsoft was valued at about 10x revenue, Alphabet at 5x, and Amazon at around 4x. Growing into this AI multiple will require these businesses to find another $500 billion in annual revenue among them, in addition to continued expansion of their non-AI business, the equivalent of adding more than Alphabet’s revenue.

The darling of AI, Nvidia, has been painted into a corner of good problems. But, nonetheless, a corner. NYU prof Aswath Damodaran has calculated that Nvidia, to justify its valuation, will need not only to continue to dominate the market for AI chips, forecasted to grow aggressively, but also to dominate another market of similar scale. Think about this: Built into the price of Nvidia is the expectation the company will find another market as big as AI, and achieve similar dominance.

At the peak of the dot-com bubble, Google was a newcomer with the second-most-popular search engine, and Meta didn’t exist. Today hundreds of AI startups aim to replicate that sort of success. One prominent VC tracks 1,400 AI startups, even in a tight VC investment climate. As the IPO pipeline widens, more firms will emerge … and submerge. Many will fail — it’s a bubble — but not all.

There are two important questions regarding AI, and neither is “are we in a bubble?” We are. The important questions are “when will it pop” and “who will endure?”

Get Rich Quick

Timing a bubble’s pop correctly is likely the fastest way to become a billionaire, as the move in your direction, and the leverage on capital, is violent. John Paulson’s hedge fund made $15 billion timing the housing bubble in 2007 (including $4 billion for himself); Michael Burry made a few hundred million and had a movie made about him, The Big Short. But timing is everything, and aggressive short positions can also pop. Burry shorted Tesla in 2020, only to watch it double before unloading his short … at the peak. George Soros took “whopping losses” shorting the dot-com market in 1999. Legendary investor Julian Robertson turned $8 million into $22 billion before he, too, bet against the dot-com bubble … and gave up on his play a month before it popped. Showing up early sunk Tiger Management. If that name sounds familiar, it’s because Robertson subsequently staked Tiger Global, which suffered from PTSD — the firm lost $60 billion staying long on tech in 2022. The lesson(s) from investing history all point to one thing: Nobody has any idea. The way to get rich is slowly, buying the whole haystack via low-cost ETFs. But I digress.

Public Service Announcement: Nobody knows what will happen — you should diversify and not try to time the market.

If I knew when the AI bubble was going to detonate, I wouldn’t be discussing it here but selling everything to buy deeply out-of-the-money put options in MSFT, NVDA, and other AI stocks, cash out after the crash, and buy Australia. Alas, I’m more confident about how, vs. when, the pop will play out.

Airpocket

Airplanes follow flight patterns, calculated to maximize safety and passenger comfort while minimizing fuel use. Atmosphere is not a static medium, however, and sometimes planes encounter localized areas of rapid air movement, aka turbulence. A sudden downdraft can cause a plane to drop hundreds or thousands of feet in seconds, an event known as hitting an air pocket. Most are harmless, but strong downdrafts can be terrifying and dangerous. Just this week, a Singapore Air 777 dropped so sharply that one passenger was killed and six more sent to the hospital.

Modern airplanes recover from hitting an air pocket in seconds, but frothy markets take longer to find their footing. Here’s one scenario: A major non-tech company (e.g., Walmart, JPM, Procter & Gamble) will announce it is paring back on its AI initiatives. Shuttering its AI team, calling off a joint venture, etc. “We remain optimistic about the long-term impact of AI on our business, but we are not seeing the ROI initially projected and are scaling back our level of capital investment in this technology.” The same cycle that drove prices up will pare them, only faster: Analysts will identify which AI players were selling to the company, and every CEO on every earnings call that week will be asked if they’re cutting back their AI spend. Trend reversals travel through earnings calls like cold viruses through kindergartens, and by the end of the month, no CEO will want to be on the last helicopter out of AI Saigon. AI stocks will decline, and once they do, speculators will begin selling, creating a stampede for the exits. Trillions of dollars in market cap erased in weeks. Someone will time it perfectly. Most won’t.

The air pocket that popped the dot-com bubble blew in from the east. On Friday, March 10, 2000, the Nasdaq hit 5,049. The next Monday, Japanese economic data showed the country’s economy had contracted in the fourth quarter of 1999, and the bad news was enough to spook the speculative market. The day’s downdraft hammered the Nasdaq to its fourth-biggest point loss ever. It wouldn’t break 5,000 again for 15 years. The housing bubble hit its own air pocket seven years later, in March 2007, when mortgage lender New Century Financial collapsed. The market’s momentum continued for a few months but peaked in October before spiraling toward Earth.

Bubble Blast

The collapse of a major bubble can have far-reaching effects. The collapse of the housing bubble in 2007 spread into the banking system in 2008 and threatened the global economy — if you’re between the ages of 16 and 94, that will, hopefully, be the most significant financial event of your lifetime.

We. Hope.

The dot-com meltdown mostly hurt people who could afford it, who’d taken an eyes-wide-open risk. I knew a lot of them — 100 of them worked for me. We called half of them into a conference room and laid them off, which still nauseates me when I think about it. The sin was hiring them in the first place — zealous hiring is a hallmark of bubble economics, both a symptom and a cause in the self-reinforcing cycle of bubbles. They were (mostly) great people, but we’d bought the same trope as everyone else: If you hire them, it (revenue) will come. The same was true all over the Valley and in the mini-Valleys that had sprung up in the bubble (Silicon Alley in NYC, Silicon Forest in Seattle — there were even a few Silicon Prairies). As in every Patagonia vest recession, most of those who were laid off are highly educated, employable young people who went on to other opportunities. There were second-order effects as well. There was a mild recession in 2000, which was bad especially for people entering the workforce or hoping to retire, and telco firms that had banked on never-ending broadband expansion got crushed. The broader market decline pushed companies with heavy pension obligations into bankruptcy.

Right now, it feels like the AI bubble is more in dot-com territory than housing-crisis country. But the bigger it gets, the more leveraged we become, and the larger the blast radius. It would be healthy if some of the air came out in 2024, but Nvidia’s monster quarter will likely keep inflating the sector.

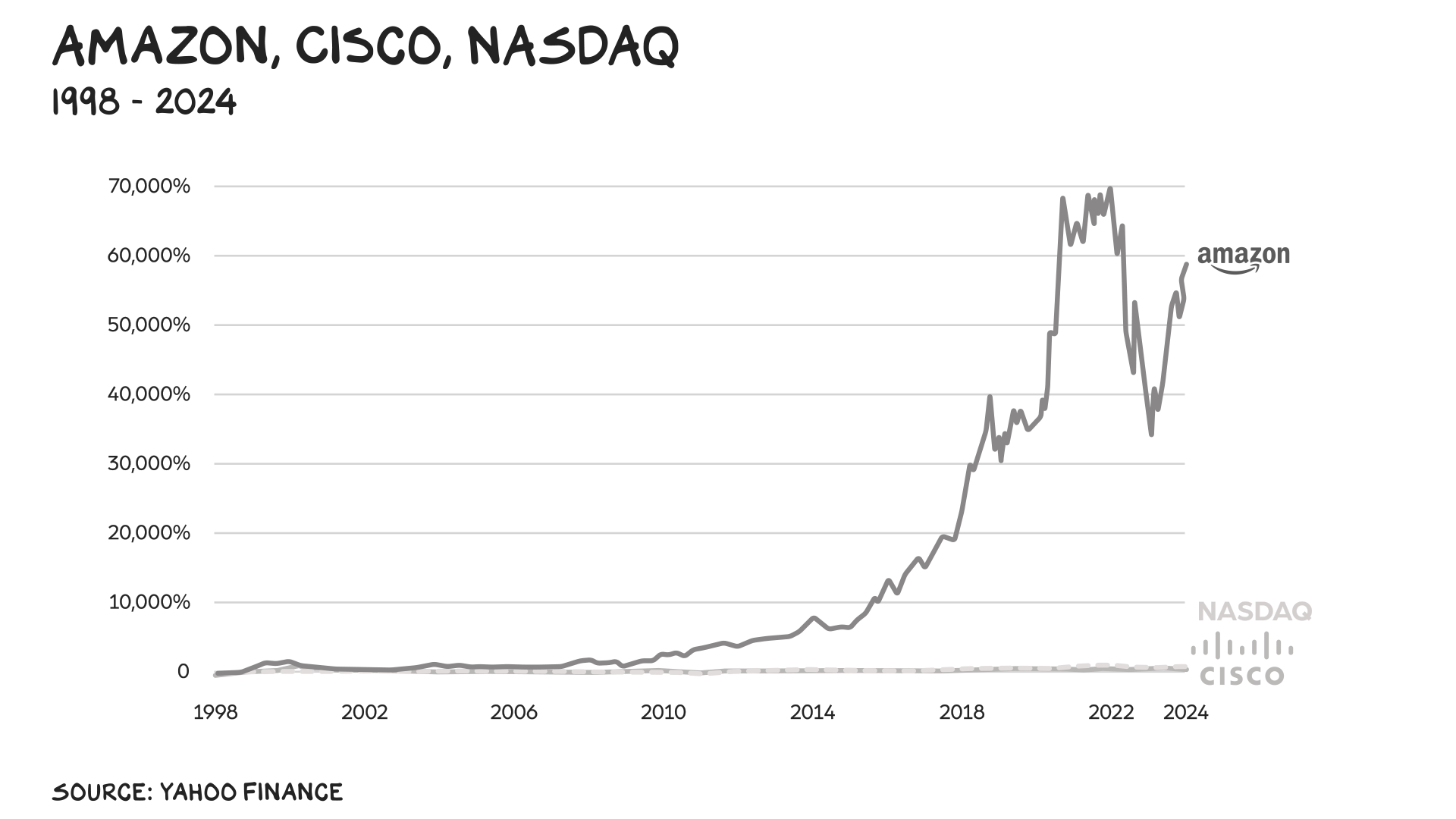

Cisco

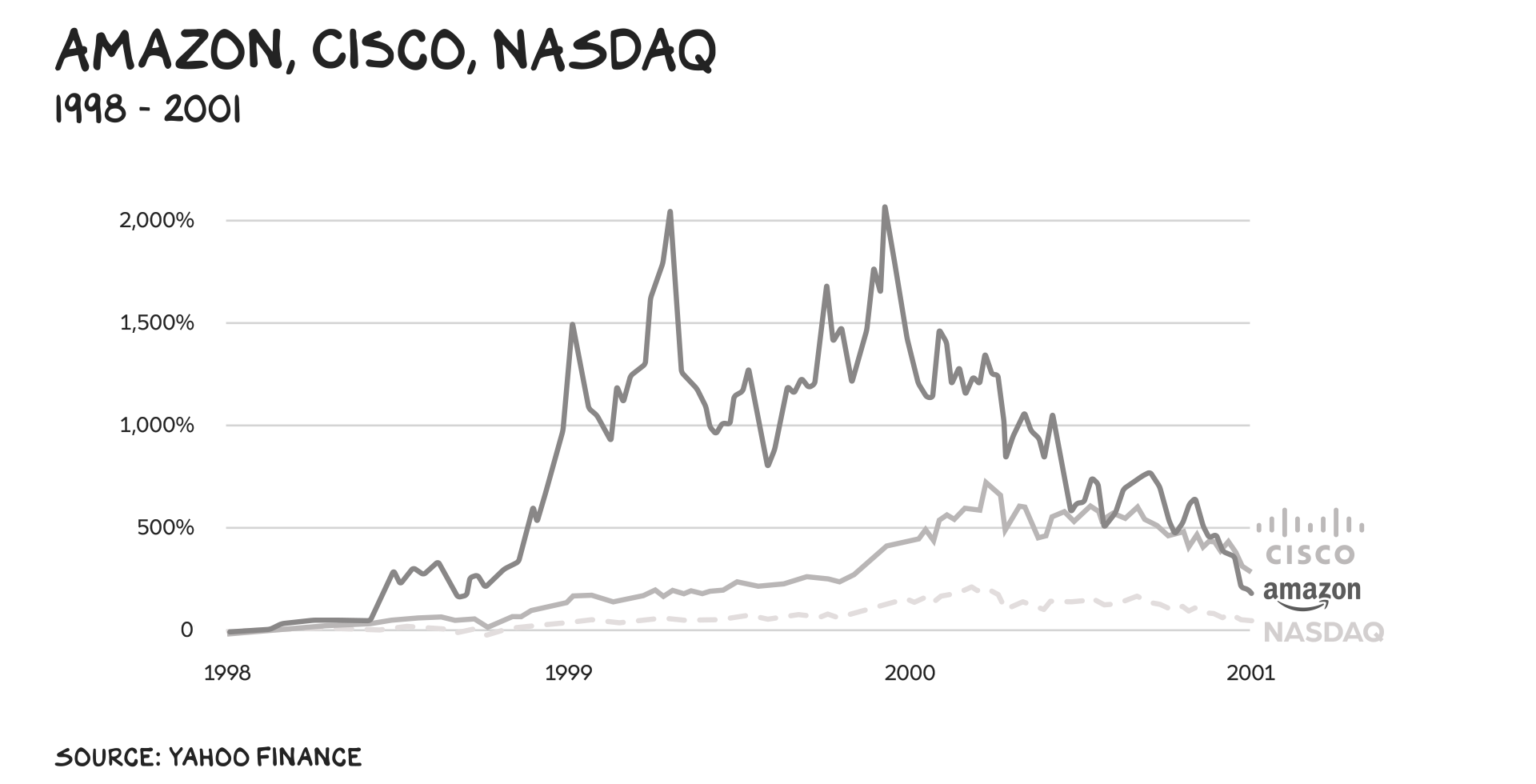

Timing the bubble’s end is less interesting than looking past it. If AI is half the technological breakthrough it feels like, it’s going to sustain long-term value creation … but where? One aspect of this bubble that’s caught my attention recently is how similar the narrative we hear today about Nvidia is to what people said about Cisco during the dot-com runup. Cisco is/was a hardware company that makes a lot of the gear the internet runs on. In 1999 it was the ultimate “picks and shovels” play, the company every tech fund had to have in its portfolio, and the stock you owned if you considered yourself a serious investor, not a speculator. Let the kids buy Pets.com and Amazon. That’s essentially the narrative on Nvidia today.

Only it turned out there was a lot of that “serious” money, and boring Cisco increased in price 40x between 1995 and 2000. When everything crashed in 2000, Cisco went with it. Though the smart buy took less of a beating than Amazon, and much less than Pets.com, which went out of business that fall.

Long term, Cisco did “OK,” staying in business and beating the Nasdaq through most of the 2000s, though it hasn’t kept pace with Big Tech’s surge since 2020. (Long-term comps to an index like this are rigged against individual stocks, since indexes benefit from survivorship bias.)

Was Cisco a better bet than Amazon? Not even close. In fact, if on March 10, 2000, the peak of the bubble, you’d put a tenth of your money into 10 of the riskiest dot-com stocks rather than Cisco, you would still have outperformed Cisco (and the broader market) by over 15x, as long as one of those risky stocks was Amazon.

Pop

There are plenty of differences between dot-com and AI, and between Cisco and Nvidia. For one, Nvidia’s runup has been fueled by spectacular earnings growth as well as hype, while Cisco benefitted from the time-limited Y2K investment boom. But when the “safe choice” is one of the frothiest stocks, we are a) in a bubble, and b) no longer playing it safe. The market is not necessarily rational in the short term, but over the long term, risk and return align. If Nvidia is the sure thing in this market, then it will generate sure-thing returns — aka it will track the market. If you’re expecting Amazon circa 1999-2024 returns from Nvidia, then you should also expect Pets.com risk. This is not your pilot speaking, but do buckle up and make sure your tray table is secured.

Life is so rich,

P.S. This week on our new Thursday edition of the Prof G Markets podcast, Josh Brown, co-founder and CEO of Ritholtz Wealth, returned to the show to discuss what’s driving the current bull market. Listen here or watch.

P.P.S. Section’s popular AI Crash Course runs June 10-17. Sign up now and become an AI guru in one week.

23 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

I would like to translate this article into Korean and publish it on an internet media site for readers in Korea, and I am seeking permission to do so.

“Es ist dafür gesorgt dass die Bäume nicht in den Himmel wachsen”

—Johann Wolfgang von Goethe (1749-1832)

This has been quite eye-opening, thank you for that and it has pushed me to do some more research on this .. And now, research studies like this (https://www.techradar.com/computing/artificial-intelligence/hardly-any-of-us-are-using-ai-tools-like-chatgpt-study-says-heres-why) are actually establishing hard facts that people are using AI tools very superficially, and it still is only with early adopters and is yet to climb up the innovation curve.

The sad part is, that the repercussions of this bubble burst will hit an already ailing tech sector hard, which has been at a down curve since the Covid boom with funding drying up in 2023 and numerous layoffs happening all around the planet.

I’m hoping the bubble of extreme hate toward men who haven’t had sex in the past six months that’s been rippling through the online economy will burst.

If there are millions of men who are alone but wouldn’t go see Sydney Sweeney in a tight costume because she’s likely to be abusive to them (she wasn’t, but the concern may have hurt business), a bigotry toward incels that rivals Sun Myung Moon’s hatred is too common. Moon used it to fuel his belief that Jesus Christ turned the crown of God over to him because Jesus was a loser who never got laid.

That’s a belief Republicans shouldn’t have ignored, but Democrats have echoed and spoken his kind of anti-incel hatred.

Recently, I saw a hate-filled thing called Steven Ing ranting about “your incels” in Psychology Today. His publishing Moon-like hate at a pro site shows a rot in psychology.

I am alone, and I’ve been trying to stop an unethical hypnotherapist who came into my brain without my knowledge and won’t leave. That hypnotherapist’s conduct was a lot like brainwashing.

I’ve tried to complain, to no avail, which means that the psychology and hypnotherapy professions are okay with unethical colleagues. That makes hypnotherapy as dangerous as the Moonie cult.

I’ve had lots of people see what the unethical hypnotherapist is doing, and they should have known it was wrong.

Right now, I’m going through a stressful situation, and the unethical hypnotherapist — who shouldn’t be there at all — wants to keep piling on. I’m going to assume that’s what all hypnotherapists and psychologists want to do to all men who are alone — you sneer at us as incels — until the unethical hypnotherapist is no longer in or in the vicinity of my head.

From what I’ve seen, hypnotherapists could abuse anyone. They have an ethics code, but no means of enforcing it. I don’t think anyone else who thought about it would want to risk that kind of bad experience.

From what I’ve read, they only get caught when they commit sex acts on a woman who’s under. I doubt that’s the only crimes of hypnotherapy, but that would be enough to make you think twice about it, if the hypnotherapist let you know it was going in beforehand.

To be clear, the hypnotherapists’ ethics code says that when someone it’s doing this awful hypnotherapy thing to says “No! Stop!”, it stops.

If it doesn’t, the hypnotherapist is unethical, according to its own ethics code.

I don’t know what excuses people have for going along with an unethical hypnotherapist, but there is no excuse, really. It has no excuse, either.

If its colleagues want to let an unethical hypnotherapist continue, perhaps there’s no excuse for hypnotherapy being legal in a society. I can’t think of anything more chaotic and evil than unethical hypnotherapy.

“Since then, his company has added $1.3 trillion in value. I did Ketamine therapy, stopped drinking for 17 days, and installed a router with only the help of YouTube. It’s been a big year for both of us.” – I’m still laughing. Thank you for this.

50 people in a conference room. Big conference room.

Cycles versus bubbles. Tulips go through bubbels, semiconductors go through cycles. Ask Intel, theirs lasted 40 years. Nvidia has shown the world a new way of computing and generating output. Their cycle is just starting and they are going to be printing money for a long time. Eventually Scott will be right, just like a stopped clock.

I’m not sure about that. When so much capital is chasing something, eventually the competitive advantage is “usually” lost, or at least diminished enough that the ability to maintain pricing power goes away. I guess time will tell.

I am one of those between the age of 16 and 94 – saw the Dotcom bubble early in my career and then the financial crisis.

Lived this piece and agree on the potential bubble. But while reading it the question that coming to mind is “why would bubbles repeat again and again?”.

Well written. Food for thought. Probably will save some a lot of money. My approach- stay long and collar (limits upside and downside) until the music stops.

Dot.com or housing crisis? …at a glance, rather dot.com as, from my view, it is not credit driven but rather valuation and less impacting the recovery … now 2 differences with the original dot.com.

– highly leverage investor could multiply its impact (think LTCM^1000)

– I bet western economies had more strengths and growth potential in 2000 than today

Let’s wait & see!

well written.. true before and certainly true today – Every so and then there is a new flavor on the shelves, and in some case a new type of ice cream, the only true constant is that the column of the temple: the chocolate and the vanilla may go our of fashion for s season or two, but then when the crowd turns unsure, it rushes back to their comfort- Above and beyond, the simplest form of advise was dispensed by Mr. Warren Buffet: “The financial market is a system that transfers money from the inpatients to the patients”

I completely agree with the article. Having worked in big tech for 11 years, I understand the technology behind what’s now called AI, particularly generative AI. Essentially, it’s linear algebra marketed as the greatest human invention. Is it useful? Absolutely. Will it help solve many problems? Definitely. But is it the best invention ever? No.

I’m frustrated with companies like NVIDIA for a simple reason: when this bubble pops, people will shift their opinions of AI negatively, which is a shame. This will set back potential improvements, all in the name of greed. Well done, humans.

I think the link in this sentence is incorrect? “One prominent VC tracks 1,400 AI startups..”

I think you are judging the statement , remember this it’s the semantics that counts. Hence, please understand. Many VC firms also tracks many ai startups. But they are highlighting the one they know.

Scott – your comparison is interesting but flawed. In 2000 Cisco made “the plumbing” . Ie they made a commodity. There may be a difference in stainless steel or plastic pipes, but it is small. High-end chips are not a commodity. they have a moat and are hard to design and build ( ask Intel ) . NVIDIA’s run may end, but it’s hard to see until there is a competing product or a significant slow in spending.

Excellent comment.

I’d add to it that Petco risk rules change when you have 80%+ of any market because there are no other choices.

Will other companies jump in to Nvdias space? Yep. But development cycles have to have a working platform to write for and test on. If it’s 3-5 YEARS before a competing untested chip is released to compete with Nvidia then many of the comparisons Scott made fall apart. That said, we are in a bubble. Year 1-2 of a 7 year cycle. Nvidia is making money as the only game in town and it will be until the late 2020’s.

How do you make a small fortune? Start with a really big one. Still early and there ain’t no Wintel on the horizon just yet.

Bubbles…busts…AI…yeah it’s all good. Ketamine rules, stay sober…dollar cost average thy ETFs, go long my son. Scott, I want the Sales Manager job in Glasgow FTA. Living local…they’ll live me.

PJ of the GreenRay

The Economist, what dumb people read in airports to appear smart.

You should (re)read Richard Rumelt good strategy, bad strategy and its chapter on Nvidia. while I may understand that you will call it second tier Co based on market indices, what they solved and cracked was a masterstroke in execution of a genius strategy. and as Jobs said, I wait for the next big thing.