Red Friday

Red Friday

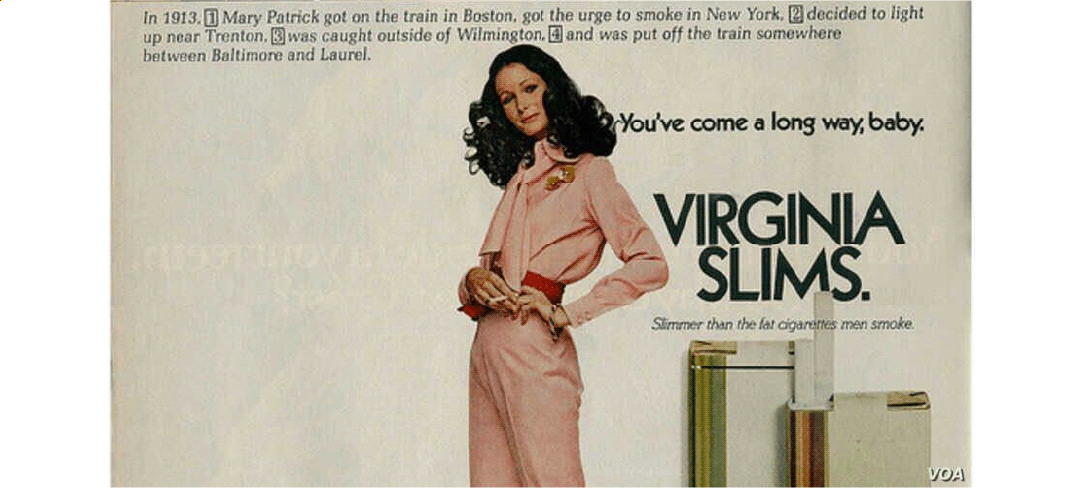

Smoking wasn’t popular among women until Edward Bernays, the father of public relations, rebranded it. In 1929 he capitalized on the feminist movement and repositioned cigarettes with a “torches of freedom” campaign. Bernays hired women to march down Fifth Avenue smoking as a public display of emancipation and rebellion. Within six years, women were purchasing 1 in 5 cigarettes, up from 1 in 20 in 1923.

The strategy is simple: If people associate something negative with your product (e.g., cancer), change the conversation — “You’ve come a long way, baby.”

Facebook’s rebranding to Meta is your mom at Thanksgiving when your brother begins bragging about all the “honk” he was making selling meth in rehab … just ignore all actions and words leading to that point, and change the subject as if the entire natural state has been suspended. Philip Morris and Blackwater are also good at this. New names attempt to divert our attention from teen depression, lung cancer, and murder, respectively.

A low-calorie version of this is unfolding in the payments space. The stale product formerly known as a loan has been rebranded as “Buy Now Pay Later,” or BNPL. The premise is simple: Buy a product for a fraction of its cost at checkout and pay the rest of it off over a few weeks or months. The good news: Debt is not as bad as cancer. Though it can trigger depression and even revolution. But that’s another post.

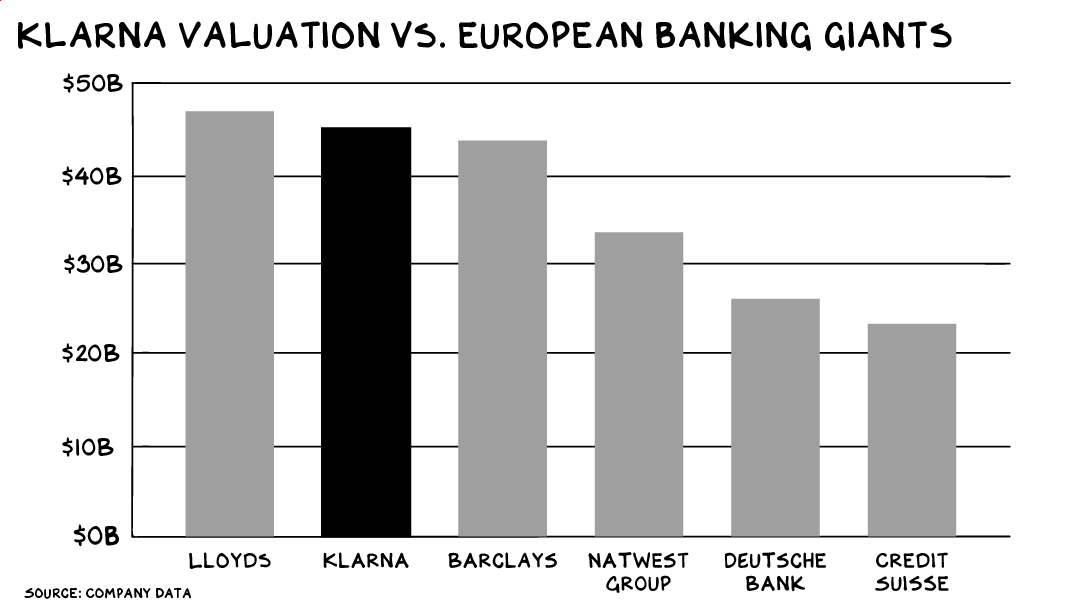

BNPL is one of the hottest trends in finance: 1 in 5 Americans used one of these services in the past year, with U.S. spending on BNPL increasing 230% since 2020. By 2025 global BNPL spending is projected to double to $680 billion. In August, Square acquired BNPL pioneer Afterpay for $29 billion in the largest-ever acquisition of an Australian firm. (We had the Founder/CEO of Afterpay on the Prof G Pod, and he’s an impressive young man.) Swedish BNPL giant Klarna is getting ready for a $50-billion-plus IPO, with a current valuation on par with ING or Lloyds Banking Group.

The target market is young people. Klarna’s frontman is rapper A$AP Rocky (who was paid in equity, not debt) — many BNPL brands rely on social media influencer campaigns. In the U.S., three-quarters of users are Gen Zers or millennials; it’s projected that nearly half of Gen Z will be using BNPL services by 2022. Their attraction to BNPL coincides with an aversion to banks and the credit they offer. This is a generation that came of age just before or in the wake of the Great Recession, a global economic crisis precipitated by … way too much credit. Young people love BNPL because, according to the former director of Afterpay, the vast majority of them “don’t want to be on credit.”

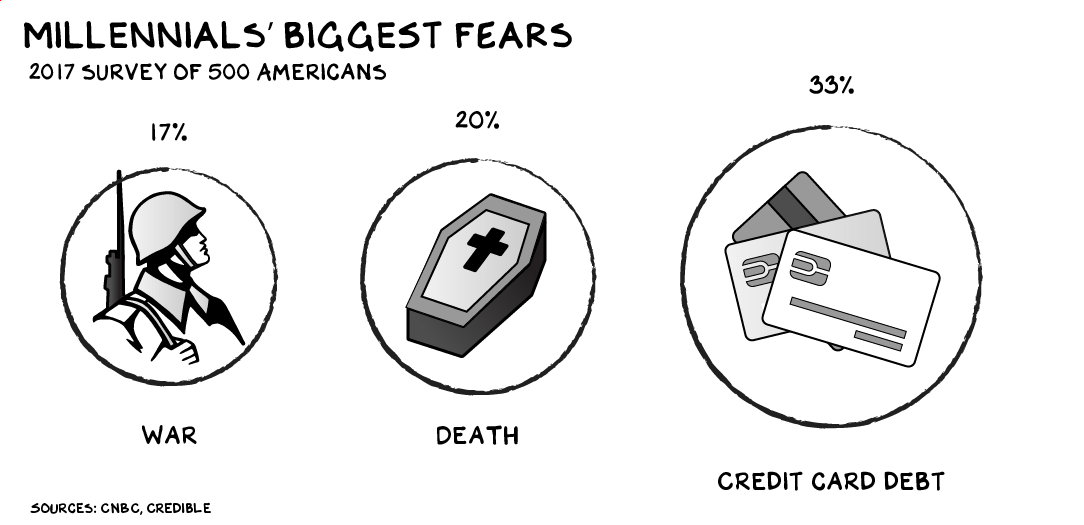

He’s not wrong. As Klarna reported in an investor factsheet, 1 in 3 millennials’ biggest fear is credit card debt. That’s more than name death or war. Deployment to Afghanistan is bad, but an unpaid balance on your Discover Card is (apparently) worse.

There’s one problem: Buy Now Pay Later is (wait for it) credit.

Hiding in Plain Sight

By most measures, BNPL services aren’t even good credit offerings. With a traditional credit card, you pay nothing up front, then you’ve got, on average, five weeks to pay without incurring any fees or interest. Closer to two months if you manage your billing cycles carefully. Carrying a balance will cost you, though, 1%-2% in interest per month. Miss a payment, and you get a late fee, about $30 — on which you’ll also pay interest.

In the short term at least, BNPL terms are worse. Take Afterpay. When you buy your new jeans, you have to come up with 25% of the money at purchase, then the lender gives you six weeks to pay off the remainder, in three installments. Miss an installment, and Afterpay hits you with a late fee. Continue in arrears, and the late fees increase, up to a cap of 25% of the purchase price. Also, you need a debit or credit card to make payments to Afterpay. Other providers have different fee and interest structures, but the basic model is the same. It’s credit.

BNPL companies market these limitations as features, not bugs. Because credit cards let you roll over your balance for a low monthly interest charge, you can rack up an insurmountable debt, which is harder to do with BNPL. Afterpay further limits customers’ risk by cutting them off once they start missing payments. It’s credit with training wheels, really. But it’s still credit.

BNPL marketing is Don Draper in Allbirds and a Patagonia vest, messaging for a modern age that generates irrational margins for the brand. Afterpay promotes that it charges “no interest!” However, miss one installment and you’re likely paying more, whether it’s called interest or a late fee. Afterpay competitor Affirm advertises the opposite: “Simple interest and no fees.” It then reiterates the message: “We don’t charge fees of any kind — not even late fees.” Bottom line, they’re all charging you the same thing: money.

Money Machine

So what’s the harm? Why not have a credit card with training wheels to ease young people into their journey toward a lifetime of debt? Especially as some of the costs are borne by the retailer in exchange for the consumer buying more sooner. Might Buy Now Pay Later even be training consumers to develop better purchase habits?

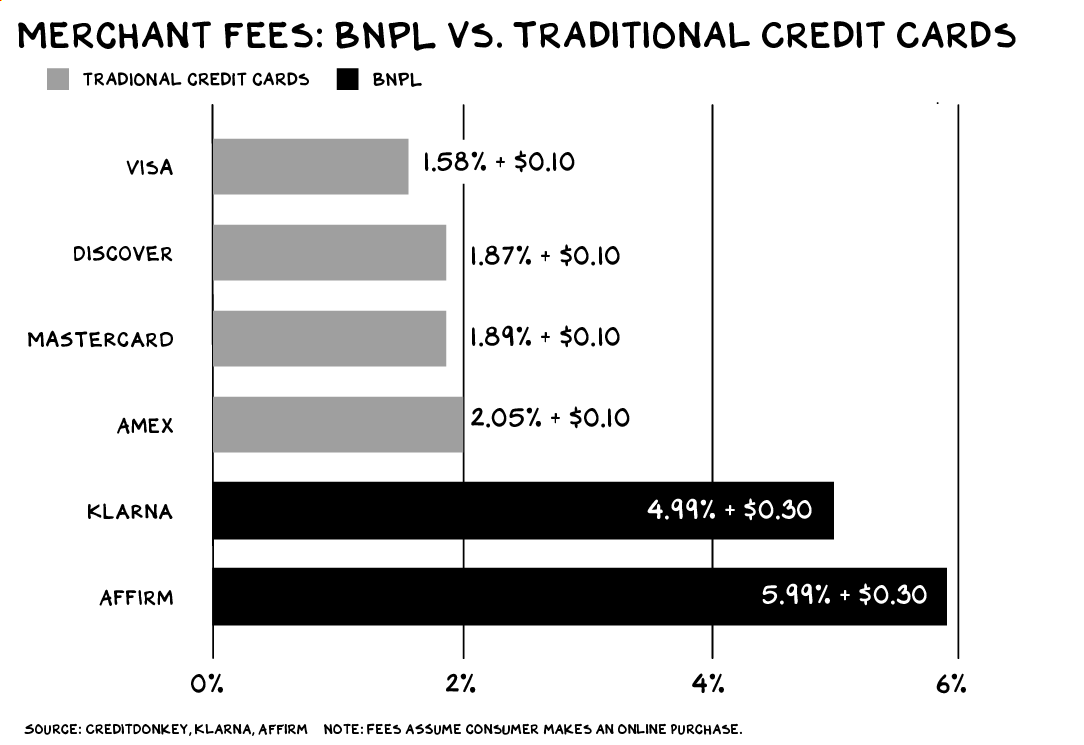

Here’s a good reason to be skeptical. (Let’s be honest, I’m skeptical about pretty much everything.) Pretending to be debit when you’re credit is an awesome business. BNPL firms take a larger cut of merchant sales than any other credit card company. Even AmEx — which charges merchants high interchange fees because its wealthy clientele are likely to spend more — gets a smaller share than Klarna, Affirm, and the like. Why would retailers do this? Because this technology/branding/sleight of hand convinces people to spend more than they would otherwise … full stop.

The business model is predicated on this fact: BNPL customers spend more money. Klarna boosts the average consumer basket size by 45%. Affirm increases it by 85%. Afterpay reports a 17% larger shopping cart, as well as a 12% uplift in overall sales. This is the psychological masterpiece at the heart of BNPL’s success: While fear of debt draws consumers toward Buy Now Pay Later, the model inspires them to spend more.

BNPL marketing teams are careful not to emphasize this with consumers. But on the merchant side, it’s the main event. More and more retailers are installing BNPL offerings at checkout, because they know consumers will load up their shopping carts. As a result, Afterpay’s merchant network has grown 500%+ since 2018.

Vulnerable

Buy Now Pay Later firms are quick to tell you that this is where they make most of their money — off merchants, not millennials. That’s true. But the business model only works by capitalizing on the instinct for immediate gratification. And younger neurons are more vulnerable to this marketing than older ones. The prefrontal cortex — the part of the brain linked to dopamine control and release — only finishes maturing at around 25 years old. As a result, younger people are far more likely to engage in risky behavior in search of instant gratification and quick dopa-hits. This is what makes trades on Robinhood, likes on Instagram, and purchases on BNPL so much more rewarding to young adults: They’re engineered to satisfy their neurocognitive architecture.

The problem is the companies are putting these people in debt. (Something I do every day: “NYU Professor of Marketing”. But I digress.) Australia’s financial regulator found 15% of BNPL users had to take out another loan to make their payments, and 1 in 5 had to cut down spending on essentials to make them. In 2019, Australian BNPL providers raked in $43 million in revenue from late fees, up 38% from the previous year. At a major U.K. bank, 10% of customers making BNPL payments overdrew their checking accounts in the same month. The authors of one study dubbed BNPL users “Generation Debt Trap.”

Some young people are beginning to catch on. TikTokers are dancing to the caption “crippling debt” after showing themselves purchasing new clothes with Klarna. Will a late BNPL payment hurt your credit score? Some of the companies say it won’t, others say it might. But a recent study found that a third of U.S. BNPL users have fallen behind on one or more payments, and 72% of them said their credit score dropped.

In countries with functioning governments, regulators have recently started to take action. After the U.K. announced a crackdown on BNPL, Klarna decided to reword its marketing to make it “absolutely clear” that it’s offering credit and not debit. Sweden recently prohibited credit payment options from being presented before debit options, sending BNPL options to the bottom of the check-out screen. In July, TikTok banned financial services brand advertising from its platform, including BNPL products.

U.S. regulation is trickier, as consumer credit laws vary by state and BNPL companies structure their offerings to elude many of them. Keep in mind, the last president is one of history’s most prolific debt-defaulters. And our current president was nicknamed “the senator from MBNA” for his good work ensuring that credit card debt (and student loan debt) couldn’t be escaped via bankruptcy. Young people aren’t wrong to be concerned about credit. They’re just being lied to about it.

Your Social Movement Is My Benjamins

Social change has become a marketing veneer to create shareholder value, vs. actual … social change. We have entered into a consensual hallucination with the marketplace that our most pressing challenges can be solved by a college dropout who will make us rich in the process. No. Climate change, teen depression, income inequality, and profligate debt have made a lot of people exceptionally wealthy. And the cost to unwind the damage will be expensive … for all of us.

The electric vehicle market, for example, has been flooded with capital on the premise that the TAM is not electric cars, but climate change. (I see no other explanation for a $100+ billion valuation for a company that does $0 in revenue.) Robinhood built a $24 billion cache turning the stock market into a slot machine with shiny buttons and fake confetti, while claiming it was “democratizing finance.” And Facebook’s mission is to “bring the world closer together.” One insurrection and extreme dieting site at a time.

Today is Black Friday. I expect our Gen Z representative to blow next month’s paycheck on a box of $6 sweaters made in a Chinese labor camp, then lecture us on how our eight-year-old (paid off) Toyota is ruining the planet. Get. Off. My. Lawn.

Life is so rich,

39 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

Best closing paragraph I’ve read in any article or “journalistic” story in a very long time:

“Today is Black Friday. I expect our Gen Z representative to blow next month’s paycheck on a box of $6 sweaters made in a Chinese labor camp, then lecture us on how our eight-year-old (paid off) Toyota is ruining the planet. Get. Off. My. Lawn.”

Literary genius 🙂

+ 1

My career has been devoted to the financial security of low-to-moderate income people and from my vantage, the Professor has described the issues and shortcomings of BNPL perfectly. Early Wage Access is more “lipstick on a pig”: dangerous credit products that are more likely to destabilize and cause financial insecurity for those least able to weather it.

India had this too for a very very long time. My dad ran his clothes business on this model for a very very long time – from 1960s to 2010. I still see this in India though less frequent. In every case – as you point out – it is credit, just different name.

Credit card (and all other forms of debt) create fear in the mind of the borrower, making people even more risk averse and thus making them great workforce, that remains in line and works hard.

When I read this I thought…have we forgotten 1938 – the year the U.K. introduced the Hire Purchase Act to combat this (near) exact exploitation of vulnerable people.

“Love BNPL because “don’t want to be on credit.”… not reporting borrowings to credit bureau and using multiple BNPL providers is only going to lead to more debt. That is when realization will hit, “credit” is right in the name 🙂 You are expected to pay later…. how else is credit defined ?

Hey prof, did you know that in Brazil we have BNPL as a widespread and almost expected form of payment? You should have a look!

Great article and dive into the details – reminds me of this, except replace nation with generation: “There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt. John Adams

Even more problems with BNPL include no consumer protection. Any dispute with a merchant is the buyer’s problem unlike card companies who will reverse a charge for you and mediate with merchant. Also managing multiple due dates on multiple purchases a challenge for people who over-use BNPL. Finally, there are no rewards points or cash back benefit from use. BNPL is just a bad product from a consumer POV.

These are really good points Tim. Also thx to prof g for another thoughtful post

plus…Goldman Sachs bought out Greensky recently. The Big Folks (not boys or guys anymore!) are not sitting idly by. I imagine a “new” VISA card that’s sorta debit and sorta credit i.e. a BNPL card. We’ll even give it a new brand name: Verily…as in mostly sorta, kinda like a VISA card but now quite and if you default on the up front payments, it dumps the remaining balance into a VISA account at 18%.

Great story as always, but PLEASE get someone to fact-check your articles before you publish them. Too often I’m finding that when I follow stats or stories through to the source, it doesn’t support the way you’ve portrayed it.

Example: “As Klarna reported in an investor factsheet, 1 in 3 millennials’ biggest fear is credit card debt.”

Klarna (and others who reported the Credible survey) conveniently omitted the fact that the survey population was specifically millennials with credit card debt. Depending what source you use, that’s only about half of the demographic – and I presume the ones without credit card debt aren’t so concerned about it. Also, the entire survey was about credit card debt habits and opinions – is it a shock that they then mentioned their credit card debt as a fear? AND this survey was from *2017* – do we really think their fears are the same today? This is just one of a half-dozen iffy pieces of supporting evidence I’ve found in the article so far. This doesn’t mean I disagree with your takeaway – I abhor the behavior (and often the model) of these businesses. I just feel like you’ve served me a nice dish with inedible garnish, and I’m left full but unsatisfied.

Excellent piece!

One comment though, over hier in Europe AMEX can charge upwards of 10% to an outlet/business, at least that was the practice for years. Of lately you can hardly use AMEX in Europe anymore, due to those horrendous charges most places do not accept the card anymore…

Excellent piece!

One comment though, over hier in Europe AMEX can charge upwards of 10% to an outlet/business, at least that was the practice for years. Of lately you can hardly use AMEX in Europe anymore, due to those horrendous charges most places do not accept the card anymore…

Brilliant piece of Gyaan as they would say in India. Needs to be disseminated worldwide and to the younger generation.

Dear Mr. Scott as usual you have hit nail on the head. I would seek your thoughts on how parents can play a role in this change or if they will be able to do?

We looked at Afterpay as a financing option for the stereos my company sold. ($3K – $7K, retail) We were convinced that we’d have increased our sales but those sales had to be held on our books for 6 months because Afterpay could force us to take returns. (Right now, it’s only 30 days.) As you might guess, being unable to recognize income from a sale for 6 months would wreak havoc on a small company’s balance sheet and banking relationship!

Why shouldn’t today’s generation do whatever they want financed by debt? That’s exactly what our government is doing!

Scott wrote: “Debt is not as bad as cancer. Though it can trigger depression and even revolution. But that’s another post.”

There’s already a great book on this — an American History book — by Scott Reynolds Nelson, A Nation of Deadbeats: An Uncommon History of America’s Financial Disasters, 2013. Deadbeats refers rather obliquely to those unfortunates with debt — when leaving town also left the debt behind. Life is no longer that simple!

I realise that the BNPL craze is geared more toward Millennials and Gen Zed, but I wonder as a percentage how much this credit craze in spending compares to the cash-out refi craze of 2000-2006, which was another form of BNPL (although the hope was the home value would cover the PL).

You have come along way from Mr. Miller‘s homeroom. And I’d like to thank you for dragging me with you. Not necessarily then, but definitely now.

Great piece – how these guys successfully rip the faces off the merchants while seducing customers into financing consumables is a remarkable marketing achievement. Debt should be mainly used to to finance long-term assets (homes, cars) rather than short-term consumables (shoes, clothes, etc). Why are Elizabeth Warren and AOC busy sparring with regulated institutions rather than focusing on unregulated lenders?

Prof – while I think this article is great I hope it’s just the first instalment (pun intended). My favourite articles of yours are those that get under the hood of a firms profitability. You didn’t go there, none of these firms have made a profit but still valued at astronomical valuations. Have a crack – I know you’ll have fun with it 🙂

You may be the smartest Man I’ve never had the pleasure of meeting.

This is a fantastic article and I am in agreement 100%. Very slippery slope and needs to be reported on more.

It’s really kinda of funny that US and Europe have this problem now. I’m Brazilian, and here we use ‘Buy Now Pay Later’ for about 30 years already.

When I was younger and went to the US, I’ve always found it funny that they didn’t have this option. Here, we had this because of inflation crisis in the ’80s and ’90s made the price change a lot. So, we came with this scheme to be able to buy things with no inflation impact.

Here, it works fine. Let’s see how you get it.

THANK YOU for this article!!! I’ve been waiting a while for this type of explanation/breakdown. I’m sending it now to all the kids and grandkids!!!

I get your argument, but I strongly suspect the value proposition of BNPL is to get people to make purchases (re: financial commitments) where they otherwise might not have. This marketing scheme doesn’t necessarily prey on the same inclination of credit buying as it does attention capture. It likely presupposes that its target demographic both has the financial wherewithal and discipline to fulfill its financial commitments; it just wants to capture those commitments before something else does. Like avocado toast, brunch, or another brand that had its ad displayed at a more opportune time.

Great read, also great to mix in human brain / psychology to z consumer behavior. That explains the root – I wish all the gen zers out there would read this!

Straight to it. I do appreciate the pointing out of the last paragraph of the $6 labor camp sweater. I tried to pass on to my sons and myself the Same moto that yvon chouinard said”‘Poor people can’t afford to buy cheap.”

Id put it another way not trying to imply I’m poor, but you get the statement. It goes for our personal income as well as our planet . And what and how we purchased was and is huge. So when you are putting your purchasing power towards organic foods, less packaging, mindful packaging, supporting those lands near and far away for better production and living to get us our goods. Sure I’d love an electric car yet that resource comes from somewhere I just keep fixing my 2001 Mercedes 4matic wagon . I’d much rather have kickass public train transportation that easily connects through California and the rest of the nation . WTF?!!

. As a ‘graduated’ single mom I’m always forwarding your podcasts to my 2 sons and my nephews, first, then my word on the street conversations.

One smart guy.

Another great post. You are my favorite curmudgeon (and I’m way older than you in my curmudgeon development). Keep writing!

Excellent post, prof Galloway!

BNPLs as well as Meta should donate massively to social media accounts of NGOs like EDF, NRDC, WRI. Google.org is the model.

Brilliant. thought-provoking piece of work, Scott! Very apt association between nefarious products marketed with positive-sounding language, from opioid “medications” to social media “connecting the world” to high-priced credit, this time remarketed in the innocuous-sounding language of “Buy Now Pay Later”.

Let’s call this what it is…credit-based layaway.

Exactly what I was thinking! It’s like predatory layaway.

Brilliant and thought-provoking as usual. Since we have so many examples of “changing the subject” generating mass shareholder wealth for companies that should have been figuratively punished for what they were doing (cigarettes, Meta, Affirm), whats an example of a company or organization that has taken a negative brand and spun it to generate a social good. Why havent we seen the same situation arise to help push the climate change movement? Is it simply because there as no money involved, and thus, no marketing dollars spent towards it? If thats the case, why arent these mega billionaires who are “donating” to social causes using this playbook?

Great research, as usual! Thanks