Jumping the SPAC

Jumping the SPAC

Note: I was not under influence of Zacapa or edibles writing this one … so it’s wonky. Oh well, my blog.

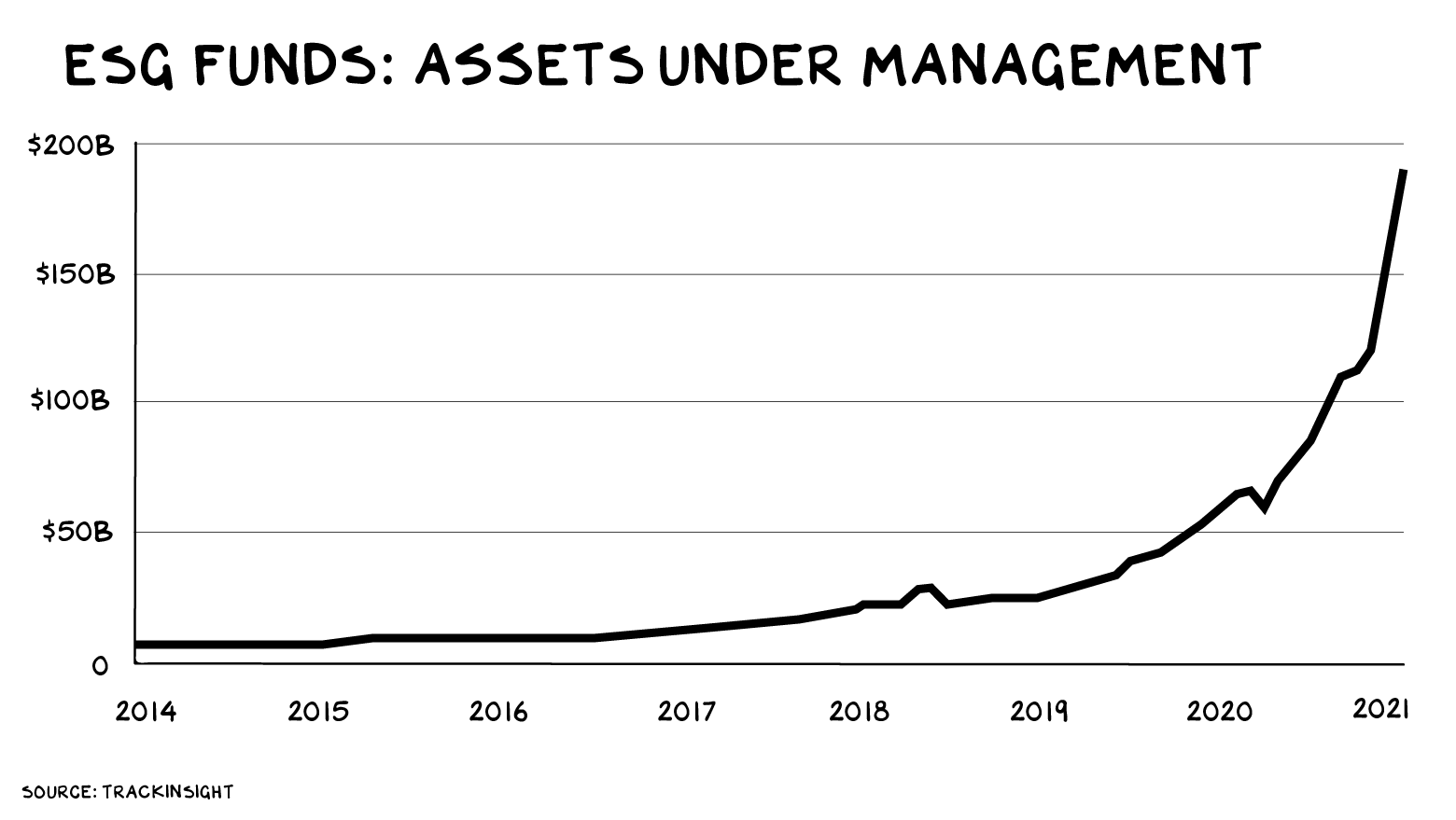

A perfect storm may be brewing: tech, software as a service (SaaS), and climate change. My podcast co-host, Kara Swisher, believes the first trillionaire will be an entrepreneur who addresses climate change. It’s not unthinkable, as Elon Musk is already 15% of the way there — to a trillion in wealth, not solving climate change. I’m more skeptical and believe the only entities that can begin to reverse climate change are the EU and the governments of China and the U.S. Capital is pouring into the space, and funds that claim to invest based on an “Environment, Social, Governance” (ESG) basis are hot. These capital flows will produce a bevy of firms that tap into the consensual hallucination that society’s biggest problems can be fixed as our stock portfolios explode in value. Yeah … wouldn’t that be nice. No, just as turning back Hitler and smallpox took leadership, treasure, and blood, so will this.

The most recent ayahuasca trip is Aspiration, a finance firm that claims its products “can change climate change.” In August the company announced it was going public (via SPAC) at a $2.3 billion valuation. (Investor presentation available here.) Change climate change. That would be awesome. Except there’s a catch. This is a fucking debit card.

Aspiration’s Aspirations

Aspiration was launched in 2015 by a former Clinton White House aide and Elizabeth Warren protegee. Its initial (and still primary) consumer product was a debit card with some green features. The company claims money deposited in its debit accounts “won’t fund fossil fuel exploration or production”; it plants a tree every time a customer chooses to round up a purchase; and it offers 3% to 5% cash back on purchases from “mission-focused merchants.” More recently, the firm launched another debit card that, in exchange for a monthly fee, offers an interest-bearing account and larger cash-back awards. Both cards are made of recycled plastic.

The company also offers an ESG-focused investment fund, Redwood (REDWX), and has plans to launch a credit card. The sleek-looking black slab of biodegradable plant matter, called Zero, was announced in March, but remains vaporware. Half of Aspiration’s revenue comes from the fees that flow to debit card issuers (interchange fees, interest, subscriptions for the higher-tier product), and half from the corporate “sustainability-as-a-service,” discussed below.

None of this is particularly innovative or market-leading. Aspiration doesn’t even pretend its direct economic benefits are anything special. It’s not PayPal, Affirm, Square, Ualá, or Public, true innovators that are disrupting existing payment and finance models.

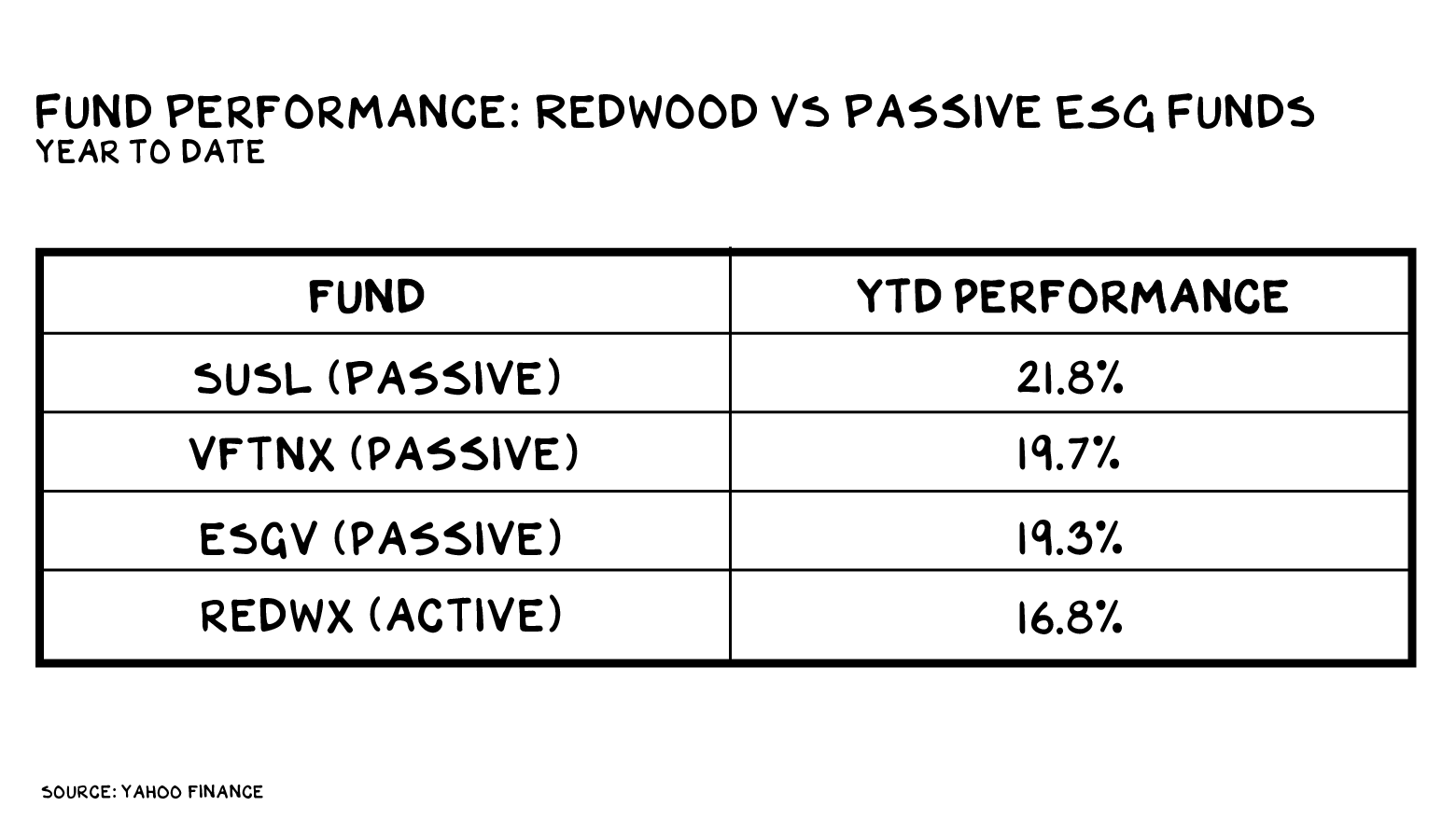

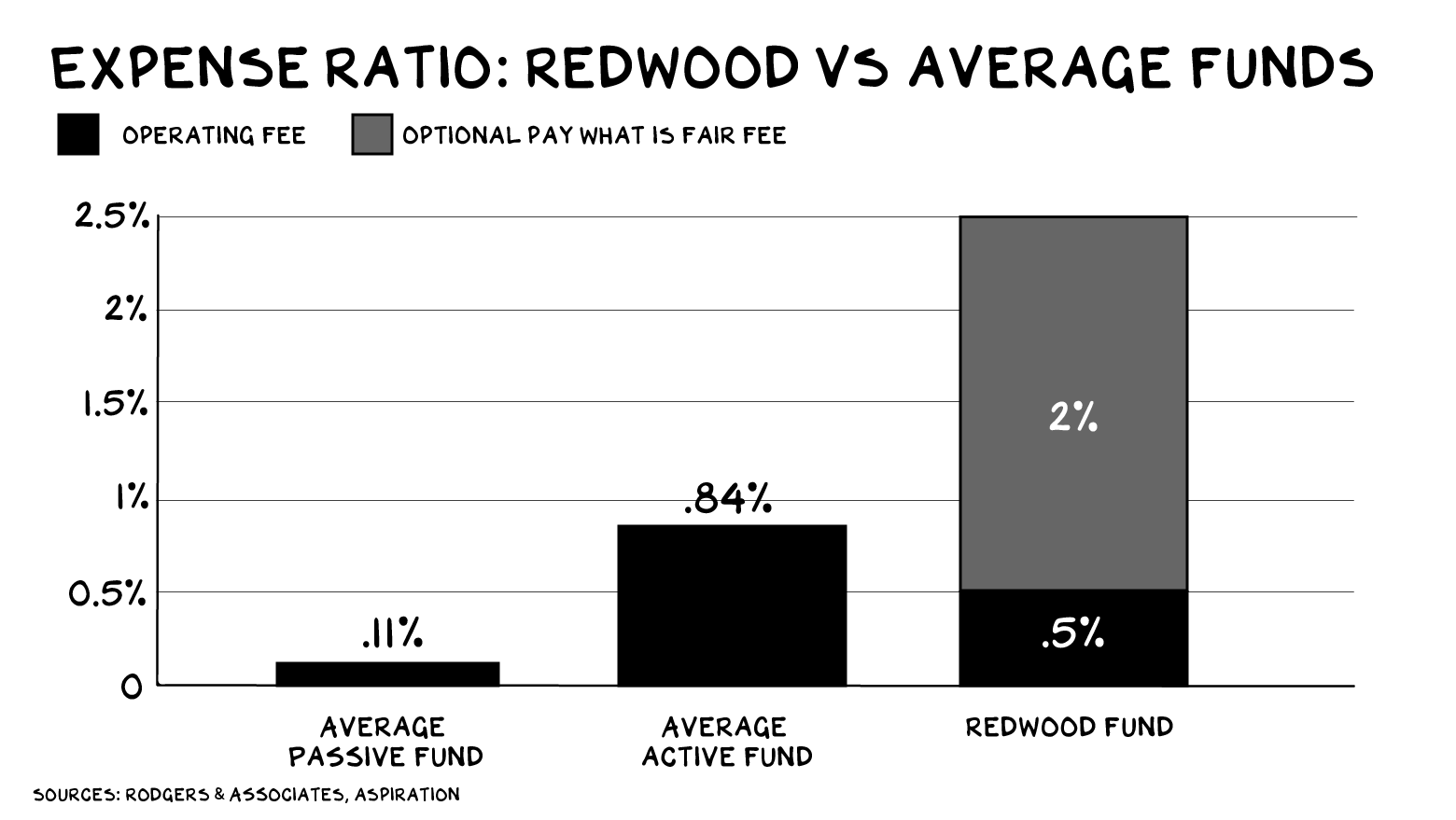

Aspiration’s Redwood investment fund does offer two apparent points of differentiation from other ESG funds: Its performance is worse, and its fees are higher.

The company’s marketing focuses on a “pay what is fair” model, which permits investors to choose an annual fee between 0% and 2%, depending on what they believe is “fair.” (Hint: the answer is zero.) But keep reading the fine print and you find a base fee of 0.5%. That compares unfavorably with fees of higher-performing passive ESG funds (SUSL: 0.10%; VFTNX: 0.12%; ESGV: 0.14%).

The bottom line? Investors pay more for REDWX than they would for a better-performing passive fund, but they can pay significantly more if they want.

It Ain’t Easy Being Green

If you use Aspiration you will, according to the firm’s materials, “save the planet.” Again … awesome. Except you won’t. The company guides debit card purchases toward companies with a high “AIM” score (“Aspiration Impact Measurement”), a metric Aspiration appears to have invented and defines nowhere. But a look at the 10 most highly AIM-rated companies (i.e. the “AIM Nice List”) suggests the scoring system leans towards the qualitative. The top 10 in 2018 include Sephora for “promoting fearless beauty,” Target for “normalizing diversity,” Marriott for “adding love to travel,” and my favorite, Delta for “flying cleaner than ever.”

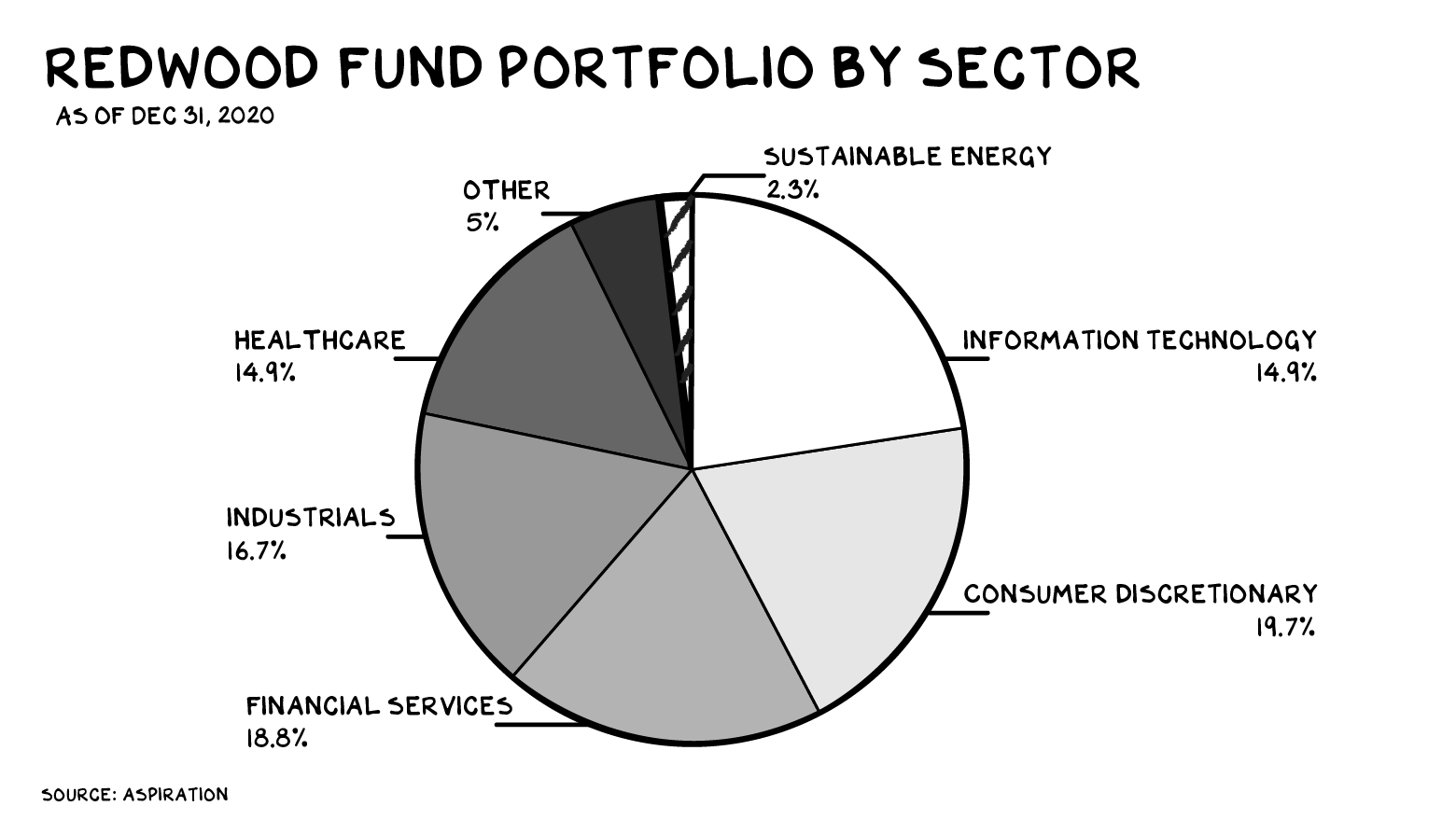

Aspiration claims the Redwood Fund is “100% fossil fuel-free.” But almost 3% of its holdings are in Southwest Airlines, a company that burns 2 billion gallons of fuel per annum and was labeled a “high ESG risk” company by Sustainalytics. Another portfolio company is Linde, an industrial gas company that touts its “experienced team of oil and gas specialists,” and brags that it’s “been supporting the industry for decades,” with particular expertise in … wait for it … fracking.

Sustainable energy is Redwood’s smallest investment sector, accounting for only 2.3% of total assets. The fund’s investment in Southwest alone surpasses that. The bulk of the portfolio consists of stocks that are prevalent in every portfolio, such as Microsoft and Starbucks.

How does Aspiration justify including companies like this in Redwood’s portfolio? That’s where the magic of ESG comes in. Redwood (allegedly) evaluates investments across all three considerations. If “social” and “governance” sound amorphous, trust your instincts. This allows Aspiration to tout Redwood’s climate bona fides, while actually investing in the same companies as everyone else, just so long as the companies have “anti-bribery ethics” and low employee turnover.

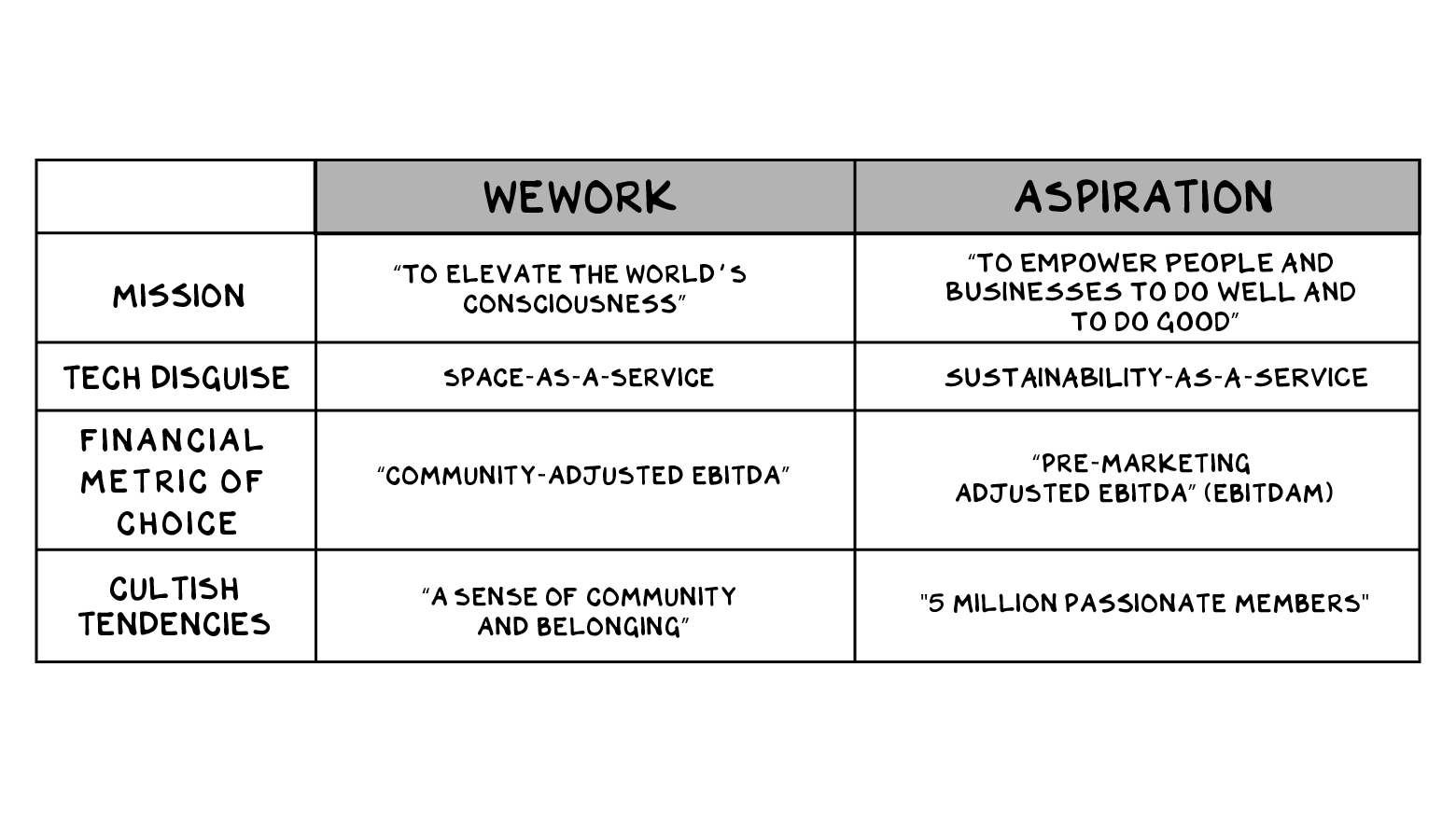

Finally, between its debit card and its corporate business, Aspiration claims it will plant 5 billion trees over the next 20 years (“at attractive profit margins for the company”). This is the primary mechanism its products use to “save the planet.” Reforesting the globe is a legitimate environmental goal with a broad array of benefits. But in terms of turning back climate change (Aspiration’s frequently stated aspiration), 5 billion trees in 20 years is … a start, sort of. According to a recent study in Science, it will take 500 billion trees to capture just the additional carbon we are slated to spew out over that period.

These sojourns in Wokeistan illustrate a larger trend: ESG projects promoting the fiction that we can shop our way out of climate change. American consumer culture results in a carbon footprint per person that’s four times greater than the global average. Flying Delta instead of United is not going to change that. Pretending otherwise is much like the way tech leaders dress in woke colors to distract us from the damage their firms levy on society. Sheryl Sandberg speaks eloquently re the need for safe places for our children to distract us from the need to find places safe from Sandberg and the Zuck. But I digress.

B2B(S)

In 2020, five years after debuting its debit card, Aspiration managed to expand revenue to just $15 million. Yet the company claims that in 2021 its consumer business will triple, to $43 million, and its recently launched corporate consulting business will generate $55 million. And then that corporate business will nearly double in 2022.

From what we can discern, the “sustainability-as-a-service” business is quasi-consulting that helps firms assess their carbon footprint, then brokers the carbon offsets necessary to account for it, marking up the offsets. Similar to the classic advertising agency model: Do the work for free and make money on the media buy.

How this works in practice is unclear: is this a scalable methodology that Aspiration can deliver to dozens of companies via an army of crisply trained college grads … or is it sophisticated consulting that requires experienced people and bespoke work? The former might be scalable at the rate Aspiration projects, but it’s also a low-value-added business with no moats or switching costs.

Building a true consulting business would be more, well, sustainable, but building consulting firms is a long, hard road (I have some experience with this). And the only member of Aspiration’s management team listed with any experience working at a consulting firm is the CTO, who worked at Accenture for 16 months and left in 2008. Nor does the company have any job postings on LinkedIn for consultants.

When the Ducks Quack

The hype around Aspiration is relentless. The company’s site and investor deck tap into a trifecta: ESG, celebrities, and the very-hot-right-now “as-a-service” moniker.

In 2019 the company announced Leonardo DiCaprio as an investor and “advisory board” member. Included in the list of Aspiration’s Hollywood backers are: Orlando Bloom, Robert Downey Jr., Cindy Crawford, Doc Rivers, and Drake. Word is Leo’s testicles have swollen, and he’s been invited to the White House — couldn’t resist.

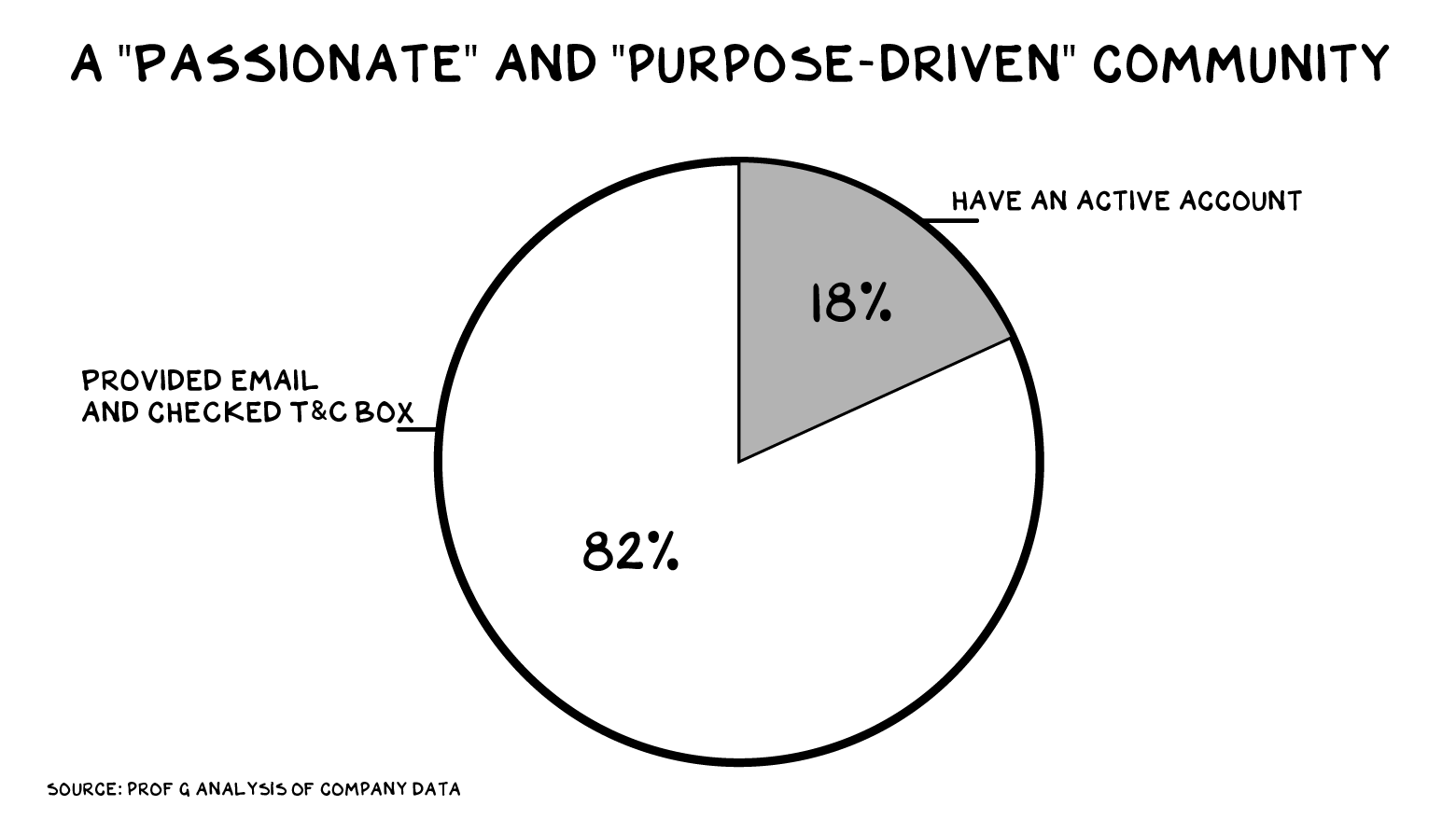

To further fuel the hype machine, Aspiration boasts that it has a “community” of 5 million “passionate” and “purpose-driven members” (see pages 5, 7, 15, 16 of the investor deck). But the company had only 361,000 actual customers at the end of 2020, and its projections suggest it has less than 1 million currently. How does it get to 5 million? A footnote in the deck clarifies that to qualify as a member, one need only have signed the company’s terms and conditions at some point (which requires only clicking a box when you sign up for the company’s email list). That means less than a fifth of Aspiration’s “members” actually use its product.

The media loves the hype, and the firm’s ability to generate press is a tangible competence that should reduce marketing spend. Fast Company called it a “world-changing app.” It was named in Certified B Corporation’s “Best for the World” list four years in a row. It made Inc.’s “25 Most Disruptive Companies.”

Yogababble: ESG Edition

When presented with companies promising the world, we apply our Yogababble analysis to their investor documents. In our experience, there’s an inverse correlation between the level of BS in a company’s materials and its stock return post-IPO. Aspiration’s mission statement: “Aspiration is in the Business of Sustainability — Our Mission is to Empower People and Businesses to Do Well and to Do Good.”

We don’t have a prospectus for Aspiration yet, but a Yogababble assessment of its investor presentation reveals the following: “Sustainability/sustainable” appears 30 times, while “profit” appears 11. Excluding mentions in footnotes, “climate” appears 10 times, while “debit” (the company’s actual product) appears only four times. The company promotes its AIM score but never explains how it works. It does, however, describe it as “a Fitbit for sustainability.”

EBITDAM

Smearing more vaseline on the lens of the actual business fundamentals, Aspiration turns to creative accounting. Specifically, it leans heavily on a profitability measure called EBITDAM. EBITDA is the familiar “earnings before interest, taxes, depreciation, and amortization.” It’s a measure of how profitable a company’s core operations are before the vagaries of capital structure, tax strategy, and accounting charges. EBITDAM excludes all those things … and then also excludes marketing spend.

In very small doses, this is not crazy. Debit card customers tend to be loyal — Aspiration claims more than 90% customer retention. So the idea is that marketing is mainly for acquiring new customers, and if you want to see how the business performs on its existing customer base, you should exclude those costs.

But Aspiration attempts to elevate EBITDAM far beyond its station. In an introductory “Aspiration at a Glance” slide, it claims to be “Cash Flow Positive,” and then in smaller type “Before Marketing Expense,” and then, in an even smaller footnote to that smaller type, identifies this as EBITDAM. Which is nothing like a measure of cash flow. Over in reality, the company’s operations burned $34 million in 2020, and they’re projected to burn $133 million in 2021. In the rest of the deck, Aspiration refers to its “EBITDAM profitability this quarter” and then uses EBITDAM throughout its financial analysis. Which is rich for a company whose entire (projected) profit model is dependent on explosive customer acquisition, which (to date) has been really, really expensive.

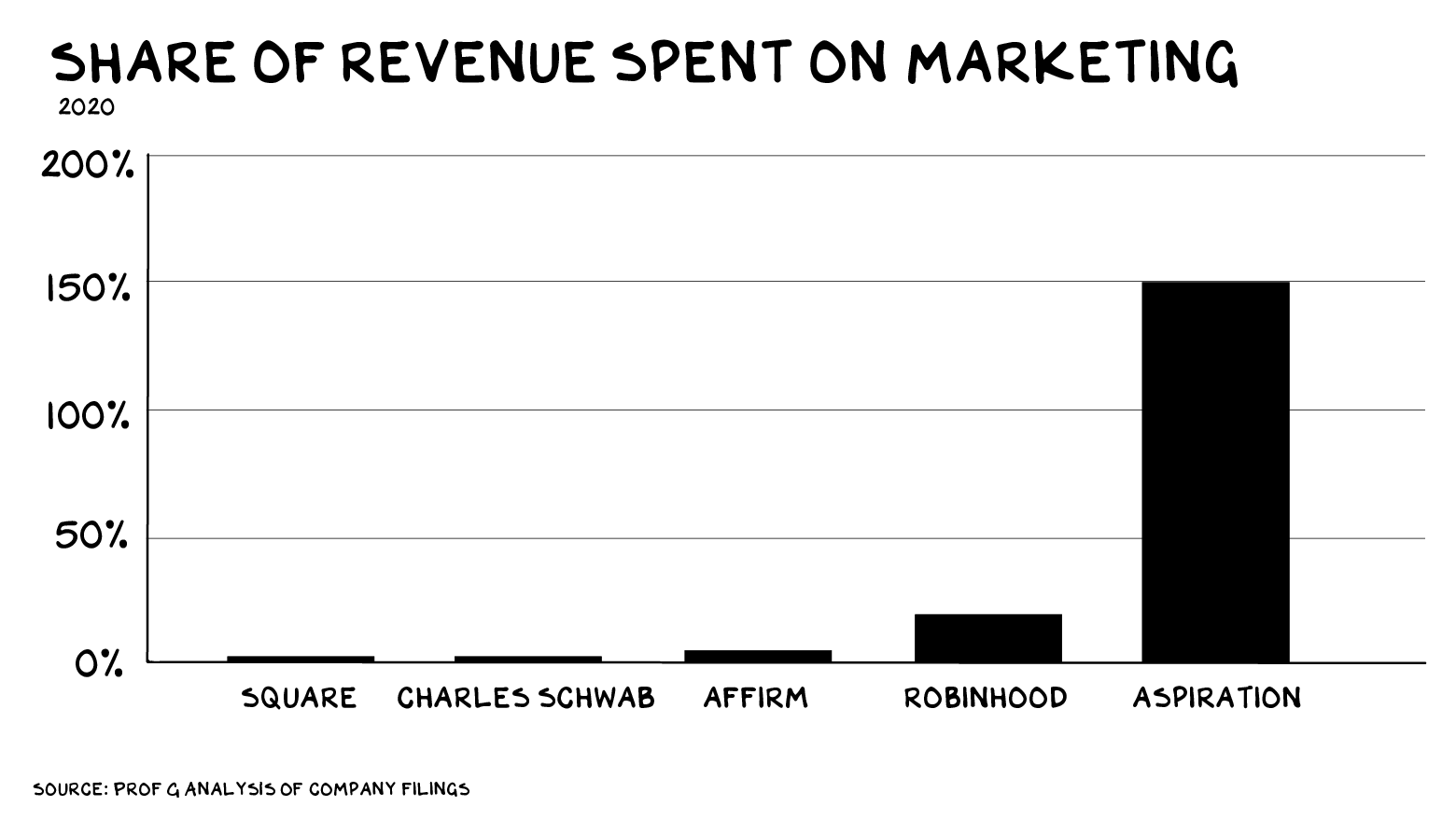

How expensive? The company spent $22 million on marketing in 2020, roughly 50% more than the revenue it generated that year. This year it plans on spending $149 million on marketing, 52% more than expected revenue. Compared to comparable firms, Aspiration’s marketing spend as a share of total revenue is stunning:

SPACtacular

What could greenwashing garner its backers? Potentially a $2.3 billion public market capitalization, should the anticipated SPAC go through.

This is a firm that registered less than $15 million in revenue last year. PayPal makes $15 million in revenue every five hours. It’s less than most NFL starting quarterbacks made in 2020 — Leo’s former girlfriend’s husband made over twice that.

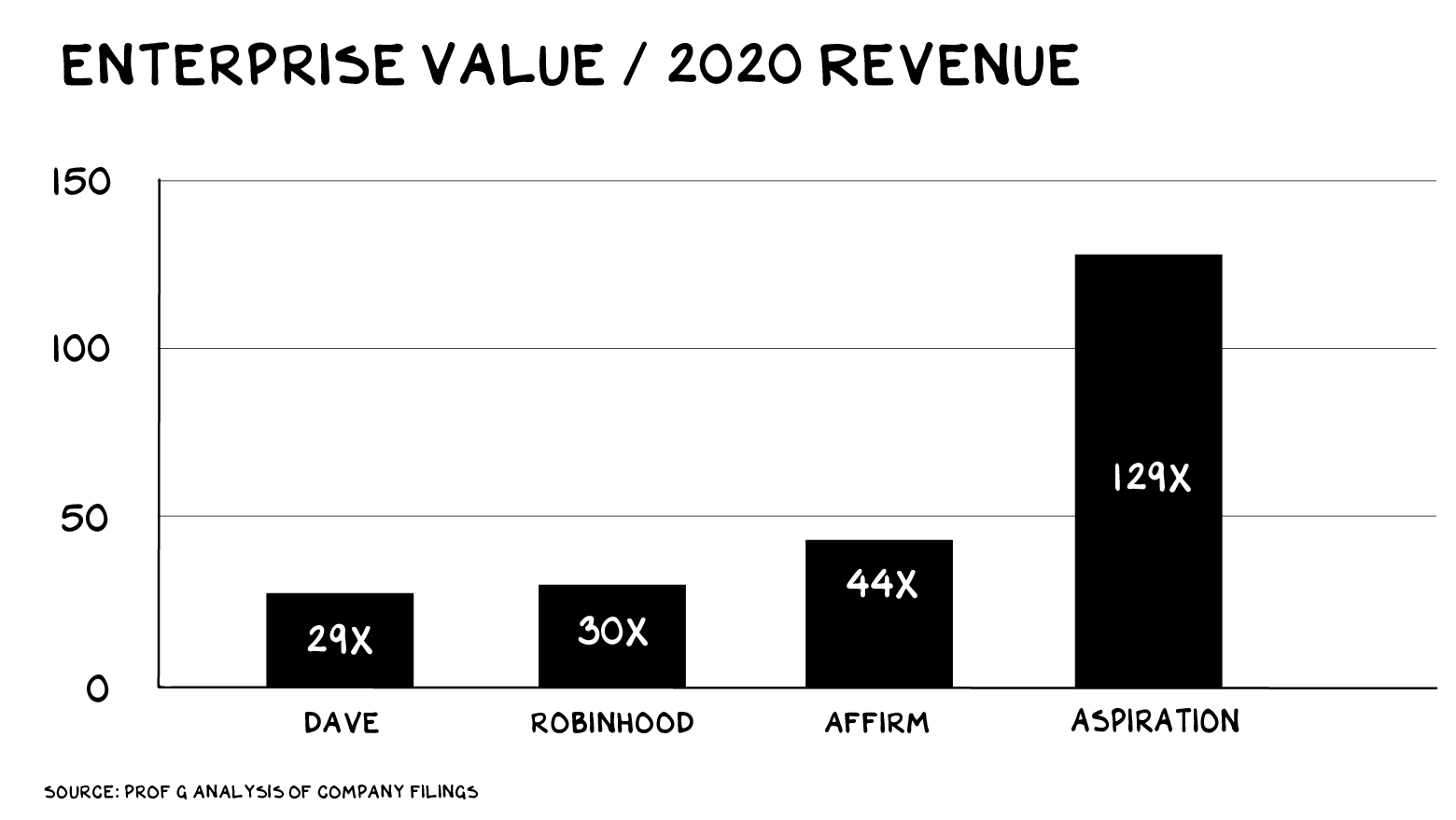

Aspiration is a difficult firm to value, considering its blended corporate/consumer revenue mix and ambitious projections. But the core of the company is its debit card business, and for that we have a close comparison: Dave. Dave is also going public via SPAC, and it also has an investor deck with similar information. Dave was EBITDA positive in 2020 on $122 million in revenue and finished the year with 3.7 million active accounts. Dave’s post-SPAC projected enterprise value is $3.6 billion. That’s 29 times its 2020 revenue.

Aspiration, meanwhile, lost $63 million in EBITDA last year on $15 million in revenue and finished the year with 360,000 consumer accounts (and two corporate accounts). Aspiration’s post-SPAC projected enterprise value is $1.9 billion. That’s 129 times its 2020 revenue.

A growth-driven valuation can be justified, but for companies with real strategic advantages. I’m not seeing any moats here — just the captain of Aspiration Air Flight 2.1 asking us to look out the left side of the plane and gaze at the bright lights of Wokeistan.

There’s one more number that jumps off the page in Aspiration’s investor deck. In 2020, when the company did less than $15 million in revenue, its general and administrative expenses were a whopping $47 million. G&A is typically salaries, daily expenses, rent, legal fees, that sort of thing. It should not be three times your revenue, five years after launch. By comparison, in 2018, when Dave was at $17 million in revenue, its G&A line was $4 million. Without more detail it’s hard to know what’s going on here, but a $47 million G&A line for a $15 million business is a red flag.

WeSG

To be clear, Aspiration is not WeWork. The story of We is insanity; Aspiration is mere intoxication. Specifically, a market drunk on true disruptors that have delivered unprecedented returns. Aspiration is only crashing a Bombardier Global Express into a mountain every six months, vs. every three days. Yet, the comparison between the two companies is striking. It’s beginning to smell like teen spirit … if teen spirit is bullshit.

The emissions from our idolatry of innovators and a 13-year bull market have resulted in an investment ecosystem that’s warmed to a boil. However, unlike in the actual environment … this warming will be self-correcting. A debit card and mediocre fund management masquerading as a SaaS firm will likely add fuel to the SPAC unwinding that has commenced. Regardless of how green a firm says it is, a shitty business wrapped in the flag of Wokeistan cannot change the weather. Winter is coming.

Life is so rich,

P.S. My colleague Adam Alter is not only better looking than me, he’s also probably smarter. Anyway, he’s teaching the next Fundamentals of Product Strategy Sprint with Section4. Check it out.

36 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

Getting an Aspiration account was the worse decision i made this year. I reported the debit card stolen from the mail box before it was activated almost 2 weeks before someone activated the card and stole 2,000 from me. Then they locked me out of my account for over a month blocked my phone number and would leave me on hold indefinitely when id call customer service. They only returned1290 of the money. I think they steal from my account in each transaction because receipts and transaction history do not match.

brilliant analysis as usual Prof G. It is amazing how many of these so called ” disruptive” tech companies are well marketed vaporware. You would think that the investor community will learn the lessons of the likes of Theranos – but guess people are so desperate to find the next big shit – that they have forgotten how to distinguish BS from actual stuffbrilliant analysis as usual Prof G. It is amazing how many of these so called ” disruptive” tech companies are well marketed vaporware. You would think that the investor community will learn the lessons of the likes of Theranos – but guess people are so desperate to find the next big shit – that they have forgotten how to distinguish BS from actual stuff……..www.smartcas1.com

Scott you covered the BS in both ESG and SPACs in a single post, well done. Lou

The Analysis is really good now I’m just waiting for Prof. Damodaran to do a valuation video on this and show us the Quantitative part.

Thanks, Prof. Galloway.

yh

Very unique PIPE on this deal. PIPE investors are provided up to a whole additional share based on actual post deSPAC trading performance.

Which means the PIPE investors are made whole down to 50% of their buy in price (ie $5). That protections not offered to trust investor

Minimum cash balance sized to PIPE which means deal can close with 100% redemptions.

Not exactly a screaming endorsement by PIPE of the valuation

Excellent analysis. Really hope it is picked up by the mainstream investor press. A real caveat emptor story.

I love the parting line, “The winter is coming”. Thanks dogg!!!

brilliant analysis as usual Prof G. It is amazing how many of these so called ” disruptive” tech companies are well marketed vaporware. You would think that the investor community will learn the lessons of the likes of Theranos – but guess people are so desperate to find the next big shit – that they have forgotten how to distinguish BS from actual stuff

Great analysis, company insiders should serve time!

This is a great analysis. This piece, and the recent essay in Medium by Tariq Fancy (former head of “sustainable investing” at BlackRock) should be required reading for anyone wanting to understand how much of ESG investing is basically a scam.

So if Aspiration is terrible, what is a good brokerage or bank?

Worth reading, thank you.

Keep up the good work.

AB

As someone who worked at Aspiration, it’s a company of smoke and mirrors. This article is spot on: “Regardless of how green a firm says it is, a shitty business wrapped in the flag of Wokeistan cannot change the weather.”

Yes, but why?

Why waste all that space on Aspiration?

Or – could it be a parable??

Fascinating as always but a bit too obsessed this time around…

So, you’re saying it’s a good investment?

TL;DR, but my attention was caught by that new ESG buzzword. Not so new actually. To address the environment crisis in an honest way, the world needs strong commitment: in short, what we need is a new buzzword. Difficult, yes, but the sky is the limit. How about EDGGHT ?

note to self: ask that new Buzzwords VP (what’s his name again ? darn..whatever) to figure out if we can make some money with my new idea.

Oh man I LOVE this article. You absolutely Rinsed them! 👏🏼👏🏼

Thanks for pointing out that ESG is BS.

ESG is just another form of virtue signaling

Another edible and we really would have known how you felt. Note: I’m four Hard Seltzers in… oh well, my comment.

I respect Professor Galloway and I am an Aspiration account holder and REDWX investor for a few years now. I am not going to argue the facts, but just say one thing. The expert of marketing and branding knew he would get 40% of the population locked in once he used the Wokeistan claptrap. Using it three times was more effective than all the other words combined.

I did not want to miss the non-GAAP metrics bandwagon, so I offer you EBITDAPETINKS: EBITDA Plus Everything To Include the Kitchen Sink.

I help private companies merge into SPACs. This article is perfect!!!

Divesting from harmful industries is done on the debit cards through the depository accounts. This is their primary “ESG” impact. Was it left out of this article purposely?

ESG is the new Disco. In a decade, today’s young people will be asking each other, as older people do now ‘What were we thinking?’

Great piece, thoroughly enjoyed it.

I hope they do ultimately go public; what a short opportunity!

Incidentally, isn’t this whole thing just a little too similar for comfort to Billy McFarland’s “Magnises” debacle a few years back? I wonder if part of Aspiration’s plan for “Saving the Planet” will include a festival on some Caribbean island – maybe an IPO / SPAC bash! I hear Ja Rule’s available…

Eric

ESG is the latest refuge of scoundrels.

“Sojourns in Wokeistan” – obvi the title of Scott’s next NYT Bestseller. 😉

Prof G: keep eating the edibles. Loved this. Favourite paragraph:

“A growth-driven valuation can be justified, but for companies with real strategic advantages. I’m not seeing any moats here — just the captain of Aspiration Air Flight 2.1 asking us to look out the left side of the plane and gaze at the bright lights of Wokeistan.”

Laughed (loudly) out loud. On. An. Airplane.

Thanks for making my life more rich.

Gloria

Loved that too lol!

same