$HOOD

$HOOD

Robinhood went public on Thursday, the old-fashioned way — via an IPO with underwriters after a roadshow. The IPO priced at $38 per share, yielding a valuation of $32 billion, and closed its first day of trading down 8.4%. The trading company’s debut is the worst on record among the 51 U.S. firms that have raised as much cash as Robinhood. (Disclosure: I am an investor in Public.com.)

So what will $30 billion buy? At first glance, Robinhood is a roaring success. In 2020 it registered revenue of $959 million, a 245% increase from 2019. RH boasted 18 million monthly active users in March 2021, up from 7 million a year prior. And in keeping with the company’s thesis, “to democratize finance for all,” female users tripled over the past year and more than 25% of users are now people of color, significantly more than at the incumbent brokerage houses.

However … I’ve written before about the problematic aspects of Robinhood’s gamification of investing. The company preys on human weakness, in particular young men’s susceptibility to gambling addiction. That’s still true, and RH’s IPO warrants a deeper dive into the firm’s business model.

What Is Robinhood?

The company operates a mobile app that enables consumers to trade stocks, options, and crypto. These orders are the company’s inventory, which it sells to “market makers” — large financial institutions that pare (execute) the trades in the market. As with Google or Facebook, Robinhood’s users are not its customers, but its supply.

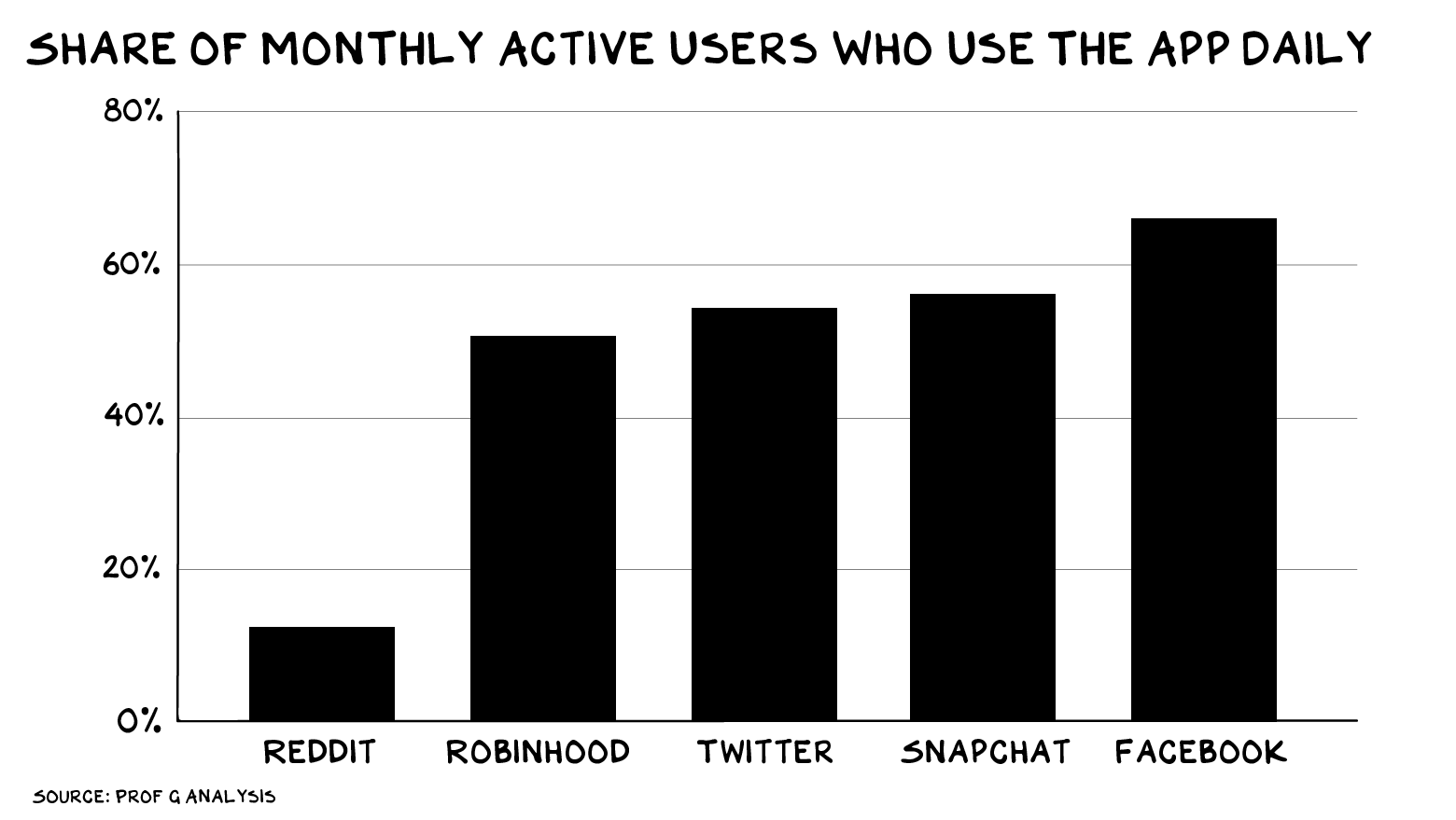

This means Robinhood is incentivized to keep its users trading … a lot. The goal: make stock trading as addictive as social media scrolling. RH has enjoyed success here. The proportion of users who check it daily rivals those of Twitter, Snapchat, and Facebook.

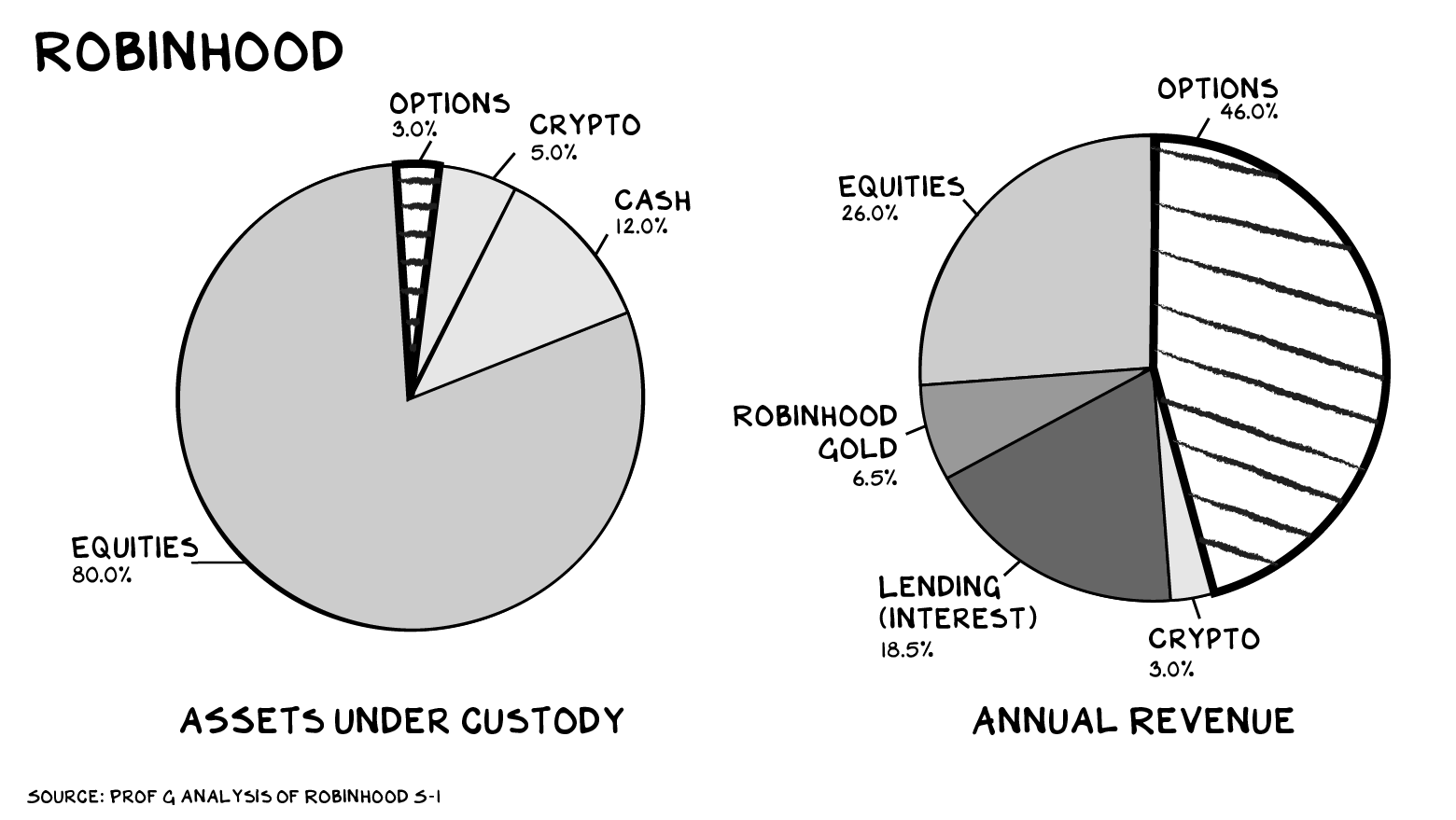

Various financial products drive the company’s revenue, but one is especially lucrative: options. RH makes at least twice as much per options trade than it does on a stock trade. Why? Because market makers pay more for options than stocks. Options trading is less liquid than stock trading, which translates to greater bid/ask spreads for the market makers. RH relies on market makers, and market makers love options. The transitive property tells us the company relies on options, as evidenced by its revenue mix. Despite making up only 3% of RH’s assets under custody, options drive 46% of total revenue.

FYI: Options don’t provide any actual equity in a company. They only let you buy or sell a stock at a given price within a finite period. Put another way, they are 1) highly speculative and 2) risky. RH is more gaming app than investment app. Keep in mind, 43% of its users have FICO scores below 650.

Payment for Order Flow (PFOF)

Robinhood’s incentive to drive investors toward day trading options is not the only fissure between users’ interests and its own.

The transaction at the heart of the company’s model is “Payment for Order Flow” or PFOF. Because RH generates its revenue by selling orders to market makers, it doesn’t charge commissions to its consumer users. But this also creates a conflict of interest for the company, which is motivated to sell orders to the market maker that offers the highest payment for the trade rather than the best price. It’s like affiliate marketing, but for your financial future.

PFOF goes back to the 1980s, when it was pioneered by, wait for it … Bernie Madoff. Madoff relied on the practice to make his firm one of the leading market makers of its day, and when regulators raised questions about whether it presented a conflict of interest, he used his position as the chairperson of Nasdaq to prevent restrictions. (PFOF is illegal in the U.K.) There was no conflict of interest, Madoff assured his colleagues, because “there are very strict rules that I would assume most firms comply with.”

Regulatory Overrun

Robinhood is the latest example of an increasing trend: tech companies for whom illegality is a feature, not a bug. Uber is an $86 billion gypsy cab company. Facebook and Google have received so many fines, it’s likely the companies internally classify them as a cost of doing business. This is tantamount to replacing civics courses with prison training, because … well … that’s how we roll.

For its part, RH has racked up: a $70 million settlement with FINRA, a $65 million SEC fine (for failing to properly disclose PFOF), and a separate $1.25 million FINRA fine. And on Wednesday, on the eve of pricing its IPO, the company disclosed that its senior executives are under investigation by FINRA for failing to acquire broker-dealer licenses. In addition, another inquiry is under way into the possibility that RH employees made illegal insider trades during the GameStop frenzy early this year.

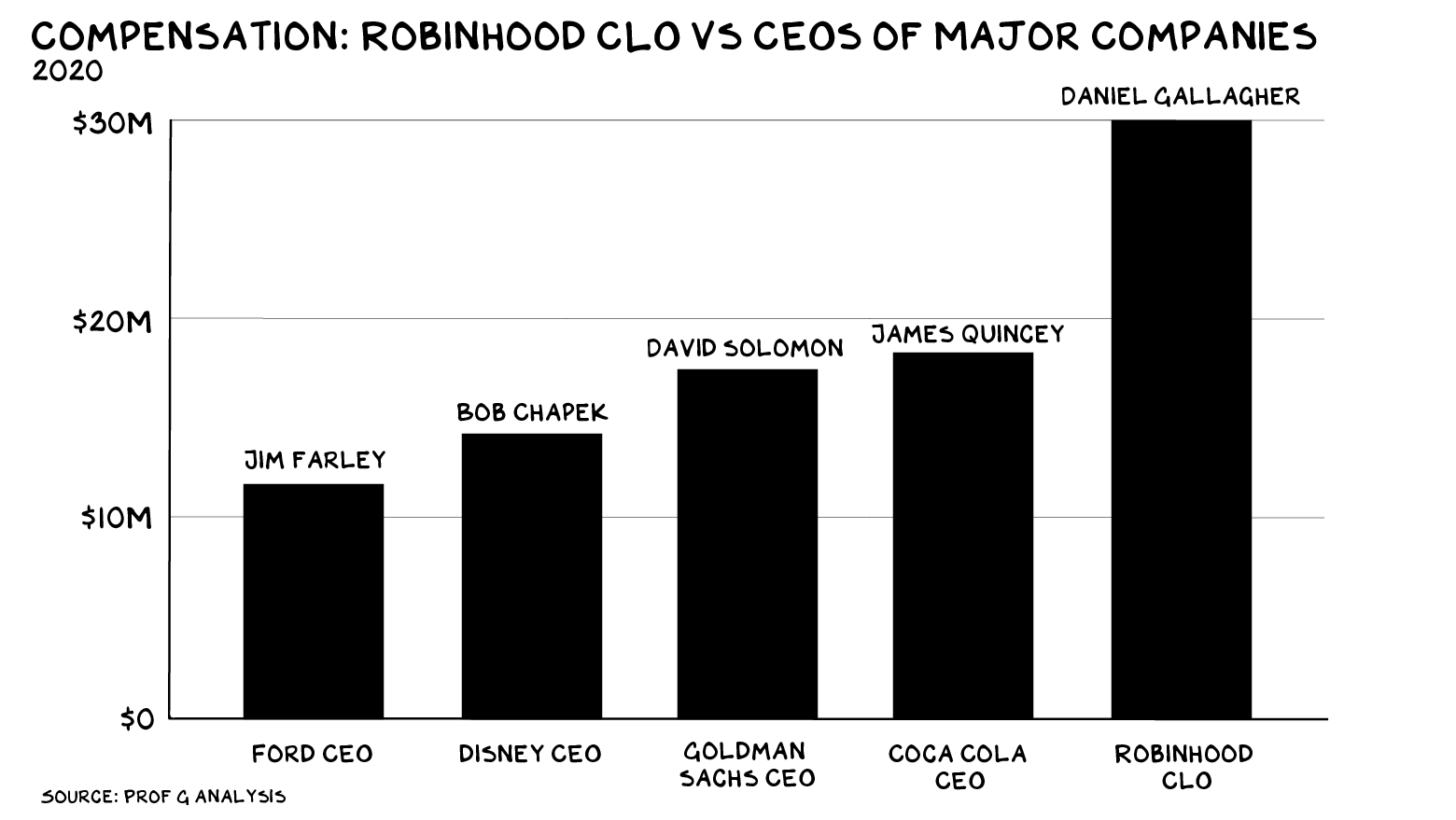

Once, that type of disclosure would have dismembered an IPO. Instead, 48 hours after it made the disclosure, Robinhood was publicly trading at $32 billion. Telling point: The company paid its chief legal officer, Daniel Gallagher, more than $30 million in 2020, even though it hired him halfway through the year. From 2011 to 2015, Gallagher was an SEC Commissioner. Our business environment has morphed from capitalism, which depends on the rules of fair play, into cronyism.

Flouting the law is now a signal to investors that a firm is “disruptive.” Established companies, which believe they have too much to lose, have spent years investing in a culture of compliance to protect themselves. Disrupters, with access to cheap capital and few legacy assets, have no such constraints. In Robinhood’s case, no less an establishment bulwark than Goldman Sachs has blessed its approach to business by taking the lead on the company’s IPO. Forget orange — criminality without consequence is the new black.

The Soul of the New Machine

Robinhood made its “customers” feel special by reserving a third of the offering for them. But the deeper into the insider circle (early investors and employees) you go, the more special (and wealthy) it gets.

In February, RH issued $2.55 billion in tranche 1 convertible notes, which are to be exercised at 70% of the IPO price: That’s $26.60 a share vs. $38. This means the convert buyers saw an instant and guaranteed 43% gain when they woke up yesterday morning. There’s also $1.03 billion in tranche 2 converts that get the same deal. In addition, 27.8 million shares are reserved for future stock-based employee compensation. That’s more than $1 billion reserved, again, for the real insiders.

As for the RH users who were looking to capitalize on their “head start,” the immediate 8% loss will sting. But that’s what happens when your IPO values you at 33x annual revenue. By contrast, Charles Schwab is worth 11x revenue, despite yielding profits 3x greater than Robinhood’s revenue.

Pocket Casino

In practice, Robinhood’s activities look more like the dispersion of financial risk than the “democratization of finance” — kind of like if a for-profit prison claimed to be “democratizing housing.” As both an app and as an investment, RH makes more sense in the context of gambling than investing. Its business model depends on active traders, but research shows the more active traders are, the more money they lose. Likewise, the casino isn’t making much off the blackjack player who sits at the $5 table cadging free drinks, but it hopes the lure of easy money (and the lubrication of those free drinks) will loosen his pockets eventually.

Greater gambling access is becoming a trend. The illegal sports betting market, estimated at $150 billion a year, is rapidly moving to legal online forums. You can now place a sports bet from your couch in 20 states and counting, and mobile gambling apps are reaping the rewards. Since its SPAC listing in April 2020, DraftKings’ stock is up 160%. I don’t have a problem with this, as these firms state what they’re made for: gambling.

Another market that’s benefited from our insatiable appetite for risk? Crypto. Robinhood caught that trend early and introduced crypto trading to its platform in February 2018. Since then, the global crypto market has grown from $450 billion to $1.9 trillion. In the first three months of 2021, 6% of RH’s revenue came from Dogecoin trades. If that sounds like an unstable business model, trust your instincts.

Remedies

Here’s what we’re saddled with: A trend of companies that prey on our financial naiveté, with no regard for law or morality and infinite amounts of capital. What can we do?

First, it’s long past time for the rule of law to reassert itself. Five years ago, admissions to elite universities were awash in bribery and fraud. Then the feds put some wealthy lawyers, investors, and television stars in jail. Did it work? I’d venture that if any parent receives an offer of a “side door” for their kid to get into an elite university today, the parent hangs up, crisply.

Second, we need to arm ourselves, and particularly our young people, with financial literacy. Everyone should be fluent in the basics of markets and how to build financial security. My NYU colleague Aswath Damodaran believes the best regulation is life lessons. Perhaps basic lessons in finance (e.g., not to trade on an app that harvests its orders for revenue) would lessen the pain of these lessons. If we can offer computer science and Mandarin in schools, we should offer courses in financial literacy. The English-as-a-second language course in any capitalist society ought to be in money.

In November 2017, Wisconsin passed a law requiring that personal finance classes be incorporated in K-12 curriculums. In 2019, New Jersey followed suit: Financial literacy education is now required every year of middle school. A start.

But according to PwC, only 24% of millennials have basic financial literacy. Meanwhile, the median age of the Robinhood user is 31. The company is covering its bases with an investing education website, Robinhood Learn, but that does little to nullify the toxicity of its platform.

The federal government hasn’t done enough either. The best the Financial Literacy and Education Commission could come up with was … another website. Its flagship education product, MyMoney.gov, received a whopping 700k page views in 2020 — less than a tenth the number of daily Robinhood users.

We’ve implemented policies in the U.S. that have resulted in a halving of the wealth of Americans under the age of 40 (as a percentage of household wealth) over the past three decades. With so much less to lose, today’s young Americans are justifiably looking for new asset classes and embracing volatility. Put another way, there is cause for a rebellion. The food industrial complex wants you to be fat, social media wants you to be divided, and RH wants you to believe you can get rich quick by day trading. Rebel.

Life is so rich,

P.S. Disruption is hot right now. I’m all for breaking the norms of both financial literacy and education to make them more accessible, and so I invite you to check out my next Section4 Strategy Sprint on Sept. 27. This two-week intensive course is designed to give you the tools you need to up your business strategy game. Sign up now.

36 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

An interesting blog that is full of very interesting information. One potential internal contradiction seems evident though. If RobinHood is appealing to the gambling instinct what use is financial literacy. I am not aware of knowledge, information, or facts having much influence on the predisposition to risky and addictive behaviors. If you have research that demonstrates that literacy can affect risky or addictive behaviors I would be interested to read it.

“But this also creates a conflict of interest for the company, which is motivated to sell orders to the market maker that offers the highest payment for the trade rather than the best price. It’s like affiliate marketing, but for your financial future.”

This part is misleading for an otherwise good piece in my opinion.

There’s no issue whatsoever with the quality of execution at RH, actually their clients generally get a better price than routing directly to the exchange (Matt Levine of Bloomberg wrote a good explanation back in Feb about PFOF)

The only case against brokers churning practices is that they are … controversial/unethical, but really you cannot protect people from themselves.

If they want to YOLO weekly call options, who are you SEC to stop them. People have rights (sacred statement in US I guess) and a very important one is the right of being stupid.

Scott:

Great perspective and an eloquently delivered position as always.

My own thought is: RH is a very very young brand.

Call it dispersion or disruption, they’ve pioneered this category- living on the edge as a company- and delivering excitement and friction-free market participation to their users.

BUT: users will grow up. Will learn their way. Will express volitionally their changing needs. (more asset classes, more transparency, whatever..). In fact, the investment mindset for new investors may be primarily about today/now/instant and not a multi-decade view.

So as its users change and grow RH, to survive and GROW and thrive, esp with competition (Pubic/ Webull, etc) will have to change and grow up.

i do see this as a moment in time.

Thanks for this, financial literacy truly is lacking. Unfortunately, the world has always run on cronyism. People are just starting to say the quiet part out loud.

Thanks for this

Great piece, and your positions are commendable. However, whatever happened to holding individuals responsible for their own behavior? It is indisputable that RH is gaming the regulatory systems, both legally and illegally (currently), by gamifying trading, but nothing is forcing its users to take the actual steps of engaging with it as much as they do but themselves. Users who have access to all of the information you set forth. So they either are aware of it or don’t care and still engage with the RH platform as they have been. To assume that it is yours or our responsibilities to convince them to behave as we have chosen given all of the information you have set forth, i.e., not trade like trading is a video game, is patronizing all of those persons. They have obviously made their decisions and/or chosen not to suss out the truth, which is their prerogative–my position has always been it is not one’s responsibility to “protect” others from themselves, which is neither relatively right or wrong, but simply a position, as yours is. The potential insider-trading allegation set forth above a side, the bottom lines are these: current regulations promote initial investment structures to advantage those with access to them, i.e., those “accredited investors”, governments have long given the potential – growth advantage to, and those yet to attain that status remain relegated to the much less profit- potentials of investing later in companies’ life cycles; and, the illicit actions of these companies are not being dissuaded by their respective law’s or regulation’s enforcing bodies to a degree which would curb them–whether those laws were regulations be right or wrong is immaterial at this point, they simply are the case right now. Thus we on the outside are left with these actual options: 1) vote and/or petition and/or lobby lawmakers and regulators for more enforcement and tools therefor, 2) create a platform that embodies the ideals aligned with trading parity and hope a user-base shift to it from the RH’s of the world; or 3) take our parity ideals and it’s offshoots to a territory wherein a new Constitution in alignment with them can be instituted (which is not as radical or as difficult as it sounds–and, no, I am not just blowing smoke, I have actually taken the time (over a year) to sit down and devise such a governance: A Just, Egalitarian, Equitous, Socialistic, Capitalistic Representative Democratic Republic

Interesting perspective about folks who should know better having the free will to act this way. Never though of it this way. Idiot tax.

Well said im learning more and more as i go…

I don’t understand the hate against Robinhood. To say that the market is more risky on Robinhood than public or any other platform is dishonest. I just can’t understand the hate its so ridiculous. I have multiple brokerage accounts for different purposes and I hear people being apologetic for using Robinhood how stupid is that. If it’s gambling on Robinhood it’s also gambling on public. If the stock market is too volatile for you then encourage people to invest in lottery tickets. That would be a whole lot less volatile than gambling in the stock market.

Because, Robinhood lies that it’s cheap and they are gamifying investments on purpose. Also, they don’t properly disclosure material information.

It’s easy, Sir, RH are violating each and every ethical standards the industry has.

Fuck Robinhood.

I’m not on Robinhood and certainly didn’t buy their stock, but I do have a question about their model. If trades are free, and payment for order flow is disallowed, how do brokerages make money? I have accounts with TDAmeritrade, and trades are free there too. I have no clue how they make money, but I assume they do or they would be out of business. Can anyone tell me how this works?

They all use PFOF plus a number of other revenue streams. (If they don’t its to for promotional purposes) Think or sswim TOS was built by the Tastytrade people and its funny they encourage you trade small trade often yet you hear nothing about how criminal that is. I’m guessing its because tastyworks is not free. I think maybe TOS might have commissions on options and futures and things. RH don’t offer futures. Most of them lend stocks with interest to short seller. Short selling is when you borrow someone else’s shares to sell to the market in hopes to buy them back at a cheaper price and the borrower has to pay interest on those shares. Can’t short on RH. Brokers also earn interest on margin they borrow to investors(gamblers) and on uninvested cash.

Others may offer various subscription services. I like Tom Sosnoff he never says anything bad about RH he actually commends them for accomplishing what he was trying to do for 40 years.

First, one of the reasons TDA was purchased by Schwab is that TDA didn’t have other sources of revenues to fall back on when trading became “free”. Here are three ways (besides PFOF) these firms make money. 1. Lending — either “margin” lending, meaning allowing you to use your securities (custodied with them) as collateral to buy more securities and charging you interest on the amount lent. 2. Proprietary securities — Most of these firms have their own funds (mutual and/or ETFs) that receive a fee when you if you buy them. 3. Banking — Schwab has Charles Schwab Bank, which accepts deposits and makes loans upon which it charges interest. The parent company, Charles Schwab, makes money when funds in Schwab brokerage accounts are deposited into Schwab Bank. Schwab advertised that its Intelligent Portfolios robo-advisor accounts had zero fees, while in fact it required a portion of all funds invested (at least 4%) to go into Schwab Bank which paid nominal interest. Many believe this is why Schwab recently said it has set aside $200M to pay for possible SEC fines. When Toronto Dominion Bank bought Ameritrade the agreement was that profits from Ameritrade funds invested in TD Bank go to the Bank, not TDA, so they couldn’t benefit the way Schwab could.

Scott always has interesting things to say. I am always fascinated by how he delivers a message which does not sugar coat. I am working out how to truthfully talk to students. Clients seem to like a direct message.

Agree the rule of law, esp. In securities is failing. SEC is a joke now. Also agree that most are challenged when it comes to financial literacy. Plus all the young people want to get rich quick so they can drive a Bentley like the rappers they follow on IG. They grow up delusional

Agree with the general sentiment, but I think the data point about 43% of Robin Hood users have <650 FICO might be difficult to back up—it’s from a study conducted by the company Stilt _of their own users_, whom I don’t think can be thought of as representative of Robin Hood’s entire user base.

They don’t include this detail in the headline, but it’s clear in the ‘methodology’ section:

https://www.stilt.com/blog/2021/02/robinhood-low-fico-users-2021/

Once again, thanks. Hard, blunt and to the point.

Gambling, in all forms, is the next level of dependence for our society. But now, it is supercharged with the help and approval from our Government. RobinHood is the most blatant, but so is Lotto.The SEC is where? When you look for who benefits, the same names that we see associated with the DNC/Left – academia, sports personalities, Hollywood, Hedge Funds. Most fund Pelosi and Company. They seem to avoid jail for actions that should put some of them there. Musk, RH, Hunter, etc. Along with Trump and Hillary if you wanted you actually dig deep. In the past we blamed big Tobacco for ills, and the DNC/Left drove them to BK. Guess the government has switched sides, as there is too much money to ignore.

You had me right up until the shill for Galloway University:)

Oops.

Every new online company needs to feed an addiction to succeed. My young kids are on Tik Tok. Half the planet’s on Facebook. Pot is barely legal and even that is in the air, all over the place. Guess that’s addictive too! The point is, they all figure out how to increase our habit forming behaviors in order to make money for the: a. owners b. stockholders c. government. The bigger picture: the Development of Capitalism in the 21st Century. Or rather, in the Third Millennium! The theoretical democratization of investing at the expense of professionals and banks in general: isn’t that progress?

Hi Scott…..Love the piece. But “compared to what”? I have no quibble with your report, but isn’t it true that rebates for trades are how all the brokerages make money? I make several thousand trades a year at a cost that is more than 99% lower than I would have paid several years ago (mostly writing options). This allows me to make a profit where it would have been impossible years ago.

I did a test between HOOD and Schwab (that’s where I do most of my trading) and note that Robinhood shares none of the rebate with me, whereas I almost always get a split on stock trades with Schwab and often get better than the bid price when I sell options.

My point is that I am happy with the current system (which Gary Gensler is looking at). The problem with HOOD, as I see it, is not that they get paid for order flow, as all brokers do, but that they gouge the very clients they are claiming to help. Regards, d.

Thank you Scott. I just signed up to receive your email several weeks ago. I thoroughly enjoy your insight, opinions, and straightforward approach. Keep them coming and have a great weekend!

That was great ! Enjoyed nearly every line of the blog –

Finally someone that can tell the truth about all the BS that goes on in this world –

Scott, good blog. I have disagreed with many, but in sync here. One comment… while your call for ‘financial literacy’ is valid, how? Do we think the ‘average’ teacher in public K-12 even has any financial knowledge? At the State level, California would turn ANY financial curriculum into a Marxist/Leninist lecture, and throw in CRT. My son’s HS ‘econ’ class textbook was a much discredited ‘get rich quick’ book. I CPA friend offered to create and help deliver a basic ‘consumer econ’ class for a local school. Teachers Union blocked any outside ‘experts’, demanded that a teacher be trained on the clock. In the real world, we welcome outside experts, as students/employees respond much better. In the world of Unionized education, it is more likely the teachers are preaching Robinhood than warning against such schemes.

So in the interest of charting a feasible & valuable path forward here…if I take these issues as a given, what’s the specific resolution?

What is the specific claim here that is most relevant here? Is it that PFOF for transactions made by non-accredited investors ought to be inherently illegal? Is it that Robinhood’s existing violations did not receive fines proportionate to their damage to individuals or society? If Robinhood (which, given retail investor volumes around Restoration Hardware, is best not-referred-to as RH) is a business that inherently profits off of social harm – i.e., that in a broad qualitative sense the unit economics of its business do not make sense except in a world in which it directly or indirectly profits off the predictable (even if self-inflicted) suffering of others – then what is the most narrow and defensible way by which Robinhood pursues that end in a way that is the result of its deliberate actions, done with full knowledge of the consequences, while doing harm to individuals in a way that cannot be explained away by an investor’s right to lose money?

I ask this in light of the inadequacy of the recent antitrust case against FB, in which the case was doomed from the start due to the prosecution’s astonishing inability to discretely define FB’s status as a monopoly in any way that was concrete or had legal relevance. The fact that the case was filed, and my casual reading of the judge’s response, suggests that current legal frameworks support a viable case against FB…the prosecution simply didn’t do a good enough job (in this first pass) of making that case.

While it may be interesting and exciting to highlight the fact that these companies are, broadly, harmful to society – and it is a point that is, broadly, argued well here, that is all talk until it is paired with either (1) a concrete, substantive legal challenge that forces these companies to defend their behavior, its implications, and the knowledge of those implications or (2) an aggressive government willing to change the laws sufficient to make these companies’ actions so obviously illegal they cede ground despite the impact on their owners and investors.

Seems to me so much of our collective hope and effort is focused on #2, which is (A) indirect and easily disrupted in its impact, (B) not a directly accessible lever except by those who already impact politics and (C) at best, active on a very extended timeline.

So my question is, how thoroughly has the viability of option 1 been vetted? And if somebody did want to bring a case against Robinhood, what would the basis of that case be, what would undermine it, and what would strengthen it? I don’t think this is an abstract exercise.

Like. TY!

+1

This is why these companies on the edge of regulatory compliance are successful and unstoppable. Nobody is going to jail. And nobody is taking them to court.

Scott, this just might be your best piece ever.

Why not do an email some of the basics of what you’d like to see as part of Financial Literacy? Even a list of topics would be helpful. I think I know all the basics but I want to make sure I’m not missing anything. This is definitely something I wish someone had done for me when I was 27 — and I’m trying to do it for some 27-year-olds now.

https://www.youtube.com/watch?v=uNrjrDV9-YQ you’re welcome

I thought it would be interesting to point out that Mr. Gallagher’s stock-based compensation of ~$24m is actually based on the shares being priced at $16.33 (according to their S-1) as it was prior to $HOOD becoming public. Since the stock is trading at ~3x, his stock based compensation is considerably more.

Thanks, Scott. I was on your investing seminar yesterday (thanks, again), where (pretty much at the end, but still) I learned that I was following the right path and was correct in trying to instill it in our daughters (28 and 31): if you’re not working, hard, to understand the intricacies of the market don’t think you can buy/sell on your own. Hire a pro and invest for the long term.

The older daughter works in a charter school in a low income part of Philly. We’ve often talked about how financially illiterate her students are, through no fault of their own. They live in a banking desert, surrounded by an under-the-table cash economy (w/plenty of illegal, cash drug sales and potential income, to boot), if they’re fortunate have working parents who’re likely not making enough to save, let alone invest (assuming someone taught/convinced them of the value of same, years ago), and rarely if ever travel outside of their neighborhoods. It’s a depressing scenario that contributes to income inequality big time. Financial literacy should 100% be taught in our schools, all of them.

Agree. The SEC should give every IPO a grade, related to the level of risk. For example, a high risk IPO should clearly be marked with a red flag and a probability level of losing your principal. Robinhood should be rated at the highest level of risk possible, similar to a biotech. Nothing wrong with investing in it, as long as the investor knows the risk level.

The free market determines risk. Not some overreaching government entity. Let people get experience there’s absolutely no substitute for it.