Unicorn Feces 🦄💩

5-min read

Season 1, Episode 1: SoftBank and Real Estate

Last night I met up with friends at Soho House, a members-only club. I’ve always wanted to be a member, and have several friends who’ve offered to sponsor me. But the thought of being rejected for membership by a club where all my friends are members is damage my ego couldn’t endure. So, no membership for the dawg. As a guest, I’ll have a nice meal and a couple Maker’s and Gingers (i.e., 5). I’ll then go home and decide the smart thing to do would be a preemptive strike against my member-like hangover, so I’ll ingest 32 ounces of water, 3 Advil, and a hit of my dosist sleep vape. I’ll then watch the last 2 episodes of Succession and get 4-5 hours of sleep.

Thursday. Night. In. NYC.

I’m going on Barron’s TV (yep, that’s a thing) Friday morning to discuss Tesla (which I believe is overvalued), Amazon, and Apple. As I don’t rave about the stock, on the subway back I’ll learn via Twitter (where technology meets hate) that I’m an idiot, not a real professor, and hard to look at, from handles that are some version of @Teslalong. I’m fairly certain there are more fake Twitter handles managed by Tesla longs than the GRU.

Note: If it sounds strange that I’ll be going on TV possibly still drunk, keep in mind the show is broadcast on Fox. Most of their anchors seem high when they broadcast.

I’ll also avoid making any important decisions Friday. When I have a member/guest hangover, my judgment is impaired. This poor judgment is predictable and can be reverse-engineered to a pattern: alcohol, marijuana, lack of sleep. So, where else could we apply pattern recognition to predict what might happen in the markets?

I know, let’s talk about WeWork.

The pattern of tectonic plates grinding: SoftBank, real estate, red flags. Where else can we discern the kind of plate collision that leads to an earthquake? (Note: especially proud of the seismology metaphor in the previous sentence.) Btw, best movie involving a guy who could predict earthquakes? Phenomenon.

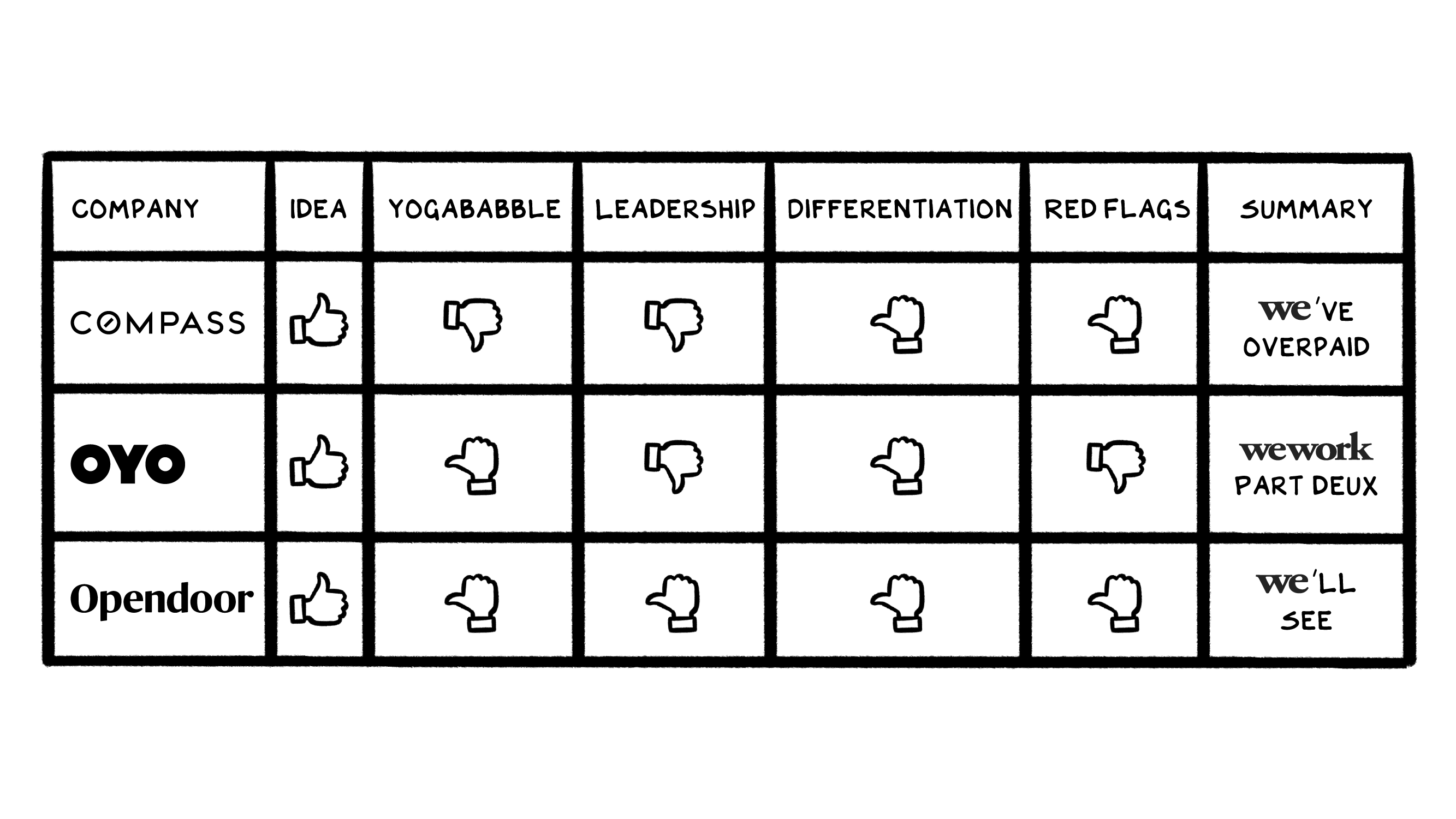

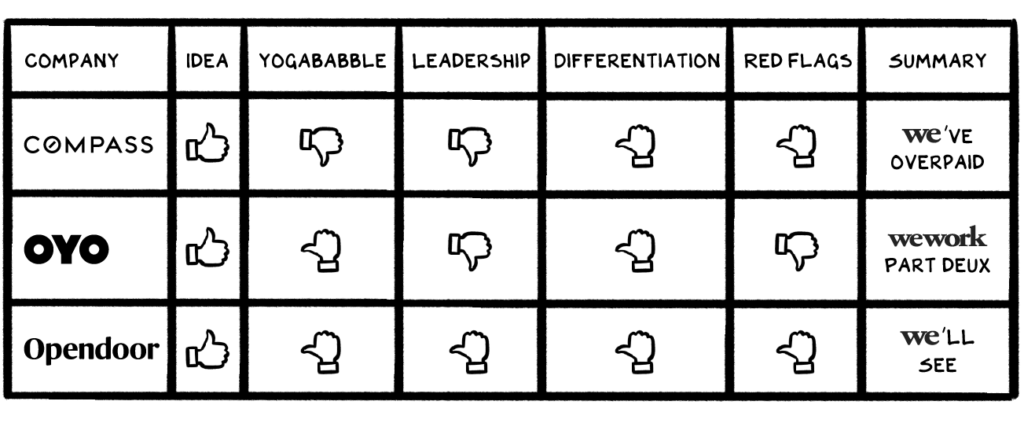

What earthquakes are to California, SoftBank is to real estate unicorns:

Compass

Business model

- Use technology to pair top brokers with home buyers

Yogababble

- “To help everyone find their place in the world.”

Funding

- SoftBank investment: $600 million

- Total funding: $1.6 billion

- Valuation: $6.4 billion

Differentiation

- Proprietary technology and 19% of non-broker employees work in “technology”

- Highest Glassdoor rating (4.3) for real estate companies

- Has acquired 14 other brokerages

Feces (red flags)

- Yogababble

- C-Suite turnover is a sh*tshow: includes the CFO, COO, CMO, CTO, CPO, General Counsel, Head of Product, VP of Product, and VP of Communications

- Capital masking as growth (some brokers receive entire commission, with nothing going to Compass, for their first 8 deals)

Summary/prediction: Strategy makes sense, and they are buying real assets. The SoftBank effect (drunk capital) likely means they have overpaid. Value will decline, but not implode, making it one of SoftBank’s better real estate investments.

OYO

Business model

- Buy or franchise run-down hotels, fix up, train staff, and take a commission (25-30%)

Yogababble

- “To offer tasteful spaces, whenever you need them, at unbeatable prices.”

Funding

- SoftBank investment: ~$1 billion

- Total funding: $1.6 billion

- Valuation: $10 billion on $200 million in revenues (50x revs)

Differentiation

- Improving fallow assets (old/out of date hotels)

- No global player for budget hotels

- Uses a tech platform to help hotel partners with distribution

Feces (red flags)

- Bought Hooters Casino in Las Vegas for $135 million (sold for $54 million 4 years ago, signal of overpaying)

- Leadership: Ritesh Agarwal — 25, first venture

- Lightspeed Ventures and Sequoia Capital getting out of dodge: selling 50% of their stake for $1.5 billion

- SoftBank (and founder) putting money in: Ritesh Agarwal invests $700 million in latest $1.5 billion fundraising round with Softbank helping to fund the remainder

- SoftBank has been a lead investor in every round since 2015 (smoking own supply)

- Reviews = sh*t

Summary/prediction: OYO feels like the WeWork of budget hotels with red flags the size of Days Inns. A 25-year-old founder and SoftBank is a toxic mix. Yes, the Zuck and Bill Gates founded their firms at the same age, but it’s a bad strategy to assume your CEO is the next Zuck/Gates. Founders buying additional shares is a good sign, unless you are 25 and borrowing against your existing shares to buy more. That means he’s hugely committed and immature.

Lightspeed and Sequoia also have too much capital and are under pressure to deploy additional money in portfolio firms where they’ve negotiated pro-rata investment rights for subsequent rounds. With OYO, they not only passed, but having the full inside information and observing the CEO, they’ve decided to sell shares. Customer feedback is awful, and customer acquisition does not appear to be scaling. Here. We. Go.

Opendoor

Business model

- iBuying: sell your house to Opendoor in less than 24 hours in all-cash deal; firm collects service charge, resells house, and offers financing to a captive market

Yogababble

- “To empower everyone with the freedom to move.”

Funding

- SoftBank investment: $400 million

- Total funding: $1.3 billion in equity and $3 billion in debt

- Valuation: $3.8 billion

Differentiation

- Provide immediate cash to homeowners

- Hugely inefficient market ripe for disruption

- Compelling value proposition (liquidity in traditionally illiquid asset class)

Feces (red flags)

- Management and board have little real estate experience

- The risks of iBuying are substantial in a downturn

- Can algorithms replace nuance of valuation in real estate?

Summary/prediction: A compelling value proposition in a market that’s hugely dislocated/inefficient. Without knowing average hold/margin on properties, difficult to assess. In absence of this data, feels like a levered bet on US real estate market.

The Bigger Story

The business story of the month is WeWork’s meltdown. The bigger story will be SoftBank’s Vision Funds impairment. Earlier this year, we predicted the 2019 IPO unicorn class would lose money — YTD it’s up 5%, vs. 13% in 2018 and 94% in 2017. The 2020 story will be a 50%+ decline in the value of privately traded unicorns. The world is not as impressed with Silicon Valley as Silicon Valley is with itself.

An 11-year expansion, cheap capital, and investors chasing a Facebook/Google high have resulted in an environment that is not “different this time.” People love WeWork and Uber as I loved Pets.com and Urban Fetch. A 60-pound bag of dog food and a pint of Ben & Jerry’s delivered next day/hour for less than cost was awesome, except for shareholders. Value is a function of growth and margins. Many/most of today’s unicorns have deployed massive capital to achieve the former while not demonstrating the patience or skill to achieve the latter. Record deficits during full employment are irresponsible, as is capital-driven growth meant to create the illusion of innovation.

There is also a bigger fault line. In 1999 I was 34 and running an e-commerce incubator (Brand Farm) backed by GS, JPM, and Maveron. I mistook my good fortune — being born a white male in sixties California — for talent. My money/success was a virtue that gave me license to demonstrate poor character and a lack of empathy. The market had a swift and effective immune response to my ailment.

There is, again, an epidemic of hubris that has rendered the Unicorn Industrial Complex a hot zone.

The good news? The antidote is imminent.

Life is so rich,

P.S. We’re working on a new project (and are hiring) — sign up for the announcement at section4.com.

27 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

FB should NOT be broken up–it should be nationalized. The Gov’t should control the infrastructure of the public conversation, just like the “real” infrastructure.

That sounds super scary

Boeing, next. Never has a company had so many moats that protected it from markets and reality. And from that ivory tower, they can watch their planes crash.

Please do the health/tech space next

Oh Professor, you speak nothing but the truth. Sleight of hand anyone? How about a review of Cargo the stale snack provider to those who frequent rideshare?

Love the way you mix humour with substance !

Yo missed Katerra

Exactly.

Another great read, Scott. I’m looking forward to what your next project is with Section4 – wishing you and your team continued success.

Great read, thx!

Thank you for your thoughtful analysis of the Vision Fund and the lunacy going on at SoftBank and the unicorn world in general, I hope to see some serious repercussions soon for SoftBank and the fund!

Why do you think Softbank’s investments are so over-valued ? Do you think Masa is not capable for this ?

Love this guy. One erudite witty son of a gun.

Scott, did you put money where your mouth is and short the WeWork bond? no financial advice taken

How do you short private equity? Is there an instrument for that?

What do you think of Clutter?

Dont listen to them Scott. You are a very attractive man.

Loved you on Bill Maher/Realtime! 🙂

There’s a point in a successful business operator’s arc where you can just “see it”. That you can see the next right move and effortlessly take the step. It could be picking the right investment or selling the right product. Nonetheless, save your money. Things will change. But good luck anyway with your new venture. I had a client at 72 Spring Street 20 years ago. She was on top of the design world and could write her own check. I think she lives in her mother’s garage now.

Scott, would love to see your take on another crazy (so I think) W-story: Wayfair.

Scott, thank you for saving us from the Pump (by VCs) and Dump (on the institutional & retail investors) system perfected by Blue Apron. What you (and everyone else) missed is the “Bypass IPO” route taken by Harry’s – a $1.4B liquidity event circumventing the SEC. Now Harry’s is part of Edgewell Personal Care – total Market Cap $1.7B. The acquisition was justified as a means to get “creative talent” and fresh branding ideas. I could have given them the phone number of several creative agencies, including the one behind Harry’s and other current brands, for a whole lot less money than $1.4B.

WEagree

It feels like the over-exposure to ease of communication allows for the tail to wag the dog at an astonishing rate. With all of these unicorns finding out that growth at all costs is a nearly impossible way to drive a business in a time where new competitors can pop up within months and disrupt the market – Do you think a larger push towards business fundamentals will be the next wave? I hope so…

Scott, thoughts on the challenger banks in Europe? They almost have the same ingredients as WeWork – poor corporate governance, over confident founders, overvalued, and negative gross margin business models.

An honest review of N26, revolut & co would be dope.

You really nailed a NYC Thursday Night….also thanks for always making my Friday Inbox better! Cheers to you, Scott!

I wish you would stop doing these analyses. You’ve already prevented me from shorting WeWork, now you’re after Compass and OYO too? It’s not fair