The Grown-Up Tax Bill

The Grown-Up Tax Bill

Audio Recording by George Hahn

Next week the Republican-led Congress plans to move President Trump’s Big Beautiful Bill one step closer to law. The most recent CBO analysis factoring in interest rates, inflation, and economic growth put the cost to $2.8 trillion. Democrats have criticized the bill but haven’t offered alternatives as they live up to their signature “right, but ineffective” brand. Not offering a contrasting bill is a missed opportunity. So here’s my plan to reduce the deficit gradually, increase investments in future generations, and maintain economic growth. (Note: While healthcare and defense are ripe for cost-cutting, I’ve left them out of this analysis, as those are posts for another time.)

Bipartisan Hallucination

Economists frame the trade-off between defense spending and social welfare as guns vs. butter. As spending on guns increases, there’s less money for butter, and vice versa. That’s the theory, anyway. In practice, the GOP believes cutting taxes is the best strategy for growth (it isn’t), and Democrats believe the government can fix social ills by throwing money at problems. So, in the sole act of bipartisanship that endures, we cut taxes and increase spending, resulting in massive deficits that amount to deferred taxes on the young. The result? The federal budget’s fastest-growing line item isn’t defense or entitlements, but interest on our debt. So, raise taxes or cut spending? The answer is … yes.

Three Choices

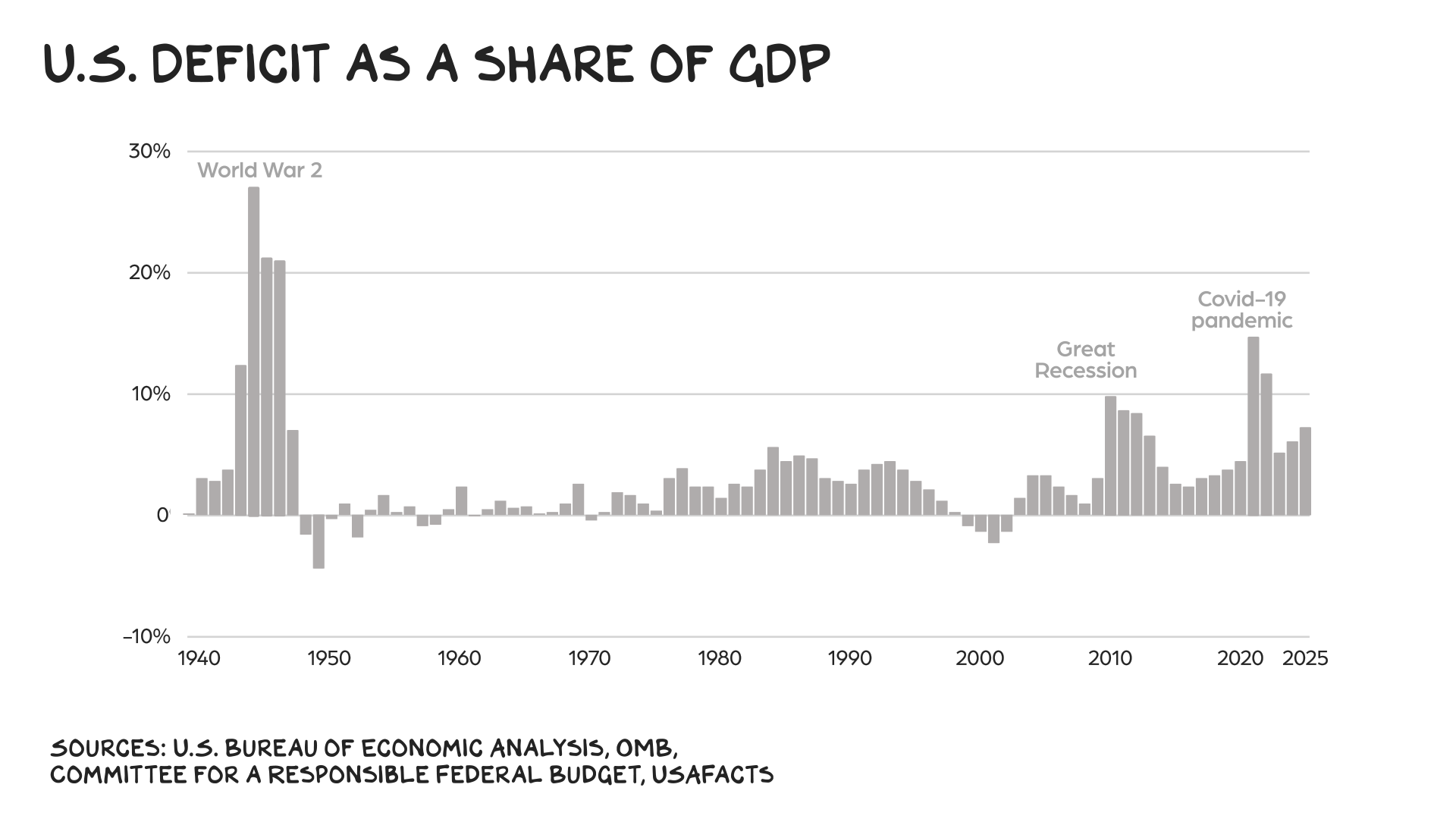

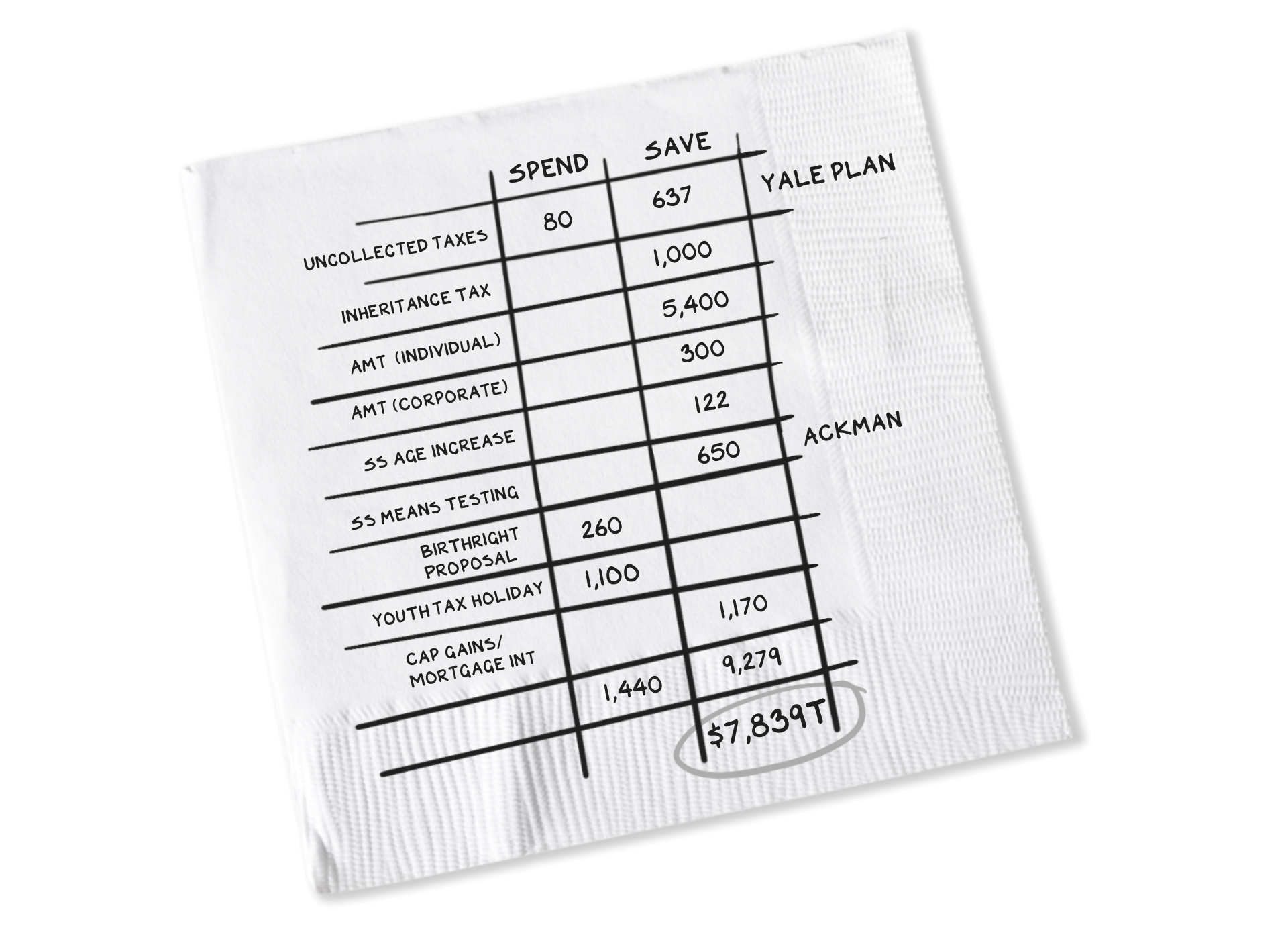

A budget involves three variables: time (costs and opportunities left for future generations), people (redistribution), and values. On my podcast, University of Michigan economics and public policy professor Justin Wolfers told me the question isn’t whether a budget increases or decreases the deficit, but what is the right level. “The basic logic is we should stash away a bit of money when times are good, so we can splash cash when times are rough.” Our current deficit-to-GDP ratio is 6.4%, meaning we’re spending money as if we’re combating a pandemic or the Great Recession. Instead, we need to run moderate surpluses that don’t stifle economic growth and/or budget deficits that are below the forecast for GDP growth. Some back of the envelope math: To reduce our deficit-to-GDP to a 1% target over the next decade, we’d need spending cuts and revenue increases that net out to approximately $150 billion, or less, in annual deficits.

Money on the Table

The tax gap is the difference between the amount of taxes owed and the amount collected on time. According to the most recent IRS data, the tax gap in 2022 was $696b, meaning we’d make significant progress on our deficit-to-GDP target simply by cracking down on tax avoidance. Biden’s Inflation Reduction Act (IRA) put us on that path. According to an analysis from the Yale Budget Lab, its $80b increase in IRS funding over 10 years (since rescinded) would’ve netted $637b in revenue over that period. Another analysis by Larry Summers and Natasha Sarin estimated that restoring tax compliance efforts to historical levels could generate over $1 trillion in the next decade. Neutering the IRS amounted to the most regressive tax in recent history: Lower- and middle-income tax returns are simple and easy to audit/enforce. However, the explosion in the tax code from 400 to 74,000 pages over the last century created an obstacle course that must be run at night. Wealthy households have experienced navigators (tax lawyers, advisers, etc.) to guide them. Reducing the agency’s staff is a conscious decision to not enforce the tax code for the wealthy. We’re gutting the fire department during wildfire season to save water. It’s not stupidity — it’s a(nother) conscious decision to transfer wealth from poor to rich as the effective tax on the wealthy plummets.

The lion’s share of uncollected revenue ($381b) would come from individuals, unreported employment taxes ($111b), underpayments ($80b), and non-filings ($53b). One paper estimated the top 1% of earners are responsible for nearly 30% of unpaid taxes, as high earners incur greater tax liabilities, and their income tends to flow from opaque sources that aren’t subject to third-party reporting. According to Summers and Sarin, every dollar invested in audits returns $7 in revenue. But since 1960 the audit rate has fallen from 3% to 0.36%. To paraphrase the bank robber Willie Sutton, audits are where the money is. According to a GAO report, AI could help the IRS deploy its limited resources to identify suspect returns, understand complex audits, and free up staff to improve customer service.

Dynasties vs. Decency

One of the most offensive provisions in Trump’s Big Beautiful Bill is a permanent increase in the estate tax exemption to an inflation-indexed $15m, per person — letting couples pass $30m to their heirs tax-free while slashing food stamps. We’re opting for dynasties over decency. Good governance is implementing taxes that are the least “taxing.” That’s the basis for a progressive tax system — I can more easily endure a high tax rate than a special needs teacher making $40k. Vastly reducing the inheritance exemption is likely the least taxing tax that could raise substantial revenue. Your kid inheriting $7m vs. $9m won’t hurt. I know a lot of rich kids. The very rich are no happier than the rich; there are diminishing returns to happiness above a $200k annual in income. My proposal: Drop the exemption to $1 million and tax inheritances above that threshold at 40%, without loopholes. That would raise an estimated $118b in annual revenue, or more than $1 trillion over a decade.

Alternative Minimum Tax

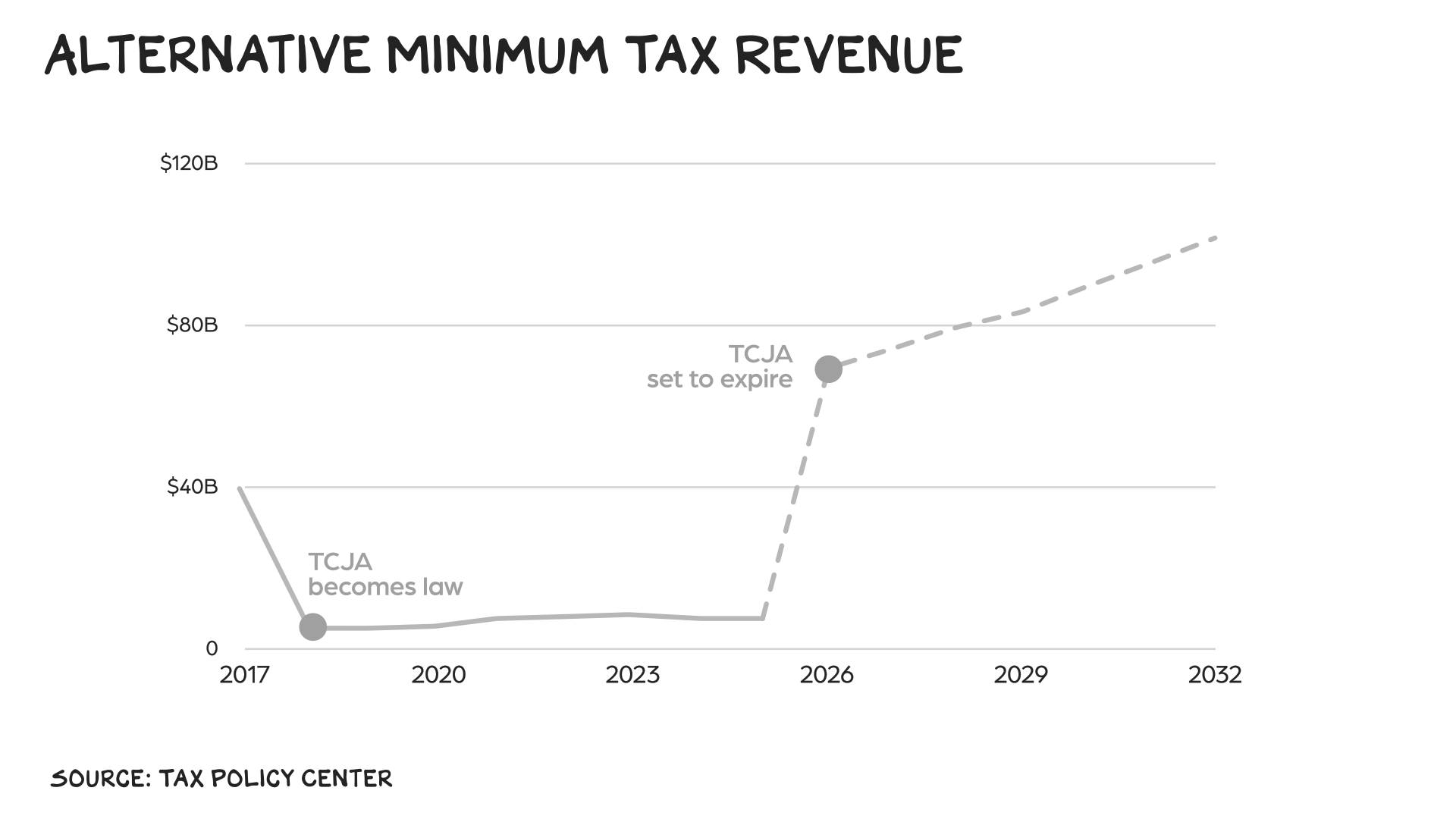

In 1969, Congress learned that 155 taxpayers with incomes exceeding $200,000 (nearly $2m today) had paid no federal income tax in 1966. Representatives received more constituent letters about these 155 taxpayers than about the Vietnam War. In response to that outrage, Congress created an early version of the alternative minimum tax. Over the following decades, Congress tinkered with the AMT, but the basic idea was to compare an individual’s income before and after they claimed certain deductions and dove into the torrent of loopholes inserted by lobbyists.

After a portion of their income is exempted, the taxpayer must pay tax on whichever amount is greater. The 2017 Tax Cuts and Jobs Act didn’t eliminate the AMT, but it limited its scope, dropping the number of taxpayers affected by the tax from 5.2m to 200k. We should bring back the individual AMT with a $1m threshold taxed at 40% and a $10m threshold taxed at 60%. If 60% sounds high, historically … it isn’t. This would raise $540b in revenue per year, while only affecting the top 0.2% of filers, or about 275k taxpayers, according to my back-of-the-envelope calculation. We could also do nothing, as the TCJA’s assault on the AMT is set to expire this year if Congress doesn’t act.

Eliminate the Youth Tax

Lower long-term capital gains rates and mortgage interest deductions are nothing but a transfer of wealth from young to old, poor to rich. Who owns stocks/homes? A: The old/rich. Who rents and makes their money from a salary? A: The young/poor. Eliminating the capital gains tax deduction (taxing windfalls at the same rate as ordinary income) and the mortgage interest deduction would add $117b/annum to revenue.

Corporate Citizens

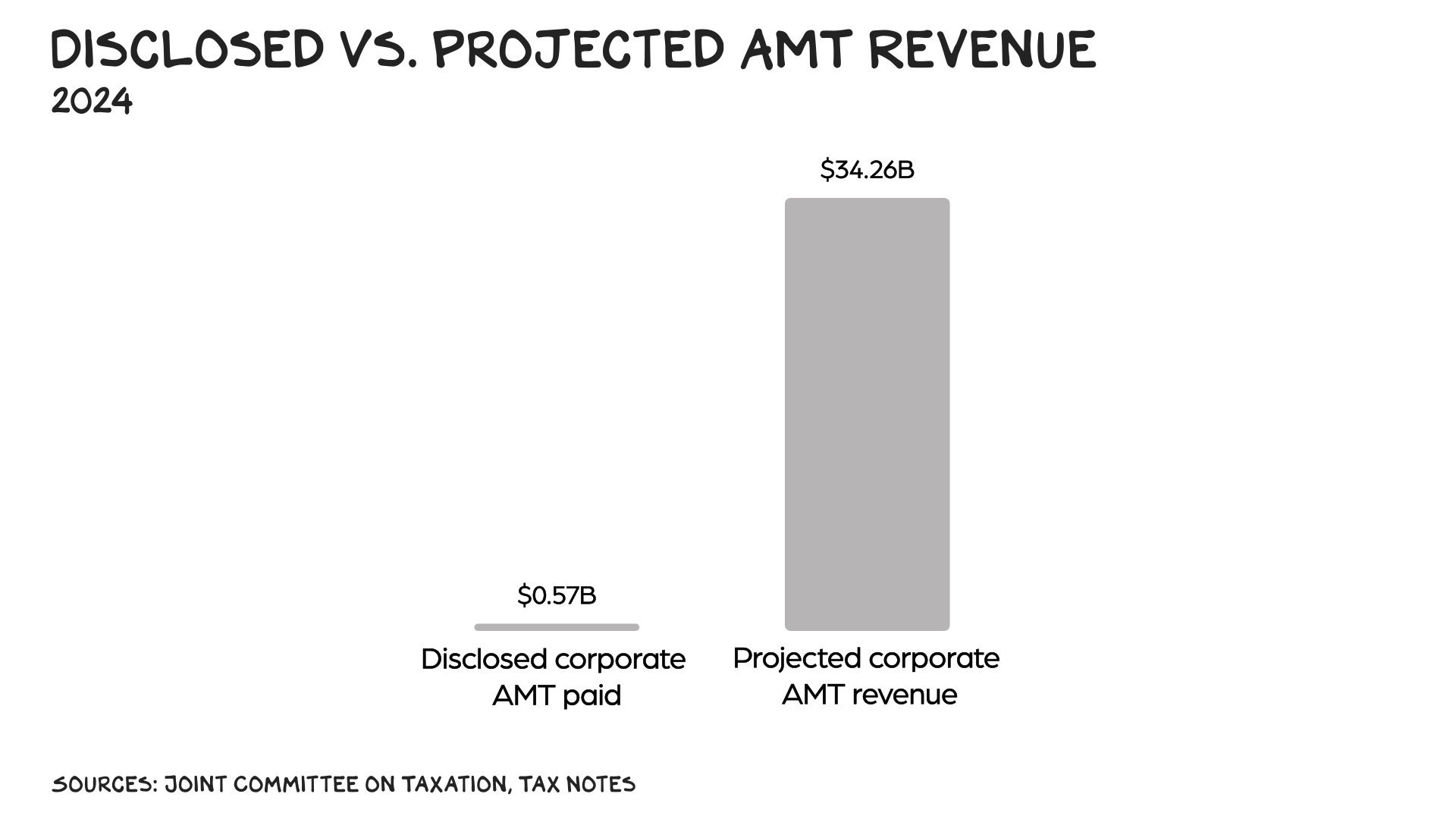

How many lobbyists does it take to change a light bulb? A: None, as they prefer to keep everyone in the dark. In 2024, U.S. businesses spent $4.4b on lobbying. It may be the greatest ROI in economic history. One study found that lobbying connected to a 2004 law that created a one-time tax holiday for repatriated profits delivered a 22,000% return. You can’t ban lobbying, but you can make it less profitable by turning on the lights. In 2017 the TCJA did away with the corporate AMT, which had raised only $13b over the previous decade. The 2022 IRA brought back the corporate AMT, but it was so poorly executed that it fell far short of its projected $222b in revenue. Here’s my idea: Lower the threshold to $500m, double the rate to 30%, and take a machete to the tax code. By limiting accelerated depreciation, restricting R&D and clean energy credits, capping deductions for net operating losses, and limiting foreign tax credits, we can design a corporate AMT that raises an estimated $300b in revenue over a decade, while affecting approximately 400 corporations, or fewer than 0.1% of all U.S. businesses.

Third Rail

Since 1957 the share of Americans who are 65 and older has nearly doubled from 9% to 17%. At $1.5 trillion dollars, Social Security is the largest expenditure in the federal budget. U.S. seniors are the wealthiest cohort in history and the recipients of the largest redistribution in history. The program, which currently serves 69m Americans, is due to run out of money in eight years. Three trends are driving insolvency: more people reaching retirement age (good), people living longer into retirement (also good), and a decline in workforce participation (not good). If/when Social Security becomes insolvent, America’s grandparents will likely put their retirement on their grandkids’ credit cards. The fix is straightforward, but politically fraught: Means-test benefits and raise the retirement age (exempting people in physically demanding professions). According to a CBO analysis, increasing the full retirement age by two months per birth year until it reaches age 70 for Americans born in 1978 or later would decrease total federal outlays by $122b through 2032. Phasing out benefits for those with more than $150,000 of non-Social Security income would save an estimated $600b to $700b over a decade. We now spend $5 on seniors for every $1 on children. Enough already. Seniors who need Social Security should get it, but it shouldn’t mean an upgrade from Carnival to Crystal Cruises for NaNa and PopPop. At current rates, within a decade, we’ll spend half our federal budget on programs for seniors. (See above: The wealthiest generation in history.)

Planting Seeds

Last year, I gave a TED Talk that asked whether we love our children. Spoiler alert: We don’t. Our policy choices rob from the young/poor and give to the old/wealthy. The Big Beautiful Bill is no exception, but it does contain one “concept of a plan” worth mentioning. “Trump Accounts” would give each child $1,000 in a tax-deferred savings account; parents would be able to add up to $5k annually. The problem isn’t the $3.6b annual price tag, but the authoritarian branding gimmick. The tell? Only children born during Trump’s second term receive the benefit; the rest of America’s children are shit out of luck.

But there are other interesting “baby bond” proposals. Senator Cory Booker’s American Opportunity Accounts Act would grant every American $1k at birth, plus an annual supplement of up to $2k, scaled by family income. The funds become available when the recipient turns 18 and can be used for education, homeownership, or retirement contributions. Financier Bill Ackman’s Birthright proposal would grant every American $6,750 at birth at an estimated annual cost of $26b. The money would be invested in index funds until the recipient turns 65 — at an 8% rate of return, the bond would be worth $1m at maturity. Giving young people seed capital can grease the skids toward upward mobility, erode stark racial and regional wealth disparities, and renew the American dream. If our leaders do their job(s) and think long term, we’ll adopt an Ackman-like plan and, in 30 years, see an end to Social Security. In another 30 years we’d likely register a decline in interest rates and our largest line item, interest on our debt. As an old Greek proverb says, “A society grows great when old men plant trees whose shade they know they will never sit under.”

Tax Holiday

To combat high youth unemployment and stem the tide of young people leaving the country, Portugal announced a tax holiday for workers younger than 35. Under the plan, young people earning up to €28,000 a year receive a 100% tax exemption in their first year of work and reduced tax rates over the subsequent decade. U.S. youth unemployment is lower than in Portugal, and brain drain isn’t an issue, unless you’re a scientist or talented immigrant. Nevertheless, a tax holiday would benefit young Americans, as many of their challenges — education and housing affordability, stagnant wages, loneliness, declines in sex and dating, and a mental health crisis — reverse-engineer to income. My proposal: A federal tax holiday for workers under 35 earning less than $75k per year. (Note: These workers would still pay withholding taxes.) This would cost $110b annually, according to my back-of-the-envelope calculation. However, the extra cash — anywhere between $4,500 and $11,500 — would be a lifeline to struggling young people, and just as important, a rare sign that America actually loves its children.

Free Gift With Purchase

The first rule of holes is simple: Stop digging. For too long, Washington has been in a bipartisan shovel brigade. Somewhere on the horizon is a fiscal cliff. We don’t have to turn on a dime, as we didn’t get here overnight. But the moment we reverse course and signal that we’re grown-ups, the bond markets will notice, and interest rates will likely come down. Or we can continue to fuck around and find out. For every percentage-point increase in the debt-to-GDP ratio, the interest on Treasuries increases 2 basis points, according to a CBO analysis. That’s not much. But as Michigan’s Wolfers told me, we’re on track to raise the debt-to-GDP ratio by 25%, to 50%, in the coming years, resulting in a 1% increase on the interest we pay to borrow money. That translates to an additional $400b/year in interest costs. The more we spend servicing our debt, the more our creditors will worry about repayment. That means interest rates will continue to rise, and there won’t be any fiscal room left to keep seniors out of poverty, lift up young people, pay for healthcare, and provide for the common defense. Even without modeling for behavioral changes, my rough calculations illustrate a stark directional choice: Continue our march toward that fiscal cliff, or find real savings and invest in our future over the next decade.

Grow Up

Just as Big Tech weaponizes the “illusion of complexity” to convince us they just can’t figure out how to fact-check, stop Nazi content from going viral, or age-gate their platform (spoiler alert: They’re lying), lobbyists will fear-monger and claim these are complex issues with unintended consequences. The solutions are simple, but they’re also hard, requiring us to resume the adult conversation that ended when George W. Bush told Americans we could prosecute a war and cut taxes at the same time. And we believed him. I’ve come to realize I’m not my sons’ friend, but their father: Our difficult conversations instill a set of values which will serve them well in the future (I hope). We’ve been told we can have chocolate cake for dinner and not go to school if we don’t feel like it. At some point, let’s hope/trust an adult shows up.

Life is so rich,

P.S. Our full conversation with economist Justin Wolfers on Prof G Markets is required listening for grown-ups. Here on Apple or Spotify or YouTube.

50 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

I’m having trouble with the tax gap item. The one-year cost is $696B. The 10-year cost is $6.96T. Why on earth should we settle for recovering less than a tenth of that ($637B)? Accepting as normal problems (scofflaws, tax code complexity) of such magnitude is profoundly unsettling to me.

nice

Nice

Smart thinking grown-ups wouldn’t create 80K more IRS jobs, they would just simplify the tax code.

One of your better newsletters in some time Prof., good read.

Nice

The problem with means testing social security is the same problem with other means tested programs: administrative burden. Since “means” changes, recipients would need to be re-qualified regularly. I am confident. that huge numbers of very elderly recipients totally dependent on social security would have their benefits cut off because they could not navigate the paperwork maze needed to prove they qualify, as happens today with medicaid, SNAP, SS disability to name 3. Means testing will further the aims of those who want to end social security not those who want to preserve it.

Seems to me we already means test Social Security by taxing benefits above a threshold.

Recently heard someone say that as long as Baby Boomers are alive we will run huge deficits.

Great article with some interesting ideas. I think the biggest take away I had from the whole thing is that lobbyists are why we can’t have nice things. They skew the board so heavily in favor of people who can afford them that they dwarf returns of a normal investment. It is a blatant turbo charge of the asset class that must be curtailed. The easiest starting point to me would come in transparency and finance reform for elected officials. All lobbyist meetings with reps should be recorded and reviewable. Limit all spending on campaigns at a certain amount per person, and completely exempt entities from being able to donate. Money in politics is and has always been why governments don’t work for the people.

Nice

60% AMT? Really? If you live in NYC, then your overall tax rate is 75%?

This shows a stunning lack of creativity. Why can we not have budget cuts?

– Pay the doctors a little bit less (Medicaid / Medicare).

– Pay the teachers union a little bit less ($40k/yr per student to get like 5% of kids reading at grade level? You could get those results for free!).

– Spend a little less on the public housing (in NYC, they want $80b to fix the apartments? That’s $500k per apartment! Just build somewhere upstate instead for like 1/5 the cost.).

– Brad Lander wants to put public housing on public golf courses? No – do the opposite – move the public housing upstate and put elite golf courses on current public housing. How much would Manhattanites pay for membership at a club in Chelsea, or the Lower East Side, or even in East Harlem? Moving the projects will reduce the crime.

Just stop with the insane tax rates. Please. It’s enough already.

Much to love and some to wince over in this piece, but this approach is a king hell better road map then the OBBB and its plan to win the future with wood, coal, wishful thinking and gobsmacking debt. It’s a gutty opening salvo to Democrats whose counter offer is at present, nothing. I get hung up here, the essential debate framework is unchanged, perhaps, unproductive. For example, on federal revenues we’ve been having the same fight over the same two variables since 1960, the personal rate and the corp rate and their relationship to growth wrapped in a muddled “values” argument; we need new multi-trillion dollar revenue sources and neither of those offers much of an answer. We’ve been having the same fight about equalizing opportunity, government assistance or free markets; neither has produced a solution to birth-site poverty (and shout out to Bill’s idea BTW). Other examples certainly exist. I’m exhausted by the same fights. We need to reframe these issues to find a new emotional source of ignition about our centering possibility because Extremely and Deeply Troubling Scary Math, unfortunately I’m afraid, won’t get us there. Bravo nevertheless for showing your work.

I live in a mobile home in Silicon Valley. If you think that ” there are diminishing returns to happiness above a $200k annual in income” in all counties in America, have I got news for you. I can’t afford a traditional home here (my family has been here since 1850). My savings were wiped out in 2007-2012, so I am paying for college and trying to save for retirement while keeping my expenses low (We only drive used cars, no vacations). From what I have seen in my area? I would say “diminishing returns over a million/year”.

“exempting people in physically demanding professions” I wish I could update my original comment! Age discrimination is alive and well in tech. Yes I have seen individuals who want to coast and not upskill, but there are plenty of empty nesters who do stay sharp but are not a “cultural fit” (they question managers). This was an issue even before the rise of AI, and I suspect Gen X will only be shoved out faster. Why do you think work visas are for only 6 years?

Good article – the deficit is the biggest crisis this country faces. A few thoughts:

“it’s a(nother) conscious decision to transfer wealth from poor to rich as the effective tax on the wealthy plummets.” – actual IRS data shows that effective tax rate for the top 1% has dropped about 1.5% in the last 20 years. Hardly a plummet. The top 50 percent has remained effectively flat over this time period.

“However, the explosion in the tax code from 400 to 74,000 pages over the last century created an obstacle course that must be run at night.” – Wouldn’t the solution be reducing the complexity of the tax code vs. hiring more IRS agents? Wealthy people will always be at an advantage over everyone else in navigating the complexity,

Social Security – “U.S. seniors are the wealthiest cohort in history and the recipients of the largest redistribution in history”. – With all due respect, this money has been paid in by these recipients. Collecting on it is not a redistribution. If anything, your solution of phasing out benefits based on income is a huge redistribution. Raising the retirement age, an Ackman like seed plan, and encouraging immigration (expanding the workforce) are much better solutions.

Bravo!

Thank you for this. Very frustrated that the Dems complain, but don’t propose anything. This is a great start….can’t wait to read your articles on defense and health care. And agree with others….why don’t you run for office?

Solutions are easy; solving is hard. The people who read this are the ones who don’t need to read it. It’s so enraging to watch the society chase culture vulture laser pointers and ignore the economic fundamentals. I miss real conservatism – fiscally strict while seeking liberty and justice for all – but I think the social media disease has killed that for good.

I have just turned off my newscasts and pod feeds and am waiting for the end or some kind of implosion.

I could see T going the way of Dubya – they loved him, wanted to have a beer with him, until their kid and friends in the Guard got sent to Iraqistan and everyone in the neighborhood lost their house, now they never even speak about him – but I don’t think it matters. Someone will replace T. Those guys are just boil infections on an American body politic made sick with diabetes from the unchecked sugar of money and influence, and they’re going to keep coming back until the body works on its health (something we don’t have a recent track record of doing) or there is a event and the body dies. If you believe the body dying couldn’t be worse, you lack imagination.

I don’t know what will change that aside from some kind of national disaster we can’t drown out with Netflix.

I know our president doesn’t read but dang, I wish he would read your articles! Also, I know you don’t want to run for public office, but could you be in someone’s cabinet to propose some of your ideas? Keep it up, love reading your stuff!

I’ve heard Scott Galloway advocate raising the full retirement age to 72 based on rising life expectancy. While this sounds reasonable on the surface, it’s deeply unfair to many Americans.

Yes, life expectancy has increased — but not evenly. Life expectancy at age 65 has risen modestly (from ~16 years in 2000 to ~18 in 2020 for men), and gains are concentrated among the wealthy. A Brookings study found that between 1980 and 2010, men in the top 20% gained 6 more years of life expectancy at age 50, while men in the bottom 20% gained almost nothing.

Even more important is healthy life expectancy — the years lived in good health (HALE). For many in physically demanding or lower-wage jobs, serious health issues begin in their 50s or early 60s. HALE in the U.S. is around 66–68 years, well below Scott’s proposed retirement age.

Finally, many retire far earlier than planned — not by choice, but due to health or job loss. Most claim Social Security at 62. The Urban Institute and GAO show over half of older workers retire earlier than expected, with limited reemployment options after age 55.

Raising the retirement age would effectively cut benefits for those who can’t afford to delay — especially lower-income Americans. It reflects the experience of affluent knowledge workers, not the reality of the working class.

Better options? Raise the payroll tax cap or reduce benefits for the wealthiest retirees — not penalize the vulnerable.

Good points.

Thank you Scott for publicizing very innovative and rational ideas. You should be Speaker of the US House of Representatives. What do you think of US Senator Elissa Slotkin’s recent presentation of ideas? What do you think of raising the Social Security tax income level cut off to $250,000?

From your mouth to Gods ears

On the SS front, running out of money is different than running short of money (when the SS trust fund hits zero, people and companies will still be paying monthly fica taxes). Means testing is a good idea, as is the lifting of the income cap, currently at about 176K.

As for pushing the retirement age to 70, the only people who are for that are people who can retire anytime they want. The answer is to fund SS properly and keep the ultra rich off it.

I pay into SS for 50 years- it’s not an entitlement. And now you want to steal my money because I’m successful? Robinhood economics is theft.

This is not the American way. It is precisely what is wrong with big government and why our country has so much distrust in government and institutions that were previously sacrosanct. Such extreme leftist behavior contributed to Trump’s successful election victory.

Capital goes to where it’s treated best. Such theft will chase capital away resulting in lower aggregate standards of living for all.

You seem to be able to survive on what you have. You also have a wide following. Why not strike out in politics? Lots of us out here would not have problems supporting you.

Scott, you mean well and are very smart and talented. Regardless, the road is paved with good intentions. Raising taxes to enable an ever increasing government is not the solution. Why? The answer has always been to reduce the size of government and spending. Why? Because the private sector is much more efficient than the public sector. Why? Because the government is the largest and worst monopoly. Corruption, inefficiency and waste are hallmarks of Government- the largest & worst monopoly with no competition and no market mechanism to measure success or failure. And it grows using threats of coercion and violence to enforce its will. The best government will always be the smallest one as envisioned by our founding fathers. Decentralized power over centralized while as limited as possible enabling LIBERTY.

Capitalism is best at allocating resources. Government is amongst the worst. Less waste simply means more aggregate wealth. As long as capitalism rewards capital our aggregate standards of living will remain the envy of the world. Capitalism has lifted more people out of poverty than any other socioeconomic system. Is it perfect? No. It’s just better than everything else. I trust the market more than any government every day and twice on Friday. Have a great weekend.

Fellow readers ….. Always remind yourself that Scott is a Marketing guy. You know “Mad Men”. If the goal is to kill small business, stifle entrepreneurship and drive the economy into the ground vote for Scott.

True. Robinhood theft will always be attractive to those who are envious of those with more while paying little to no income tax.

It would be great if your message would get to the folks passing (or not passing) law in Washington. I am guessing your readers are not the problem.

Mind over matter – the ones who matter don’t mind and the ones who mind don’t matter.

Scott –

Social Security is not a “benefit.” It is a fully funded return of capital from workers who have contributed to it for their entire working life. It is not the government’s money; it is the recipient’s return of contributed capital. Nobody will ever get an ROI on their investment nor will anybody get back all of their money.

Since inception during the Great Depression, the rates have increased from 1% of the first $3000 of earnings to 12.4% of the first $176,100 of earnings.

In 1966, Medicare/Medicaid tax of 2.9% on ALL earnings was imposed and tacked onto the same attachment scheme.

Today the total burden on workers and employers is 15.3% of wages up to $176,100 and 2.9% on all earnings beyond that amount.

In 1983 SS funds were taxed as income and again in 1993, and 2023.

While there is some mythology attached to the issue of commingling of SS and general funds there is no question that the bogus special US Treasury certificates — the infamous IOUs — are completely specious as they depend on the same source of payment, the US taxpayer.

Today, there are 67.1 million (51.4 million retirees, 8.7 million disabled, 5.7 million survivors) people receiving SS benefits.

The solution is to privatize SS.

In the course of privatizing SS, a tax of 1-2% on the working population that opts out coupled with a delay of the eligibility age would work wonders on extending the drop dead date of the solvency of SS.

Cheers.

That’s appealing on one level, but who would run it? The banks? They are already opaque af and as Bill Maher said, with a gun you can rob a bank but with a bank you can rob everybody. They’re already such a tumor wrapped around the heart of US capitalism the 2008-9 emergency was how to give them what they wanted, not make them better. I am not sure how giving them more power would make anything more effective except stratification of wealth (which doesn’t need any help).

Yes, corporate lobbyists have won the day.

In addition to some of the suggestions of an updated corporate AMT, I think that some limitation of full current deductibility of R&D expense is a reasonable and appropriate item. The current five year capitalization and amortization of R&D expense is excessive, as is the current proposal to return the R&D expenditures back to current expenses. But the biggest corporate issue is the limited IRS audit staffing for large company audits. Clearly the 21% rate is too low, but the proposed Biden rate of 28% was dead in the water. But nothing will happen since King Donnie the Mendacious is in control of the MAGA members of Congress.

Changing the retirement age for people not yet in the workforce is one thing, but changing the rules of retirement for Millennials—the oldest of whom are already 60% of the way there—would be politically and socially disastrous. It would shatter what fragile confidence Millennials have left in the American system. Social Security is a promise to Americans from our government and reducing the benefits breaks that promise. Raising revenue to fulfill that promise (for example, by increasing the contribution rates and limits) is better than reneging on that promise to American’s who have fulfilled our end of the deal by paying our payroll taxes for our entire working lives.

One of your best Scott. You allude to it with capital gains, but if we are going to have an INCOME tax, we should tax all income the same. Why should a couple with combined income from wages pay over 7 times the federal tax of another couple with no wages and $150,000 of dividend income.

Because those funds have already been taxed at least once?

A citizen earns income and it is taxed as ordinary income.

A citizen invests that after tax money and makes a capital gain and it is taxed as a capital gain.

A citizen works hard, makes good investments, and accumulates an estate and is taxed yet again when he dies.

How many times does income get to be taxed?

This is why ideas like the fair tax and the flat tax make sense.

Cheers.

JLM

Bingo! The answer isn’t to keep finding new ways to expand the tax revenue. The answer has always been to reduce the size of government and their spending. Why? Because the private sector is much more efficient than the public sector. Why? Because the government is the largest and worst monopoly. Corruption, inefficiency and waste are hallmarks of Government- the largest & worst monopoly with no competition and no market mechanism to measure success or failure. And it grows using threats of coercion and violence to enforce its will. The best government will always be the smallest one as envisioned by our founding fathers. Decentralized power over centralized while as limited as possible.

“Democrats have criticized the bill but haven’t offered alternatives as they live up to their signature “right, but ineffective” brand.” I’d say Scott is showing himself to be right, but naive. The reason the Democrats aren’t proposing an alternative isn’t because they are “ineffective”. It is because to do so would simply give the Republicans a new target and help them rally themselves. It would change a conversation that is going very well for Dems right now. And to what end? Their is no way a Democratic proposal would be enacted. Scott, I’ll vote for you if you ever run for something, but definitely get yourself a professional political consultant.

Scott –

You provide a fair agenda for discussion, but your foundation argument as it relates to the impact of tax cuts on Federal revenues is simply not true. It undermines the validity of your arguments.

Since WWII, the US has had 6 tax cuts from both parties:

1. The 1945 Revenue Act that stripped out the WWII excess profits taxes no longer necessary post-war.

2. The Revenue Act of 1948

3. Kennedy tax cuts of 1964

4. Reagan tax cuts of 1981

5. Bush tax cuts of 2001-2003

6. Trump 1.0 tax cuts

In every instance, Federal revenues post the implementation of the tax cuts had a positive impact on total Federal revenues. It takes a year or two to really feel the impact.

The honest numbers guys in the tax racket know this to be true. You should reflect this fact in your musings. It simply undermines your arguments on everything when you don’t deal with the truth of this matter.

Cheers. Hope you have a happy July 4th.

JLM

Jeff. Wrong. The U.S. economy always grows and it doesn’t matter if taxes get cut or not. This is the greatest country in the world. Has nothing to do with tax cuts. Ask Buffett.

If true, then what is the brief not to cut taxes, amigo?

JLM

Bigger deficits.

Spot on, Mike. Measured as a share of GDP, the Federal budget has been about the same percentage for about 50 years. Tax revenue as a share of GDP has declined due to tax cuts #4, #5, and #6. Thereby exploding the deficit.

Scott’s research is stimulating if not easy to translate into action as many of us try. I ask when will Scott run for office or focus on how to create a movement to take these ideas to the streets? Being right but no effective is not enough! Thanks and how can we help.

You forgot about removing the cap on Social Security contributions . . .

Valiant attempt, but I find the piece populist and misdirected for the following reasons:

Progressive Tax Fatigue

Continuously raising taxes on the wealthy (e.g., AMT at 60%, estate taxes) risks capital flight, reduced investment, and declining entrepreneurial activity — hurting the very economic growth needed to reduce deficits.

Baby Bonds ≠ Behavioral Change

Giving every child $6,750 at birth may sound promising, but without addressing structural issues like education quality, housing access, and job opportunities, it won’t meaningfully shift wealth outcomes or mobility.

Tax Holiday = Regressive Relief

A tax holiday for under-35 workers earning <$75K may offer short-term relief, but it bypasses those most in need — the unemployed or underemployed — and does little to address root causes like wage stagnation or student debt.

Means-Testing Social Security Undermines Trust

Transforming Social Security into a means-tested benefit erodes its universal appeal, risks political backlash, and may weaken long-term support for one of America’s most stable social safety nets.

Audit Expansion Could Backfire

While targeting high earners sounds fair, aggressive IRS enforcement risks political weaponization, public distrust, and unintended overreach — especially if AI tools misclassify honest taxpayers.

“A tax holiday for under-35 workers earning <$75K may offer short-term relief, but it bypasses those most in need — the unemployed or underemployed"

What happens to the 34 year old earning $74k when she gets a raise to $76k? No longer eligible for the holiday, is she now paying the Federal 20% on the whole $76k? If so, that's a massive pay cut. If not, what about after her birthday? Happy birthday girlfriend, now look for a new place to live because you can't afford the rent now we've cut your income by 20%.

All this stuff is super easy to Scott, who makes snide comments about fear-mongers and claims of complex issues but, unless you're a basic populist, it is in fact extremely complicated.

“A tax holiday for under-35 workers earning <$75K may offer short-term relief, but it bypasses those most in need — the unemployed or underemployed"

What happens to the 34 year old earning $74k when she gets a raise to $76k? No longer eligible for the holiday, is she now paying the Federal 20% on the whole $76k? If so, that's a massive pay cut. If not, what about after her birthday? Happy birthday girlfriend, now look for a new place to live because you can't afford the rent now we've cut your income by 20%.

All this stuff is super easy to Scott, who makes snide comments about fear-mongers and claims of complex issues but, unless you're a basic populist, it is in fact extremely complicated.