Scarcity Cred

Scarcity Cred

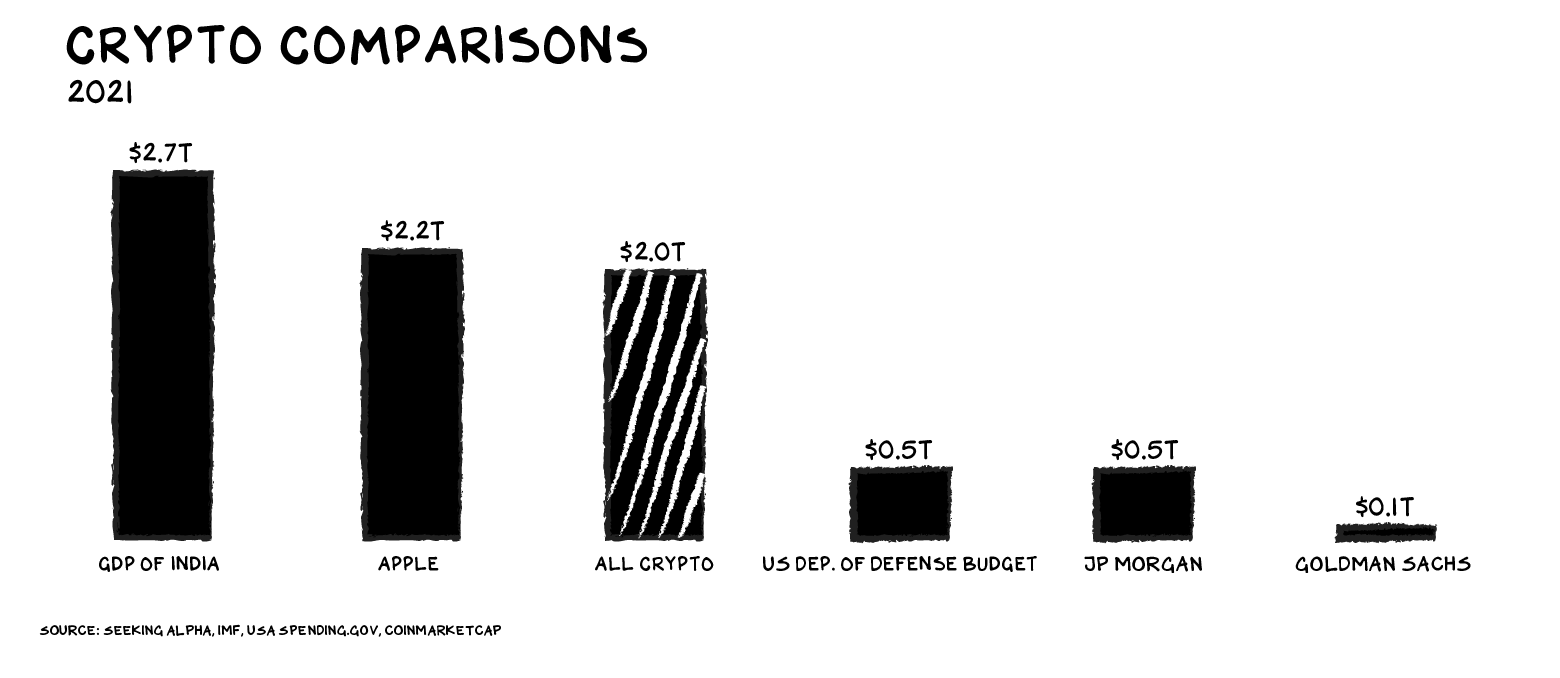

Any firm that approaches $1T in value has tapped into a basic human instinct. Consuming, signalling, loving, and praying have been the fuel of Amazon, Apple, Facebook, and Google’s ascents, respectively. That the crypto asset class universe has reached $2T reveals, I believe, that it taps into two attributes we instinctively pursue: trust and scarcity.

Trust

Our superpower as a species is cooperation, which requires trust. It’s the reason banks, traffic lights, and anesthesiologists exist. Even before crypto, creative minds have been drawn to finance, as trust creates opportunities for leverage and securitization. In 1997, seeking more control over his songwriting catalog, David Bowie raised $55 million with Bowie Bonds. The bonds paid 7.9 percent interest over a 10 year-long term — a scant premium to a U.S. 10 Year Treasury Note at 6.4 percent. What made Bowie Bonds unique was the collateral, or source of trust: future royalties on Bowie’s music, which the bondholder felt people would continue to value. Moody’s rated the bonds A3 and Bowie used the proceeds to buy out his former manager, shoring up the bonds and securing long-term control of his music.

Though innovative in its collateralization, the Bowie Bond was on its face a vanilla financial instrument, no different in form than a bond issued by GM or P&G. In order to connect his art and potential investors, Bowie had to rely on the (expensive) apparatus of traditional gatekeepers in finance and entertainment to imbue his bonds with the essential attributes of trust and scarcity. The royalty stream (trust) was mediated by lawyers and accountants in big publishing houses, and the legitimacy of each individual bond (scarcity) was dependent on the financial powers of Wall Street.

What if Sir David Bowie (note: he declined knighthood in 2003, but it’s my blog) fell to earth in 2021? What might Bowie have done … with crypto?

Scarcity

People like scarcity — a lot. Owning something scarce makes one feel unique, and signals success and worthiness as a potential mate. Scarcity is also an instinctual trigger for obsession — when we sense a scarcity of something, be it food or a mate, we are programmed to become obsessed with finding it. Art auctions, the (pre-pandemic) lines outside Supreme, and the margins on a Panerai Tourbillon prove this point.

A Van Gogh and a Rothko are both unique, and therefore scarce, because they are made of atoms, and it is impossible to arrange a second set of atoms in an identical configuration. Print artists, whose lithographs are made to be reproduced without alteration, use a small “17/100” written in the corner, to distinguish each print and bestow scarcity upon it.

To hold value, scarcity must be credible. The dirty (not-so) secret of the art world is that art buyers, and even professional art appraisers, struggle to discern originals from forgeries. A well-made forgery provides the same practical value as an original — you can hang it on your wall and bask in its profundity. Yet the art world invests millions of dollars in identifying the “real” version of valuable works; once unmasked, forgeries are nearly worthless.

Digital art suffers from perfect reproducibility, and hence, a lack of scarcity. There is no “real” version — even in the artist’s studio, copies proliferate in backups, on shared drives, and in cache files. For decades, we have experimented with watermarks and anti-piracy tech to try and enforce a physical, world-of-atoms scarcity on digital goods. By contrast, non-fungible tokens, (NFTs) reflect a digital-native approach to credible scarcity.

Attaching an NFT to a digital artwork gives the NFT owner discretion to designate any digital copy of that artwork as the sole authentic copy at any point in time. This approach jettisons our world-of-atoms obsession with a specific physical object, and acknowledges that scarcity has always been a function of bits, not atoms. Value is in the eye of the beholder.

Let’s Dance

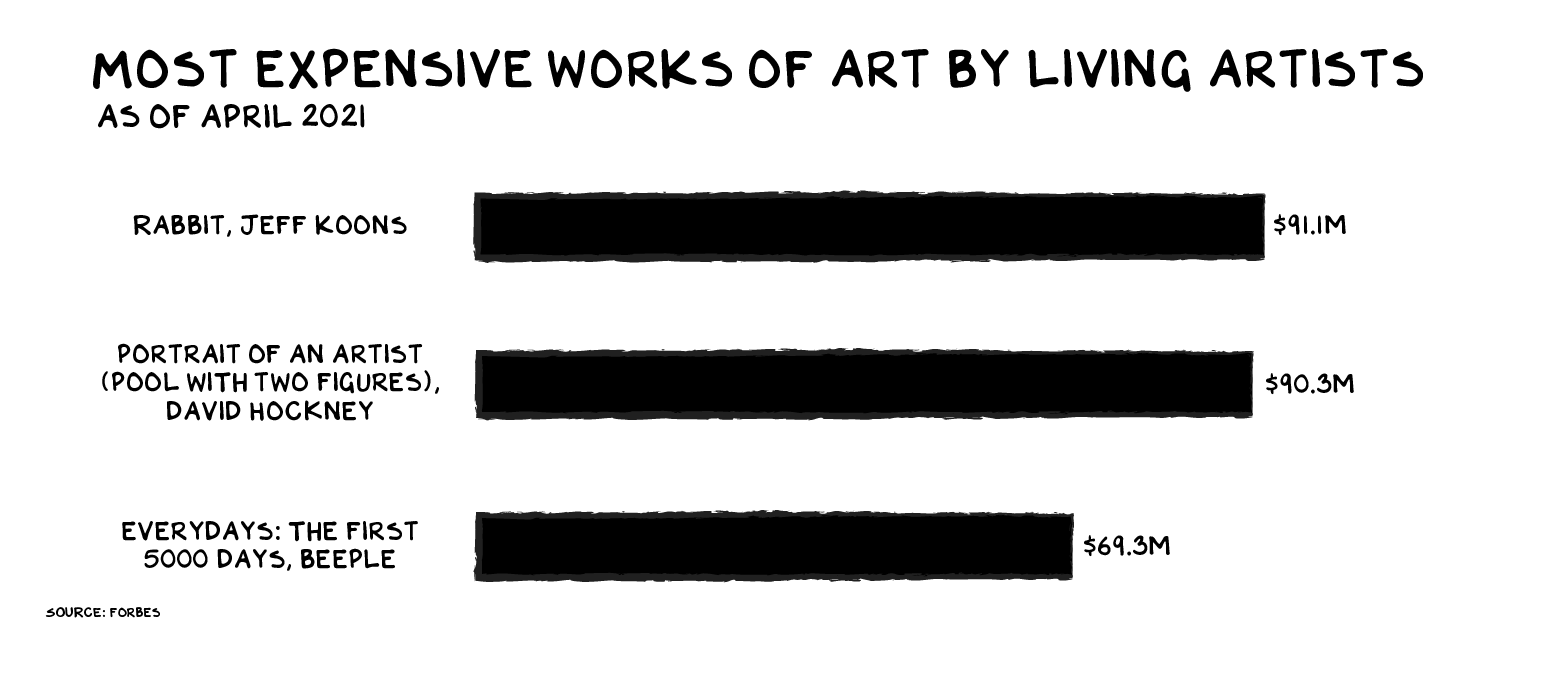

On March 11, digital artist Beeple collected $69.3 million (minus the hefty fee of his gatekeeper, Christie’s) from the auction of an NFT associated with a collage of his 13 year-long project of daily digital artworks. The media has made much of the fact that the buyer of Beeple’s NFT, crypto investor Vignesh Sundaresan, did not obtain any tangible “thing” for his money. The art itself is available for anyone to view — for free — on Beeple’s web site. But collecting art has rarely been about the thing. It’s about credible scarcity.

NFTs create and capture the value of scarcity cred in a massively dispersed fashion that bypasses gatekeepers and taps into capital anywhere. At the high end, digital art sold for millions doesn’t really need an NFT, just as Bowie didn’t need crypto to securitize his royalties in 1997. Christie’s could have just as easily sold an embossed paper certificate, and entered the buyer’s name in a leather bound book securely held at Christie’s headquarters. But that sort of infrastructure isn’t available to the vast majority of digital artists, whereas anyone can create an NFT. Nyan Cat, a pop culture meme, isn’t likely to appear at Christie’s any time soon, but as an NFT it sold for nearly $600,000.

All the Young Dudes

Scarcity cred explains more than NFTs. The entire $2T crypto asset class rests on scarcity cred. Bitcoin’s attractiveness as a store of value is a function of its scarcity cred, as it has a built-in limit of 21 million coins. Compare that to the USD: Almost 30 percent of the U.S. money supply has been created since 2020.

There’s a variety of crypto technologies/products/platforms evolving new means of creating and capturing value in a network: Ethereum, Ledger, Uniswap, Hedera, Cardano — a soup of innovation that is, similar to other tech innovations, not doing anything new … just doing it better.

It remains to be seen if this approach will take hold. Crypto’s energy use is a source of real concern, but the hardware and software are evolving quickly to become far more energy efficient. Even Beeple thinks the current mania is a bubble, as he told my podcasting partner Kara Swisher. But the history of the art market is a history of bubbles, as are the histories of finance and the internet. All are still with us.

Crypto is firing on the walls of the world’s financial citadels. Naturally, the generation of leaders behind those walls is not inclined to acknowledge the Wildlings outside. But scoffing at novel technology, be it a mangonel, black powder, or blockchain, rarely ends well for the legacy asset holders. Bigger castles are already being erected on the hill just above the naysayers … in this case, in mere years vs. generations. It’s likely that on the day of its imminent public listing, Coinbase will be more valuable than Goldman Sachs. A reasonable question in the JPMorgan and Goldman board meetings:

How the fuck did we/you let Coinbase happen?

But that’s another post. Unencumbered by regulation, reticence to destroy legacy assets, or boomer brains that just don’t “get it,” crypto is a $2 trillion disruptive force. I can validate that anybody over 50 has trouble understanding this stuff, and am fairly certain that the number of candles on the CEO’s office party birthday cake is inversely correlated to their understanding of crypto.

Of course, in a system that is still heavily skewed in favor of older, white men, “getting it” for that cohort can be worth billions. Crypto investors Michael Novogratz and Michael Saylor, both over 50, have a combined net worth approaching $10 billion. But they are the exceptions.

Bowie himself was 50 when he issued Bowie Bonds. A prolific art collector, Bowie was also famous for championing young creators, and being enamored of technology: In 1998, he launched his own internet service provider, BowieNet, an interactive music community a decade ahead of its time, and the next year, he launched an online bank (BowieBanc). “If I was 19 again, I’d bypass music and go right to the internet,” he said at the time. In a prescient 1999 interview, he is a time traveler explaining the future to our skeptical past.

RIP Bowie, you would have loved crypto.

Life is so rich,

P.S. I’ve got a side hustle (#fakemillennial). In 2019, I founded Section4 with the intention of lowering the barriers to receiving an elite business education: letters of recommendation, the GMAT, the time away from work, and the cost. We’re addressing these barriers with Section4 Sprints – 2-3 week intensive courses taught by the best professors from top MBA programs. Next up from Section4 is NYU Stern Professor Adam Alter’s Product Strategy Sprint (I also make an appearance as a guest lecturer). Sign up now.

P.P.S. Esther Perel, one of the leading voices on modern relationships and the New York Times bestselling author of “The State of Affairs” and “Mating in Captivity,” joins us on the Prof G Pod this week. We discuss why eros is the antidote to deadness, the pain points cofounders have experienced throughout the pandemic, and parenting tips to ensure your children grow up to be great partners.

26 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

My concern remains that this transfer of wealth and potential earnings from a perceived whimsical and surely artificial sense of scarcity doesn’t contribute much to an individual’s productivity and that of a society and nation as a whole. If only crypto has so much potential to transform fortunes of a cohort or a nation, it would have done so. Alas, for what I seen from my vantage point, its just become another adrenaline-induced gambling-mania that most are findings just too hard to resist. Bovid-bond are fine since there was a certainty of performance and outcome, but NFT and crypto are too prosaic to be considered an asset class.

Scott, you frequently lament the transfer of wealth from the young to the old through traditional channels and government policies. I’m not as worried. I see crypto and other disruptive tech as the natural and legal antidote. The other antidote against older, white men continuing to accumulate wealth is senility (Buffett’s still not getting tech 20+ years since the internet bubble is a good example). If that does’t work, death will take care of the rest.

“I’m born in 1957 and it was too late for me.”

Me too and although it was a struggle, with a bit of a math and IT background I managed to cope, possibly better than some from later birth years.

The exploitation of age stereotypes is just another -ism that deserves to be abandoned. The young aren’t universally digital natives, the old aren’t universally excluded from novelty. Each brings a useful perspective. Next we’ll be hearing the young know nothing and the old omniscient.

I’m born in 1957 and it was too late for me.

Coaxed by my son, I made a few very brief ventures into the pond with a toe in the water, and honestly, the returns were so striking that it all scared me — mostly because I knew I had no idea what I was doing.

But my LED moment came when I began to appreciate the enormous amount of creativity, endeavor and construction that is going on relative to block chain, and, very much of it is based on an economy of tokens and coins. If these “currencies” can be exchanged for such a massive enterprise building, they have intrinsic value, period. One cannot say how much value with precision, but one cannot deny these basic transactions exchanging (highly skilled) labor for decentralized, trustable, limited volume (for the most part) digital currencies . So I converted from a lucky, tentative person, to one holding a diversified portfolios of coins at about 10% of liquid net worth.

Not for everyone, but a stimulating exercise is to run through (or walk or crawl through) Gary Gensler’s MIT course, 15.S12, Fall 2018, on Blockchain & Money. It can be found on YouTube. Gensler is anticipated to lead the SEC after Senate confirmation in mid-April.

I know that in theory bitcoin is limited to a certain number of coins. (is that the right term?). Does the theory still hold when it can be forked? I got some bitcoin cash years ago in a fork. That added to my overall ownership, doesn’t it?

Secondly, couldn’t the community vote to increase that number? Ie. When we are down to the last 100K couldn’t more be created?

When we speak of “understanding Crypto”, there appears to be a need to segment understanding the technology against understanding the impact on human psychology. While trust is inherently part of the technology in the blockchain, scarcity is a choice and is manufactured in both Bitcoin and NFTs to tap into the psychological drivers of value.

This manufactured scarcity is particularly interesting when the product exists solely on the blockchain. Given the lack of any intrinsic value, we are left with “scarcity cred”, or a form of signaling importance through ownership. While this is not new, it has never been distilled into its rawest essence.

While Bitcoin and an individual NFT is scarce, in aggregate cryptocurrencies and NFTs are infinite. The value of any individual cryptocurrency or NFT will depend on trends and a not insignificant amount of luck. The fine art market is an often used comparison, however as a whole, it has underperformed against most asset classes (source CITI analysis, 1985 – 2018). Unless you know the Vang Goghs and Rothkos ahead of time, there are safer places to store your money.

On a personal note, I am disappointed to see a trend towards embedded ownership. I had great hope in seeing news articles of millennials moving to a sharing economy, with a premium of investing in experiences and relationships rather than in things that convey status. Perhaps the pandemic was a big enough force to disrupt this movement, sending us searching for meaning in things, even if these things were ethereal. Let’s see – I’ll hope for the better.

Beyond crypto, the digital ledgers created with blockchain have enormous possibilities with notary and simple record keeping. Identity will be a big mover….I love Identity.com and Civic. There is also a new player in town, SOLANA. It’s a giant leap for blockchain that solved a major problem with transaction thorough put.

I am a big fan much over 50. I get crypto but the history of currency is i think about who will go to war and kill to defend its value. Unlikely to see artists and whatever generation this is now go to war to defend crypto value. The institutions that do have that power will no doubt ultimately restrict its enemies like crypto and enforce it. Meanwhile enjoy the ride

Actually YOU don’t seem to understand NFTs. You literally buy “bragging rights” to a receipt that a specific fungible work of art was minted to a blockchain.

There is no value either in the product it represents, or the actual “receipt” aka NFT.

The entire market is just a bubble based on IOUs between people.

There is zero scarcity in cryptoart, as even if an “artist” sells a work on a blockchain or a marketplace, he can always just re issue it on another blockchain, or sell it through other means elsewhere – the artwork is just a JPG or GIF file ffsake, not even the original source files of the artwork! This is like selling for $69M a picture made with your phone of the Monalisa, not the actual Monalisa. Sure, it’s a “unique” picture of the Monalisa, but one must be very idiotic to pay $69M for that.

Apparently, some people are really that stupid…

p.s. also nobody actually paid $69M for Beeple’s artwork, that is a speculative price, the final amount was settled in ETH and the price of ETH was X at sale then, but can be X-$68M in a year as there is no guarantee of future value. While buying an actual Monet or whatever for $69M in cash is something no crypto bro would attempt when their real net worth is based 100% on speculative “coins” and no real assets.

p.p.s Beeple can re-sell the same “artwork” for $100M in Tezos on the PoS Tezos blockchain and that guy who bought on ETH blockchain can do nothing about it.

Was actually replying to Ngyrnot with my comment.

But can apply to the OP also, as this was a very poorly written article, missing the point on both crypto, NFTs, etc.

as they can – arguably – tap into a basic human instinct: greed – nothing to do with trust or scarcity.

Who is to say that Bitcoin has a definitive scarcity value since the owner ship of billions of Bitcoins not in play is unknown or when they may be released on to the market. Other more efficient and less energy consuming cryptos may also emerge while governments may insist on regulation or annulment of what is a unregulated and secretive hoard for black market money and gamblers.

does “cred” mean “credibility” ?

“It remains to be seen if this approach will take hold. Crypto’s energy use is a source of real concern, but the hardware and software are evolving quickly to become far more energy efficient.”

One could argue that this is not the point. The real progressive question to ask ourselves is – is it really necessary to spend that much energy to ensure a high level of security and speed? Absolutely not.

The reality is that Blockchain is a very badly designed technology and cryptocurrencies that are based on Blockchain (and more specifically Proof-of-work) are a waste of time and energy.

You mentioned Hedera. Well, Hedera Hashgraph is the perfect example of a well-designed technology in which we should all invest. It is a far better alternative in terms of security (Byzantine fault tolerant) and scalability (+10,000 transactions/second) and years ahead in terms of energy consumption.

So saying that Hardware is evolving so that we can mine more and more is completely missing the point.

We have the technology at our disposal to do BETTER.

Bravo – spread the word about Hedera! We’re talking Model-T/Tesla vs. Horse & Buggy

Scott, Quick question. While it is true that “ NFTs create and capture the value of scarcity cred”, what does fractionalising ownership (that NFTs allow at scale) do to that scarcity?

Bharath, for an example of “fractionalising ownership” with NFTs at scale, consider the massive number of people who have software license keys that allow them to claim “ownership” of a right to use one or more software products. Those keys generally allow an unlimited number of people to buy equivalent usage rights. (i.e. A Microsoft Word key allows you to use Word as much as anyone else holding a similar key.) NFTs are basically just software licenses for digital products (like .jpegs) or certificates that allow one to prove a claim (e.g. An NFT/key could designate someone as the “First owner” of the .jpeg.) In some applications, presentation of the NFT/key will be needed to actually “use” the product or make the claim, in other cases, possession of the NFT/key only allows you to make statements about your specific rights to use a thing. (i.e. We might all be able to “use” or “view” a particular .jpeg, but only someone with the NFT could claim that they use it as the “owner” or as the “first user.” Analogously, imagine that everyone could use Microsoft Word but only some people could claim that they they had a license to use Word. Many people would wonder why anyone paid for a license to use what could be used without one. That puzzlement is what many experience when hearing about NFTs applied to bitmaps or .jpegs.

Your point about NFTs and art is bizarre. If I own an original Van Gogh, it’s scarcity comes from the fact that I have it and no one else can. An NFT is just a URL in a blockchain, everyone else can have identical copies of the art and not pay $63 million dollars. You can buy an NFT for $1billion but it produces no scarcity for you. It’s literally no different from an app that costs $1million and does nothing. It’s for dick waving.

An NFT is a digital representation of something. The NFT itself has no intrinsic value, but the thing that it represents does. Think of it as a receipt for something you purchased, a proof of ownership. What NFTs allow you to do is to transfer that ownership seamlessly. When you buy an NFT, you are buying the rights to that which the NFT represents.

Ngymot, your claim that NFT’s have no value ignores at least two cases where they do have value:

1. When “ownership” of the NFT allows one to make claims that might have value. (e.g. “bragging rights”)

2. When “ownership” of the NFT is required for the use of some asset. For instance, in the case of software licensing.

One can copy and possess a copy of Microsoft Word without a software license key (off-blockchain NFT) but mere possession of Word won’t allow you to use it unless you can prove that you have the NFT/key. In this case, it is arguable that the “value” is in the key, as a proxy for the right to use Word, not in the Word software itself.

Back in the 80’s and 90’s we dealt with this issue as we were introducing software license management for products at Digital Equipment Corporation. We had interesting debates with customs officials who at first suggested that imported CDROMs containing software products should be valued at the full market cost of the software. However, we were able to establish that nothing of value had been transferred until the the key to use the software was also provided. Thus, the CDROM’s value was that of a piece of small piece of plastic (e.g. $0.00) while it was the NFT/key that had dutiable value. The argument is still a good one. NFT can or could have value if proof of one’s ownership of the NFT enables one to do something that cannot be done with out such proof.

The arguments regarding keyed access to utility are ok; the rest are not so good (including Scott’s).

First, value is subjective, and in markets, statistical. You don’t get there from 1 purchase. That says more about the surplus funds of the buyer than anything else. Driving around in a $300,000 convertible is a better social signal, in terms of having a market value to match what was paid for it. If suddenly, those cars were available identically for free, that signal would be lost. Extravagant purchases made by the wealthy are done for social effects out of reach by ordinary people of the 99%.

That has little to do with scarcity, and much more to do with ability. When we look at someone like Van Gogh, it’s the talent that was scarce, divided by the time alive. Digital talent does not exist; it is indistinguishable between creators who’ve created identical items. Time & money are also irrelevant here, as no additional work or cost is needed to make 100 or 100,000 more copies.

In order to capture this non-fungible kind of value, utility has to be made of access to it. That would mean a non-digital access; this is using the Oracle problem. There’s always a weak point between the digital & physical worlds that can be exploited. There’s also nothing stopping another digital host (blockchain) from re-entering the same data copy on a separately controlled system, if it’s available digitally.

Ask 95% of crypto buyers why they hold cryptocurrency. They might regurgitate talking points on ‘blockchain’ , ‘system of ledgers’, or ‘impossibility to forge via NFTs’ mentioned above but if they are being truly honest with you it’s to get rich – and get rich in USD. Keep digging and you’ll see that the vast vast majority has as much understanding of it as the boomers you deride. These currencies have almost no legitimate utility (again if we are being honest) and are way to volatile to be used as a legitimate currency in the near term.

At best Bitcoin and cryptos replace gold due to limited supply as a store of value. Aka just a commodity, a speculative one at that

Scott – will there be any sprints on finance?

Bowie, love it! Scott, I’ve heard you say on Pivot that you don’t understand crypto, but if you ask me, you understand it pretty well, because this is a better way to think about it than the cryptspeak booster stuff you get most places online. Keep it up.

I’m happy to see you discuss a subject of importance. Most of the world is belatedly catching up to this development which is over a decade old. Better late than never, I guess.

I respect and agree with most of your points. I differ, however, on the ageist notion. I’m 63 and have followed crypto-currencies from the outset, simply out of intellectual curiosity and not for any other reason. (I work in law, not tech.) I don’t believe age affects one’s awareness of new technology; it’s more whether you care to pay attention to emerging trends or not. Most people are content to remain oblivious to them until events shape their lives. I prefer to stop and scout those forces in advance of that.

Scott you are usually on point but this to me is more of a filler post than anything else.

Scott – I always look forward to your notes/podcasts, thank you. Inevitably there is good food for thought/debate. I agree with your point about scarcity as a reason for blockchain/crypto appeal. However, on the subject of trust, is it not the absence of trust in today’s society that is driving us to blockchains? You say: “Our superpower as a species is cooperation, which requires trust.” I think we want to, and can, cooperate but can this cooperation not be better done in the “trustless”/”permissionless” world that is a hallmark of platforms like Ethereum? I suppose you could argue that this “trustless” state paradoxically produces the trust we all crave. Like you, I am over 50 and trying to stay on top of this. By the day, I am reminded of the mid 1990s when Web 1.0 was launched. Investors then were not able to invest directly in the Web 1.0 platform (or the subsequent Web 2.0 mobile platform). If Ethereum (or one of the mooted “Ethereum killers” like Solana) represents Web 3.0, it’s a pretty exciting investment opportunity to contemplate, yes?….perhaps you can address this subject in an upcoming piece?