Trust vs. New

Trust vs. New

In the first session of my brand strategy course, I ask the kids what is the strongest brand in the world.

Most say Apple. A few kids sense I’m going off script and will say Jesus or Michael Jordan. I offer up the US dollar. Near 100% recognition, owns a color, unique associations, and extraordinary trust.

We personify brands and have pseudo‑relationships with them. If that sounds fucked up, trust your instincts. It’s the same sort of fucked up as loyalty to institutions, which I don’t understand. I tell my students to be loyal to people, not to inanimate brands or organizations. The former may or may not take care of you when you’re older, but I’m certain the latter won’t.

We’ve placed a great deal of value around the trust component of brands, as for a long time it wasn’t a given that you could trust the brand to treat you well. They had products that gave us cancer, appliances without warning labels, devices that broke down. Brands often refused to stand behind their product or give you your money back if you were unhappy with it. But in the nineties and aughts, brand strength was synonymous with trust, which was based on brand experience and associations. We grew to trust brands the more we used them, and the better they treated us. The kindness, courtesy, and effort brands put into their relationships with us evokes the preferential treatment of select societies.

In a culture that sees the consumer as our nobility, potential risks of choosing the wrong brand are minimal. Instead of trust, the new points of differentiation are competition and transparency. Now, what’s more important to consumers, rather than trust, is delight. Whether it’s my dad returning a sweater years later, no questions asked, Nordstrom bringing cufflinks to my hotel room before a wedding, or Amazon Now getting an order to my desk in 47 minutes, we have an arms race around delighting, vs. trusting.

Enter New

So, as consumers no longer need to worry as much about the downside, we’ve raised the bar and no longer need to defer to the known and trusted brand. Our expectation is that any brand will treat us relatively well. We’ve replaced trust with different, special, new. We used to ask, “What’s the best hotel in London?” Now, it’s “What’s the hot new hotel in London?” We have weapons of discovery that can find new and get us to a level 10 satisfaction (great and new), vs. the trusted 8 (great and same). Our instinct to diversify the gene pool and seek competition triggers excitement when we find the great new thing.

This has played out in business results. In nearly every consumer sector, small, independent brands are increasingly taking a bite out of larger‑scale players. Between 2013 and 2016 craft breweries went from 9.4% to 12.3% of beer production in the US. Craft alone is no longer cool enough, and in 2016 the smallest guys — microbreweries and brew pubs — drove 90% of craft brew growth. A similar story has played out in the booming beauty sector, where indie brands were up a staggering 43% in 2016. In activewear, Nike and Adidas face competition from ankle‑biters Allbirds and Outdoor Voices, who have established a foothold among millennials in urban markets like San Francisco and New York. And in CPG, long controlled by corporate giants, the only thing the fastest‑growing brands in e-commerce (read: growth channel) have in common is that most of us have never heard of them.

So what’s a brand to do in an era of new vs. trust?

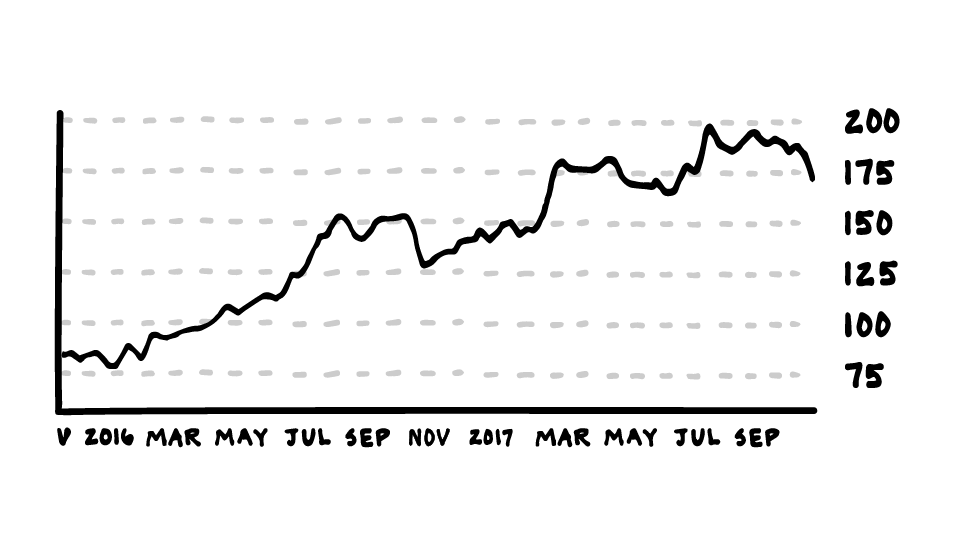

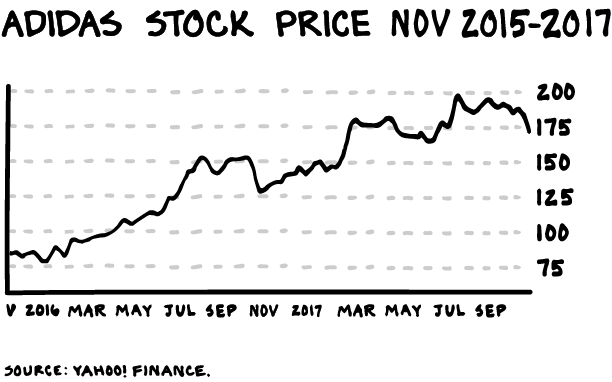

— What’s old is new again. Heritage or vintage product has an interesting blend of trust with new, as it’s from a trusted brand, but we haven’t seen that product in a while. Adidas saw its shares swell 104% in two years on the blend of trust and new we feel with vintage Stan Smiths and Superstars.

— New is a direct function of your supply chain ability. Most consumer boards I serve on try to establish a metric around agility (time from concept to shelf). Agility is the strongest signal when finding drivers of YOY growth among retailers.

— Adding new across the supply chain. If this sounds like a dumbed-down way of saying “innovation,” you’re right. Apple, Warby Parker, and MAC Cosmetics created billions in shareholder value by fomenting new in the retail channel, as achieving new in product was increasingly hard / expensive.

— Embrace new media. One of the new competencies of winners in the consumer space is facility with Instagram. A brand’s facility with new media is an indicator of cool and new — the company you keep, so to speak. Burberry reanimated a tired brand by embracing new media and committing to being the early adopter across every new platform. Being an early adopter is usually expensive, but investing in social media isn’t.

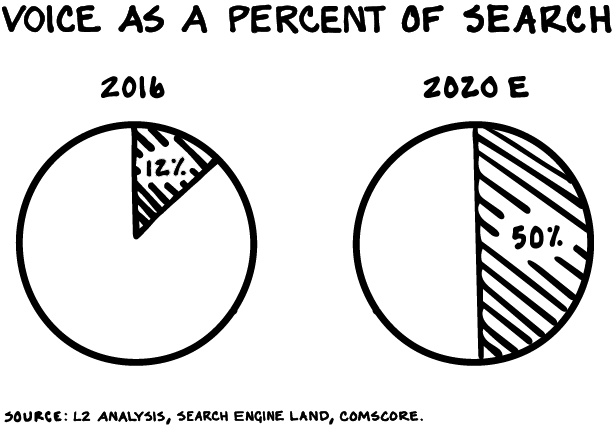

— Embrace voice and messaging. It helps to be a leader and invest early in the medium or technologies that are booming. You have the wind at your back, and those who follow won’t bask in as bright a glow. The greatest opportunity for “new” right now is facility and programming with voice and messaging. Take all your IOT, VR, and 3D printing initiatives and shit-can them (reallocate the capital). Figure out a way to communicate with existing and new consumers via messaging, and encourage people to interact with your product via voice.

Trust me on this …

DOJ vs. CNN

“Save us from CNN,” said nobody, ever.

The Department of Justice has threatened AT&T that it would block the acquisition of Time Warner unless AT&T sells off CNN.

This. Is. Insane.

Some questions for the DOJ:

Isn’t asking AT&T to sell CNN like asking Kenny Rogers to fire his bassist, as he could become too powerful?

Google has 90% share of search, a market greater by dollar volume than the ad market of all nations except the US. But AT&T needs to sell CNN?

Amazon Prime is in 64% of US households and spends $4.5B on content. But AT&T and CNN are the real threat?

The DOJ is worried about vertical — content and distribution. Have you heard Facebook has the distribution of 2.1B users and massive content?

Facebook owns four of the five most used apps in the world, but AT&T needs to sell CNN?

Why do you let big tech play by different rules?

Potential buyers of CNN, like Comcast or News Corp., have their own news channels. Wouldn’t the disposition of CNN create greater concentration of power?

Isn’t the DOJ concerned they are becoming the regulatory equivalent of Sean Spicer, trashing their credibility as they lie for their boss?

Is the DOJ ignorant of tech and media, or is it just Trump’s bitch?

Isn’t this low-budget bluster about to be neutered by US law?

Life is so rich,

0 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com