The Great Rotation

Audio Recording by George Hahn

“Stay in your lane” is a person’s way of saying they disagree with you, but they’re too lazy to counter your point(s) with any evidence or argument. I get this a lot when I talk about politics. Separating business from politics is akin to believing that fish swim independent of the water’s current. America’s toxic uncertainty is urging capital to look elsewhere.

The world’s biggest yard sale is taking place now that brand America is sick, and the world is on the front lawn hoping to pick up $26t in economic activity on the cheap. Capital flows into EU index funds and institutional interest in investing in the U.S. are at 30-year highs and lows, respectively. As such, I believe Europe and China represent investment opportunities. Since the fourth quarter of 2024, I’ve been reallocating capital out of the U.S.

(Note: This post isn’t investment advice.)

Capital Flows

The Amazon River flows eastward across South America for 6,400 kilometers before it empties into the Atlantic. But 65 million years ago — a blink of the eye in geological time — the Amazon flowed in the opposite direction, toward the Pacific. Tidal rivers reverse their flow daily. Others reverse their flow annually as seasons change. Three times this century, the Mississippi reversed its flow during hurricane storm surges. In 1900 civil engineers reversed the flow of the Chicago River, changing its outlet from Lake Michigan to the Mississippi.

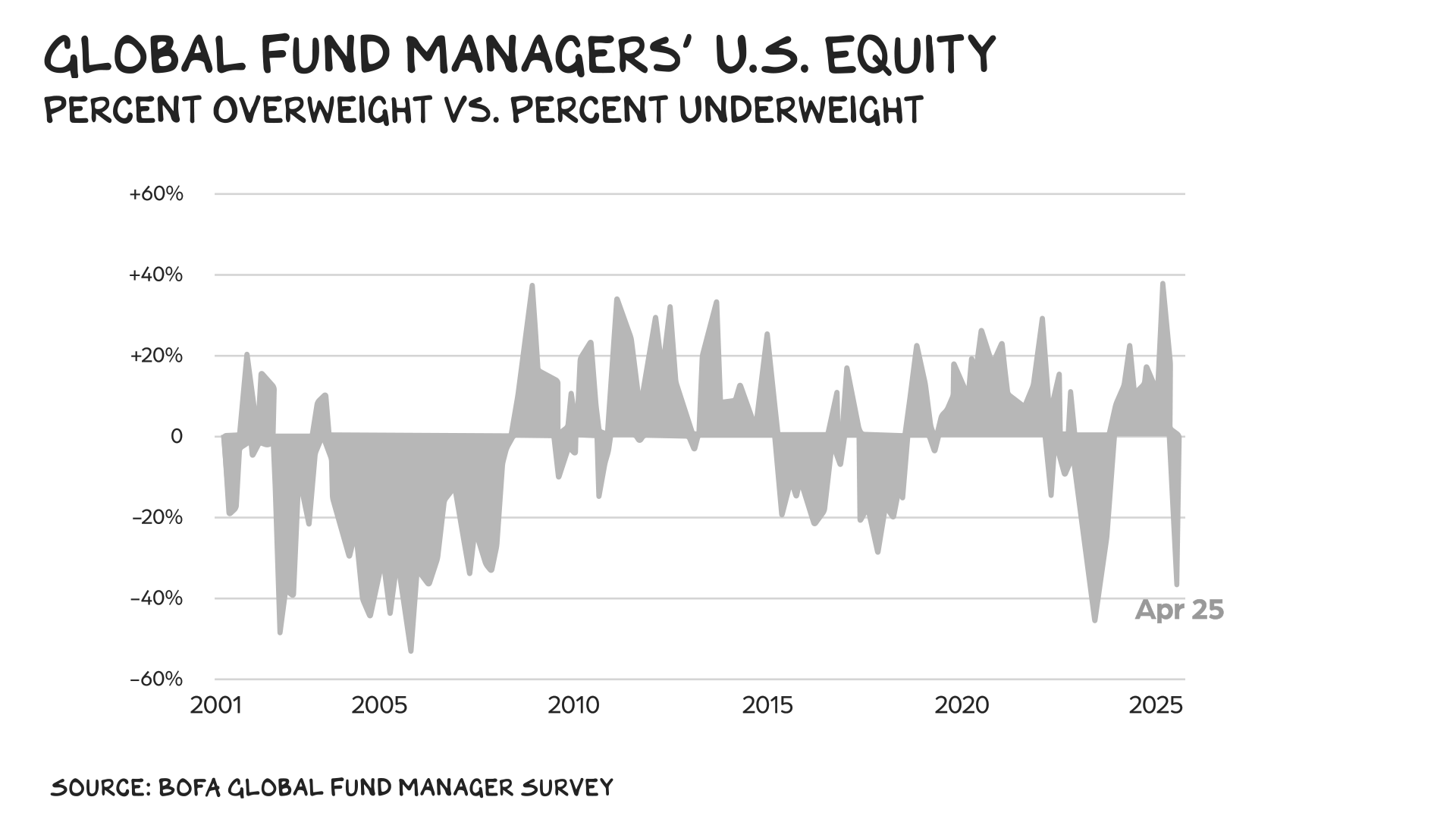

Capital flows also shift cyclically and as a result of human intervention. Unlike rivers, shifts in capital flows can be sudden and violent, as capital does not pledge allegiance, but moves aggressively toward safety and opportunity. In the most recent Bank of America fund manager’s survey, the allocation to U.S. equities fell to a net 36% underweight. That represents a 53-percentage-point swing in the U.S. equity weighting since February — the biggest two-month decline on record. In the same survey, 73% of fund managers said they believed U.S. exceptionalism had peaked. What began as a cyclical movement in capital akin to a river’s seasonal change in direction now resembles a transformation on the scale of the Amazon’s ancient rerouting — though this shift was engineered and accelerated by humans, like the redirection of the Chicago River.

Regression to the Mean

Heading into the recent NFL draft, Shedeur Sanders, the University of Colorado quarterback and son of NFL hall of famer Deion Sanders, was considered a likely first round pick. As it turned out, he was the 144th overall pick in the fifth round, costing him an estimated $40 million. I don’t know what Deion told his son afterward, but here’s what I’d tell mine: You’re better than your worst moments, but never as good as your best ones. This regression to the mean is one of the most powerful forces in the world. Also, Deion should tell his son to tell his dad to shut the fuck up.

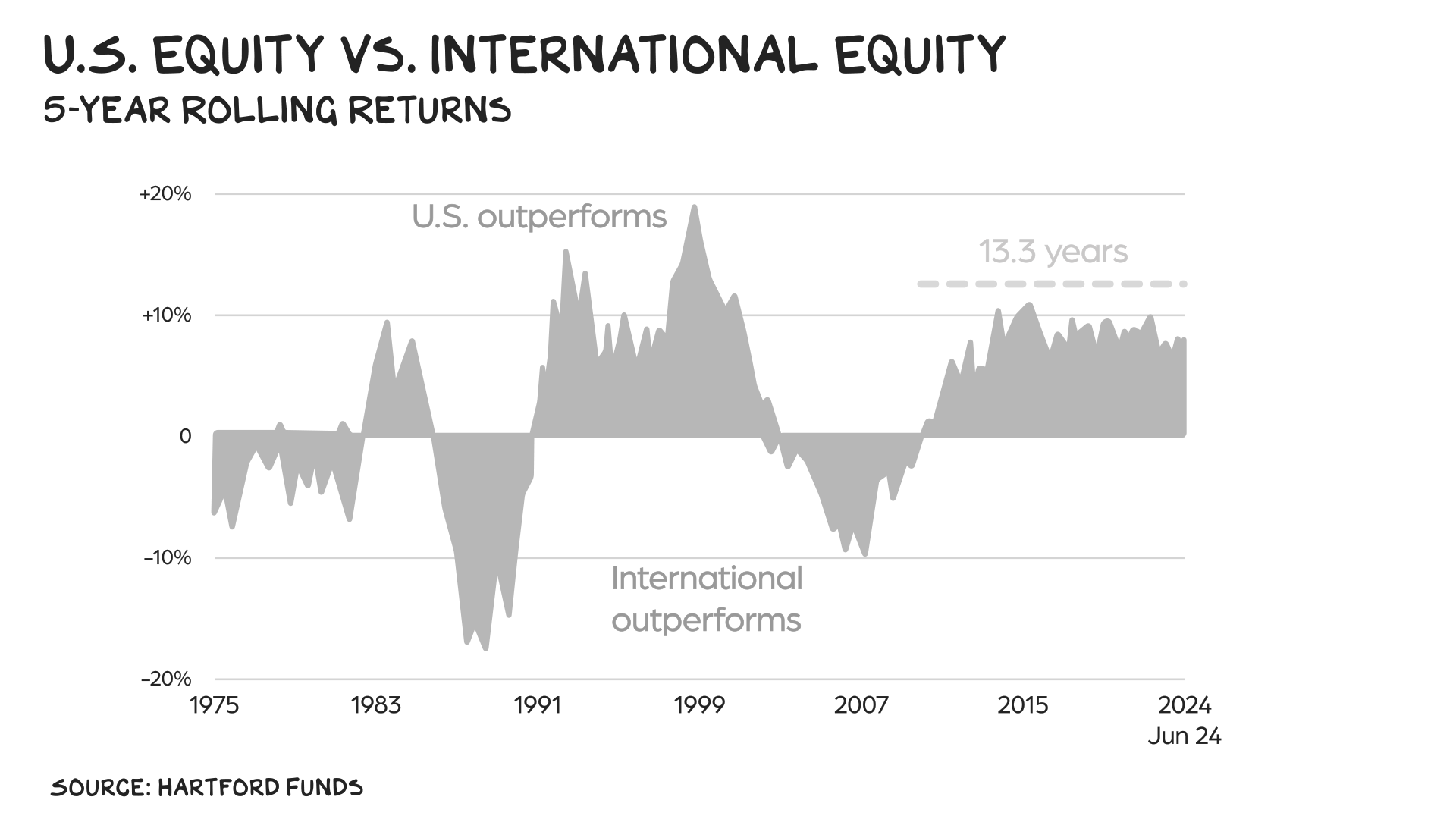

Over the past decade, U.S. equities have delivered an extraordinary 14.8% annualized return, outpacing global ex-U.S. equities (7.0%) and Eurozone equities (7.8%). After a historic bull run, it’s tempting to believe American exceptionalism is a permanent feature, like gravity. Since 1975, however, the outperformance cycle for U.S. vs. international equities has lasted eight years on average. At the end of 2024, the U.S. was 13.8 years into the most recent one. U.S. equities are regressing to the mean.

Overvalued

Eleven months into the pandemic, Warren Buffett wrote in his annual shareholder letter, “Despite some severe interruptions, our country’s economic progress has been breathtaking. Our unwavering conclusion: Never bet against America.” This statement was based on a set of assumptions that our checks and balances protected the U.S. engines of growth (risk aggressiveness, rule of law, IP, university research, attracting premier human capital). Over the past 100 days it appears we’ve taken these things for granted, and I now believe it makes sense to bet on other regions. Over the long run, I’m bullish on America, as there’s no better platform for unleashing human potential. The question isn’t whether to bet against America, however, but at what valuation? BTW, if a human was engineered to be the polar opposite of Warren Buffett, they’d look strikingly similar to Peter Navarro.

During the Great Recession, I bought Apple and Amazon at around $10 to $12 per share. After 15 years and a historic bull run, I’m up around 19x to 22x. (Note: I also bought Netflix at $12, and sold at $10 — I get it wrong all the time.) The chocolate and peanut butter was the combination of great companies priced at historic discounts. Since then, the natural disruptions that bring valuations down and transfer value from incumbents to entrants have been arrested by massive stimulus (i.e., deficits) at the behest of an older generation, which is spending younger people’s money to prop up their wealth. But that’s another post. The Great Rotation isn’t as much a bet against U.S. equities, but simply the recognition that U.S. equities are overvalued relative to those of Europe and China.

The S&P 500 trades at a multiple of 26x; the STOXX Europe 600 Index trades at a multiple of 14x, and the CSI 300 trades at a multiple of 15x. When stock valuations become inflated, future returns decline. I’ve done well with my Apple and Amazon investments, but with both of them trading at multiples of 34x, I’ve begun taking profits and looking for returns elsewhere.

Great Bulls of China

At the start of the year, investors were bullish on China for a few reasons: strong corporate profits, AI breakthroughs, and the apparent easing of regulatory pressure from Beijing. The trade war and fears of a global recession have dampened China’s growth forecasts. The IMF cut its GDP growth forecast for 2025 from 4.6% to 4%. But as I’ve written before, China is better positioned than the U.S. to weather the fallout from a trade war. I also believe that, over the long run, tariffs will always trend toward zero as consumers opt for cheaper goods over … everything.

Anyways, the stocks I’m looking at:

Alibaba

Alibaba, China’s answer to Amazon, saw its stock hit an all-time high in 2020, and since then it’s off 62%. Its co-founder, Jack Ma, disappeared from public view after criticizing financial regulators. He resurfaced in 2023, but it wasn’t until this February that President Xi blessed his return in a meeting with Chinese entrepreneurs, urging them to “show their talents.” As one China-watcher told CNBC, Xi sent a clear signal that China’s policy priorities are private sector growth and AI. Last quarter, Alibaba posted $38.5 billion in revenue — a 7.6% YoY jump and its fastest rate of increase since 2023. Net profit increased 3x YoY, coming in at $6.7 billion. Alibaba’s growth was driven by its core e-commerce businesses and the progress it’s making on its AI-powered marketing tool. The stock is up 50% YoY.

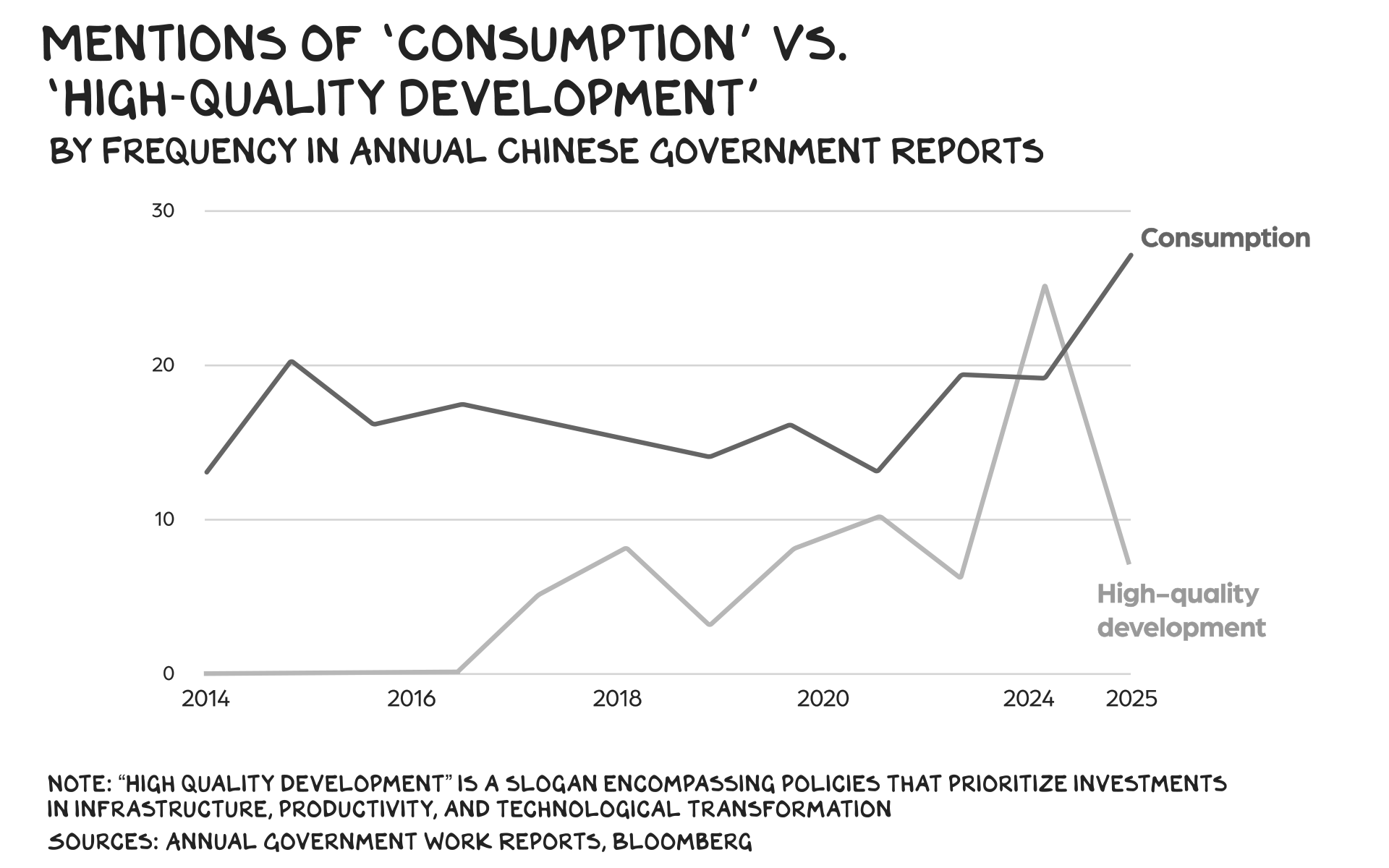

I believe Alibaba is well-positioned to continue to take advantage of the U.S.-China AI race. Alibaba’s challenge is expanding its consumer business units domestically and accelerating cloud growth (up 13% YoY this quarter). China’s household spending is less than 40% of the country’s annual economic output, 20 percentage points below the global average. Closing that delta offers a massive opportunity, and (again) China’s leaders have signaled support for Alibaba. In his annual report to parliament, Premier Li Qiang prioritized “consumption” over long-standing policies aimed at moving Chinese production up the value chain. While there’s concern that Chinese consumers may reduce spending on nonsubsidized goods, it’s worth thinking about what could go right. China may finally become a consumer economy — a transformation that would benefit Alibaba. Finally, BABA’s cloud revenue will likely register a surge as European firms shift their gaze east (away from the U.S.) for cloud services.

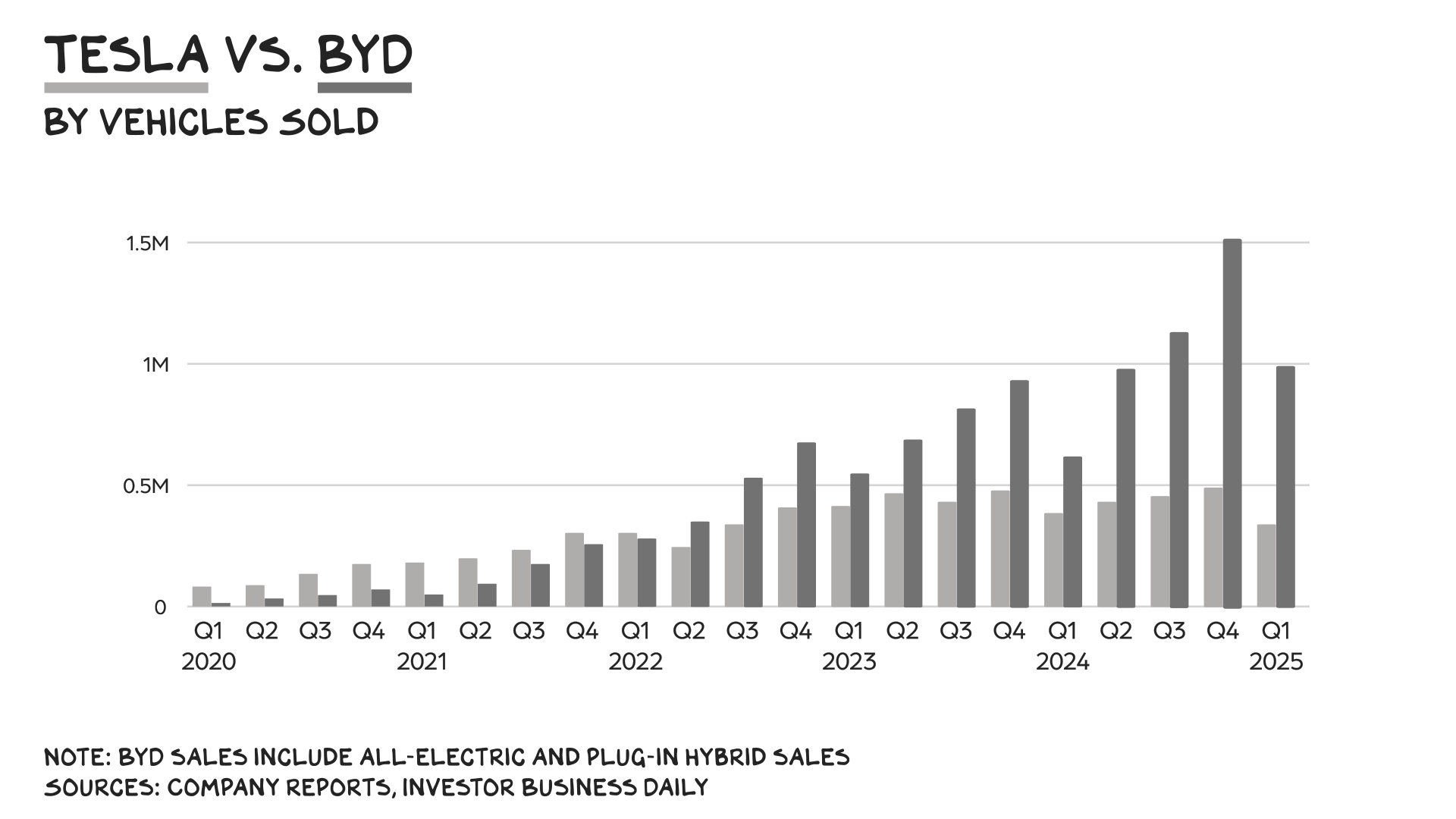

Build Your Dreams

Starting at $8,000, the BYD Seagull has a range comparable to those of other EVs and comes standard with autonomous driving technology, and in the coming years it will receive a battery upgrade with 5-minute charging capabilities. My Pivot co-host, Kara Swisher, really wants one, but they aren’t available in the U.S. — a fact that hasn’t slowed BYD’s growth. Its first-quarter revenue jumped 36% YoY, to $23.5 billion, while its net profit doubled, to $1.26 billion. This year, BYD is on track to sell 5.5 million vehicles, including 800,000 exports and is the fastest growing brand in the UK. Meanwhile, Tesla, which registered a first-quarter sales decline of 13% YoY, trades at a multiple of 130x, vs. 20x for BYD. The Chinese company’s mission is to cool the Earth by 1 degree Celsius, and it just launched its first cargo ship.

Das Bulls

Even before “Liberation Day,” capital inflows to European equities were at a decade-long high, suggesting the Great Rotation was already underway. The trade war has accelerated inflows, but it’s also contributing to a growing sense of European patriotism. In the first two weeks of April, U.S.-focused funds managed by Amundi, State Street, and UBS saw a combined outflow of $4.5 billion. As I previously wrote, America’s retreat from the post-war order it created could be a catalyst for the EU to harness its economic strength and finally become a true union. After Germany’s recent decision to lift its constitutional debt restrictions to boost defense spending above 2% of GDP, the bloc began discussions to encourage other member states to make similar fiscal reforms. A defense boom across the continent keeps Ukraine in the fight, but it’s also an economic stimulus for the EU.

Vertical Aerospace

I try to avoid helicopters. They’re noisy and smell of fuel. To me, helicopters feel flimsy and crude, like a fan stuck on a soda can with duct tape. I spend most of the journey adding up the staggering number of points of failure. Statistically, helicopters are 26x more likely to crash than commercial airplanes, and helicopter crashes are 230x more likely to result in a fatality. The upside? Helicopters are one of the few last-mile solutions at the premier choke point in travel.

I recently participated in a $50 million PIPE in a British company called Vertical Aerospace (NYSE: EVTL) that’s developing an electric flying taxi. Electric vertical takeoff and landing (eVTOL) aircraft are quieter than helicopters and emissions-free, and they have lower projected operational and maintenance costs. They may also turn out to be safer, as eVTOL aircraft use distributed propulsion systems with redundant motors and battery packs. Built for short hops with small payloads, eVTOL aircraft aren’t meant to replace helicopters, but rather create a new last-mile solution capable of delivering people, packages, and meals without having to navigate through traffic jams on the ground.

Currents

The eVTOL sector is in the process of testing and regulatory certification. The FAA is adopting new regulations, while U.K. regulators are using an existing framework for aircraft under 5,700 kg for interim operations and tailoring as they go. Also, the EU has realized that its rich uncle (Sam) has gone bat-shit crazy and can no longer be counted on for support. If the EU, per its claims, increases defense spending from 1.9% of GDP to 3%, an incremental $200 billion more will be spent on defense per annum. This, in my view, could be a turning point for EU stocks and tech firms. This wager is much riskier than betting on BABA or BYD, as the bankruptcy risk is real. The stock is off 97% from its high, and American competitors Joby and Archer trade at 10x that valuation. I see this one as rocket fuel: It’s got enormous thrust (upside), but it’s dangerous (downside).

Restoring Balance to the Universe

I went to a pop-up bar last night run by the doorwomen from the recently burned down Chiltern Firehouse (#enormousfuckingbummer). I believe the universe was not comfortable with me having access (they liked me for some reason) to the best room in Europe. The natural order has been restored, and now I’m back at members’ clubs with other middle-aged men trying to fill the void in their chest with alcohol and clinging to the myth that David Beckham and Guy Ritchie also “hang out here.” Too much?

Anyway, it wasn’t about the venue, but the people in the room. And it’s the same here with VERT. I co-invested with my friend Jason Mudrick (Mudrick Capital). The previous investments he stitched me into returned 4x and 30x. So he had me at hello.

As Brand America shifts from prosperity and rights to oligarchy and corruption, I distract myself with a great American pastime: wondering how I make money here. The greatest own-goal since Brexit/Iraq/Vietnam is underway, and, as in any disruption, there is an explosion in Alpha. It’s fun and (again) helps distract me from watching the pillars that provided me with a life my immigrant parents couldn’t imagine crumble. It helps. Sort of.

Life is so rich,

This week on my Conversations pod I spoke with New York Times columnist David Brooks about the decline of true conservatism and the crisis facing men and boys. Listen on Apple or Spotify or watch on YouTube.

32 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

Propuesta para Profgalloway.

Hola, es un placer saludarte.

Te escribo porque sería interesante comentar contigo la opción de que Profgalloway posicione en los primeros lugares de internet y que aparezca cada mes como noticia en cientos de periódicos digitales, con artículos reales dentro del periódico que no se marcan como publicidad y que no se borran.

Estas noticias se publicarán en más de cuarenta periódicos de gran autoridad para mejorar el posicionamiento de tu web y la reputación.

¿Podrías facilitarme un teléfono para aplicarte un mes gratuito?

Muchas gracias.

I get paid over $130 1 to 3 hours working from home with 2 kids at home. I never thought I’d be able to do it but my best friend earns over $27k a month doing this and she convinced me to try. The potential with this is endless. Heress———–> rb.gy/tzkwnx

ewg8xb

rv2p8u

roulaj

Trump is a straight dollars man. Saudi Arabia is worth more to Trump than Israel. Türkiye is worth more to NATO than Israel.

I have a strong suspicion Trump is going to side-line Israel.

Trump’s administration is doing a deal with Saudi Arabia that does not require it to normalise its relationship with Israel.

Israel is being reduced to being a bystander.

It will be interesting to see how Israel goes with throwing its weight around the neighbourhood now it is no longer considered special by a US administration.

Great article.

To say Trump has massively undermined confidence in America is an understatement. Allies are running for cover and they will likely take much of their billions of dollar in defence budgets with them and spend it elsewhere.

Previously, America’s allies purchased over priced US military weapons because they came with a relationship based on shared security and trust – that is now dead.

US companies got deals because of the US security arrangement that America had with countries. Now that is in the past, US companies are going to have to line up along with world competitors and compete on price and quality. The favoured relationship that gave US companies the edge is gone. Welcome to now competing on price with China!

Trump does not get it. It was the relationship and security arrangement that gave American companies a big leg up when it came to making deals.

In an October 2020 tweet, Galloway called PLTR a “shitty business” and the “Rudy Giuliani of tech” and argued that its high market cap was “disconnected from reality,” given its consistent losses and uncertain path to profitability. He saw the valuation as a symptom of market exuberance rather than a reflection of the company’s fundamentals.

In an October 2020 tweet, Galloway called PLTR a “shitty business” and the “Rudy Giuliani of tech” and argued that its high market cap was “disconnected from reality,” given its consistent losses and uncertain path to profitability. He saw the valuation as a symptom of market exuberance rather than a reflection of the company’s fundamentals.

aren’t these tariffs simply a tax increase on consumer goods for the poor, which Trump will use to lower taxes for the rich?

Fuck I wish you would run. Was sick last week and gorged every episode i could find on Youtube and now smashing through your audiobooks. Brilliant as always, many thanks.

I came to you with a bit of DC insider talk a while back about how the Washington Times gets others to go after its staffers, helping it do the brainwashing thing. The Washington Post did a story back in 2000, with Dick Cavett and others talking about how DC lefty types bully TWTers, and I’ve heard enough about the brainwashing thing to know that those bullies end up helping the Moonies.

I’d still advise anyone who went after anyone for TWT to start reflection on your own thought patterns, just in case the Unification Church (TWT’s owners) got into your brains, too.

I doubt you’ve got much useful info in your brain if you’re out bullying people to help the Moonies, but TWT could have it.

Agree with the content re rotations and reversions to the mean. The longer term question is will the rotation slow or reverse if America can claim back some exceptionalism if/when Trump and the Republican Party as they are now are constrained and hopefully kneecapped.

Expert in politics, expert in marketing, expert in parenting, expert in bitterness, expert in Trump derangement syndrome …..blah blah blah

Least important correction, Sanders went to University of Colorado, Boulder. University of Chicago football, please…

I fear I am a boring broken record, but excellent column as usual. Perhaps you need a thumbs up (and maybe thumbs down) button to avoid textual attaboys like mine. I would add that, contrary to other comments, I think you should write about Trump either implied or directly to the extent you think it important. I think your judgement is sound on that topic.

Scott, I always appreciate how honest you are. Things truly do look dark in many places around this world, and also there is still light here and more light that will come again.

Your conclusion (“It helps. Sort of.”) is also honest…and makes me think of Mark 8:34 – 37

It’s the only way to get out of the myth that we can earn / buy / invest / succeed / achieve to peace and finally filling that whole in our chests.

BYD have been fudging their figures for years. If you need first hand evidence have a look at the EV graveyards across China where fully registered vehicles are sent to rot. Critical thinking needed here folks. Understand the CCP chess play and you can be a more savvy investor in BYD.

Zillow and the rest of the profited from the.subprime debacle and fraud that crashed the real estate market.

Now being the rest of the rent economy leeches are further distorting values and hel o ing create more homeless people.

May they all rot in hell.

Current fiscal and social policies often fail not due to a misunderstanding of the challenges we face, but because the solutions offered are ineffective and counterproductive. Chief among these is the reliance on printing and distributing money, which results in debt accumulation and eventual insolvency. An alternative, long-term strategy centered on effective asset management of all government land, minerals, energy, and SS funds would solve our debt and deficit problems in as little as10 years.

The middlemen are so angry right now.

are you ever going to write about anything non-Trump? I think we get the picture now. can we get back to markets, trends, demographics, big picture stuff that is NOT Trump related? Your weeklies were a place I could come expand by worldview on economics, and culture and evreything else. but everytime you write and I read about Trump, my mind shrinks. touve become like the Late night Kimmel & Colbert. thy used to be funny & creative. now they’r just shells of who they were. Fallon has 100x the creativity in 1 show Kimmel has in 1 week.

He didn’t mention trump a single time in this article. I did a quick “CTRL+F” and the first time on this page the name was mentioned was in your comment. Get over yourself.

Right? Trump has next to nothing to do with this post, it’s the cabal of loons who are whispering in her ear.

Can’t wait for this post…..I can add an analogy which is as true but, hopefully, will get people angry enough to recognize what is happening and start to demand our political representatives stop allowing it to continue. The younger generation cannot be heard but we can: “Since then, the natural disruptions that bring valuations down and transfer value from incumbents to entrants have been arrested by massive stimulus (i.e., deficits) at the behest of an older generation, which is spending younger people’s money to prop up their wealth. But that’s another post.”

Scott: Your advocacy for young men and PK-12 public school children is outstanding. Your loathing for President Trump makes you myopic and another source that I cannot trust. If you can’t see some of the positives in Trump’s 100 days and the opportunities for the U.S. economy, I recommend you stay focused on advocating for our young people.

agree w Eric. just stop writing about Trump, Scott. he Won. we know where youstand on him. got it. thanks. now, get back to being great by being Scott, not by bashing Trump. more is not better its just more.

But the Assclown president is a supreme cunt.

I get the theoretical argument: reversion to the mean, expensive US stocks, and so on. But in practice, I don’t see clear green shoots anywhere. The US pulling back from global trade won’t be offset by Europe, Japan, or the Global South without harming their own industries. While the US has real challenges, other regions are in equal or worse shape.

It’s similar to the reserve currency debate. The US has overspent and misused its position, but there’s no viable alternative yet. So despite good reasons to be skeptical of the US, there’s no clear bull case elsewhere either. In reality China has serious demographic and structural issues, which make it challenging for it’s future prospects (We’re looking at a similar situation as Japan in the 80s, where things look good from the outside, but it simply won’t sustain).

We’re probably heading into a period of messy, sideways growth. The US could just as easily reassert global dominance in five to ten years as we could see a shift toward international outperformance. Your chart might still be directionally right in relative terms, since US equities have further to fall, but that doesn’t mean strong investment opportunities are emerging elsewhere.

Scott panic sold out of US equities the first time Trump got elected, and now he is letting his politics influence his investing decisions again. It’s hard to argue that EU with its strict regulatory environment, or China with its fascist government and 40% savings rate, deserve the same P/E multiple as the US. No thanks Scott, I’ll bet on Warren Buffett’s thesis over yours.

You mean the same Buffett who shifted $300 billion to cash in recent months?

Yes – but Buffett has been building cash for well over the past year. He also shed a significant portion of his Apple holdings before it tanked. I don’t think Berkshire is investing very much in China or Europe.