The Algebra of Wealth

My next book is the product of a lifetime spent as a founder, professor, parent, and mentor. The Algebra of Wealth contains 300 pages of insights and hard lessons drawn from experience, paired with the best research on the foundational question of prosperity: how to achieve financial security. The book comes out on April 23, and between now and then I’ll be sharing eight short excerpts and summaries of key points with our readers. We’re still writing No Mercy / No Malice every Friday; we’ll share Algebra of Wealth content on Mondays.

We started work on this book several years ago, inspired by a No Mercy / No Malice post about the difference between having money and being rich, and how to achieve the latter. It was one of our best-received pieces when we ran it in February 2021. In anticipation of the book it grew into, here’s that initial post.

[The following was originally published on February 12, 2021.]

I know a lot of people who make an extraordinary amount of money, but few people who are rich. Rich is having passive income greater than your burn. People on a path to money focus on their earnings; people on a path to wealth also focus on their burn. Joseph Heller said, “It takes brains not to make money.” (I think he was casting a favorable light on his starving artist friends.) This may be true, but it definitely takes brains to hold onto it (money).

My father receives $48,000 per year from Social Security and his Royal Navy pension (he was a frogman). He spends $40,000, and that’s enough to make him happy. He swims every day, watches a shit-ton of hockey (Leafs fan), and on Fridays goes to the Taco Stand (an actual restaurant in La Jolla) and orders something called a michelada. (Apparently it’s medicine delivered in a chilled, salt-rimmed glass — he claims his hair is regrowing and that he’s sleeping better. I believe half of that, so … I believe it.) Anyway, it’s not your income, but your income-to-expense ratio, that determines if you’re rich.

My observation is that there are four variables in the algebra of wealth: focus, stoicism, time, and diversification.

People conflate a lack of focus with a lack of talent. Intelligence and talent are correlated with success, but the strongest signal of future success is your perseverance and resilience: what the books in airport bookstores call “grit.” Unless you are supremely disciplined, your career will have to be something that gives you some enjoyment. But don’t mistake focus for your “passion.” People who tell you to follow your passion are already rich. Follow your talent. The accoutrements that accompany being great at something (relevance, admiration, camaraderie, money) will make you passionate about whatever “it” is.

Focus on putting yourself in a position to be financially successful. Get certified: In a digital world, much of the corporate world decides whether to swipe right or left based on the logos (aspirational universities/firms, vocational certifications, etc.) on your LinkedIn page.

Sector dynamics will trump your talent. (I realize how awful that sounds.) However, someone of average talent at Google has done better over the past decade than someone great at General Motors. Be thoughtful … any opportunity you have when you’re young to choose among different paths is a profound blessing.

Look for the best wave to ride. Twenty-five years ago, I chose to paddle into the e-commerce wave. My first effort (Red Envelope) failed. Even worse, it failed slowly … over 10 years. I stuck with it and started a firm that helped other firms develop e-commerce strategies (L2) and have owned Amazon stock for 12 years. It took me a while, but the strength of the wave kept me moving, and carried me to the beach. I just read the last sentence and am fairly certain I will never be a truly great writer. Anyway.

Focus on your relationships. Family and friends are essential to long-term happiness, and the most important relationship is with your spouse. The most essential economic decision you make will be who you decide to partner with or, more specifically, who you decide to have kids with. The net worth of married people grows 77% larger than that of single people. Marry the right person, and then invest in that relationship every day. You’ve wagered 50%+ of your net worth, and your value in the marketplace, on that partnership. Don’t keep score, and bring forgiveness, generosity, and engagement. In sum, show up.

Determine what you can and can’t control. You can control your reactions to temptation — a lack of discipline is the antichrist to economic security. Our society of superabundance makes this difficult. Billions of dollars are spent every year on schemes to manipulate our natural impulses into spending more money, consuming more fat, and believing everyone around us is more successful than we are. The upgrade from economy to premium to business to first class to private jet can seem like an investment in yourself — it’s not. The most powerful forward-looking indicator of your financial freedom is not how much you earn, but how much you save.

A specific activity accelerates in a bull market, conflating luck with talent and dopamine with investing. Diabetes, high blood pressure, and sharing a screenshot of your Robinhood gains are maladies of industrial production that exceed our instincts. Trading — distinct from “investing” — can feel like work and productivity. It’s not. It’s gambling, but with worse odds and no free drinks. One study found that over a 12-year period, only 5% of active retail traders made any profit at all. This time around, apps including Robinhood, with its dopamine-triggering confetti, and 24-hour-a-day, volatile crypto trading are the drugs of choice. Most day traders will be fine, suffering affordable losses … most. However, for many there are darker outcomes. Young men are especially vulnerable, as they are more risk aggressive. Between 80% and 85% of day traders are men, and 23% of men who gamble become addicted (as opposed to 7% of women). Most of us can gamble without becoming addicted, just as most of us can drink without becoming an alcoholic — but know the risks.

Stoicism is not just about remaining calm in the face of temptation. It means having good character. Succeeding in life is much easier if other people want you to succeed. We have a mental cartoon image of rich people as grasping and cruel. The reality, in my experience, is that wealthy people, in general, demonstrate strength, acumen and … kindness. Economic security is in the agency of others, and you want others to want you to win.

I spent the first 40 years of my life chasing some form of Western relevance so I could register more dopamine surges. Nothing was ever enough. More, I want fucking more … now. The pursuit always managed to distract me, and I was unable to get the engines of success and fulfillment firing on all cylinders. This stage of my life was characterized by fits of progress, getting close, but never achieving anything resembling the potential my opportunities warranted. In one moment that all changed for me: When my first son came rotating out of my girlfriend 13 years ago. In sum, shit got real. I was young enough to be selfish, but old enough to recognize it and acknowledge that I needed to change. I decided at that moment (no joke) to bring more focus and discipline into my life.

“Time is the fire in which we burn,” says the poet. It is our most inflexible and valuable commodity, the one thing with which you should not be generous. Squander money, you may earn it back. Squander time, it is gone forever.

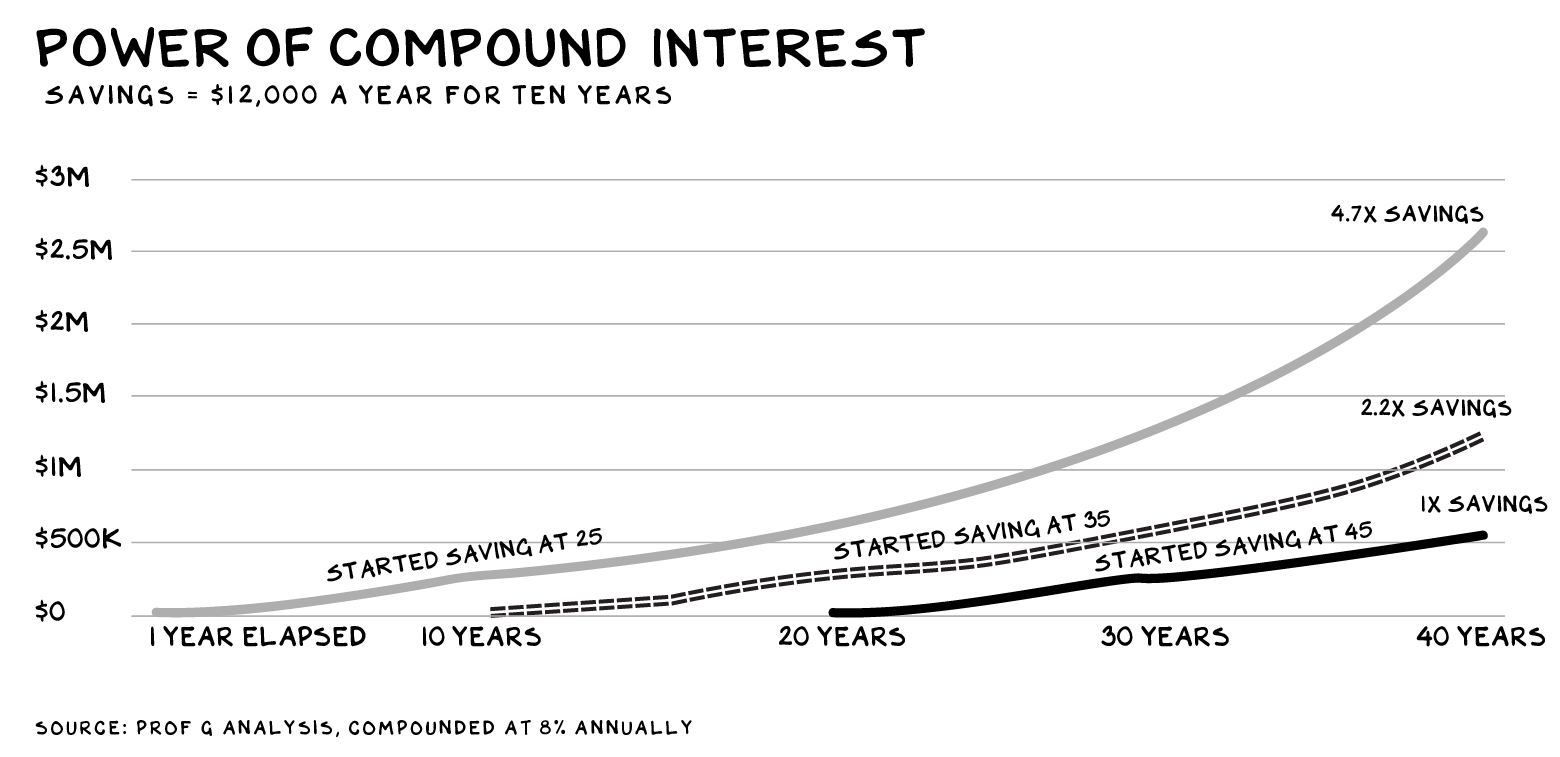

Re investing: The long term is our ally, the short term our nemesis. The gangster authority on time, Albert Einstein, supposedly remarked that compound interest is the eighth wonder of the world. Yet our brains are not wired to understand this. When I was 26, I thought of being 46 as the distant, irrelevant future. Now that I’ve reached that age (actually I’m 56 … ugh), 26 feels as if it was last year. But small investments I made a decade-plus ago have grown into the base of my economic security.

Compounding is not just a financial thing. The most important returns in life come from the compounded effects of our investments over time, whether in our finances, careers, hobbies, or relationships. Change the timescale of your life, and you change your life.

In your life, focus is key. Plan A for financial security is being great at doing something the market values highly, and leveraging that into income and/or equity in a business. But Plan A squared is investments. And with investments, focus is to be avoided. Diversify and, unless your plan is to be in the finance industry, be sure that your time spent tracking/trading does not distract you from what is/should be your source of income and savings.

Investing over the long term pays out, but there are always dips along the way. Diversification is kevlar — with it, bad decisions will still hurt, but they won’t prove fatal. Diversification, in other words, is your bulletproof vest.

A few of my many egregious investing errors:

- Red Envelope: I was so emotionally involved (I co-founded the firm in 1997) that I kept putting money into the business and ended up losing 70% of my net worth when it declared Chapter 11 in 2008. I had no kevlar, as I was terribly concentrated in one asset.

- Netflix: Yes, Netflix. I believed in the company, respected its management, saw its potential, and bought a lot (for a professor) at $12/share. That’s the good news. The bad news is that I sold it six months later at $10/share to capture a tax loss and never re-bought. Today it’s at $558. Not that it doesn’t haunt me … every day. Nope, definitely not.

Most of my major mistakes in investing can be distilled down to two things: not diversifying, and trading.

Mistake No. 1 (Red Envelope): Almost fatal. I was 43 and outwardly successful. But with the birth of my first son, I was feeling more economic anxiety than I had since I was a kid. (I grew up in a household with a single mother who worked as a secretary.) Mistake No. 2 (Netflix): Painful but nowhere near fatal. I had eggs in other baskets (i.e. Amazon, Apple, Nike, Oracle). In the end, my kevlar has been not allocating more than 10% of my net worth to any one investment. That doesn’t mean I don’t look for opportunities that offer asymmetric upside — I do. I just don’t ever take off my kevlar. You don’t need to be a hero to get to economic security.

Not Your Fault

These principles have served me well, especially as I’ve become more disciplined about following them. But while I wasn’t born into wealth, I did benefit immensely from the circumstance of my birth. My smartest move was to be born a white male in California in the sixties. An America that loved unremarkable kids presented me with a world-class education (at the time, UCLA had a 60% admissions rate and cost just $400 a semester), thrust me into the financial boom of the 1980s, and, through sheer luck, positioned me to catch the internet wave.

Since I set foot on the UCLA campus in the 1980s (feels like just last year) we’ve told ourselves we remain the Land of Opportunity, and that we’re making progress to remedy our historic imbalances. Yet as illustrated by one metric after another, economic security is harder to obtain, not easier, and is becoming less a person’s individual fault and more a result of circumstance … America is becoming less, well, American.

Are we headed for another revolution? I don’t know, but we are due for another righteous movement. What can you do in the face of a system that profits off you becoming overweight, indebted, divided, and addicted? Answer: Rebel.

Focus on what matters. Be a Stoic in the face of temptation. Use Time to your advantage. Diversify your investments.

In any economic climate, how do we build economic security, foster love, and find joy? How do we get rich?

Slowly.

Life is so rich,

P.S. You can pre-order The Algebra of Wealth here and receive it on April 23.

28 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

Getting the inside track on the fire sale of a company that sells blueberry vaping cartridges doesn’t hurt either.

enjoing your articles in some hidden corner in Africa …

and convincing myself that even though I have nothing to show for my worth well am heading in the right direction..courtesy of your timeless and precious bits wisdom.

yamune

Great article. Wondering if and how your view on diversification may change if Red Envelope was a huge success, a tail event that single handedly made your investment successful.

I deeply admire the way you’ve intertwined the impact of fate AND personal qualities as determinants of success. Doing so in an entertaining way is the cherry on top. Thanx.

Until now I have suggested NM/NM to my older friends and often forwarded the newsletter for them to consider subscribing. With this Algebra of Wealth newsletter and announcement I am hereafter making the same recommendations to young folk including family, friends and former students. Over years I have preached much of the same to those listening in my classroom. With this formula F=S+T+D I see the real benefits should be available to young peeps anywhere and everywhere. Thanks Doc.

Scott

This week you gave me a substantiation of my values when it comes to investing and spending. I’ve followed this for a lifetime. I do see now that there is more spending in society, and it’s got to be watched. This is good advice Steve Guttenberg

Excellent article. I wish I had found it 25 years ago, but then again, even if I had, I don’t know that I would have understood it.

Scott, I would love to see an article for how those of us who did not practice this formula for wealth can still succeed. I am 48, own a couple of homes, have $250k in index funds. Sounds like a lot but astute readers, as well as you Scott, understand this is not very much at all. Not in today’s world, nor the world that is coming in 12 short years when I would like to retire.

Love the posts. I read every week. I want to share the content with my kids, but you have to censor that f-bomb that creeps into every post. That will unlock into a broader community.

In a post about building wealth, the salient point is this: “What can you do in the face of a system that profits off you becoming overweight, indebted, divided, and addicted? Answer: Rebel.” Perfect, PERFECT Prof G.

Add to that prices (for things like food and cars) just keep going up (but inflation is down?), corporate profits are through the roof and housing (to buy and to rent) is becoming unaffordable to larger and larger numbers of Americans. We’re becoming a feudal state. And it isn’t sustainable. There are too many guns in the hands of too many Americans. Prof G says: “Are we headed for another revolution? I don’t know, but we are due for another righteous movement.” Yep. We’re headed for a reset. You’d better have your bunkers ready.

Regarding your happy father: Charles Dickens, in 1849, on the relationship between money and happiness: “Annual income twenty pounds, annual expenditure nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pound ought and six, result misery.”

I always liked the saying, “being rich is having money, being wealthy is having time”. Do not underestimate the value of controlling your own calendar

Excellent article, thank you. What jumps out to me is reality and luck. Excepting what you are good at and what you are not should be a driving force in what career direction you take. Once done, there’s no doubt that luck plays a large part in moving you forward. Being at the right place or working with the right people-gold!

Long-time follower, first-time commenter. This is the best post you’ve ever shared. Keep up the good work, Prof!

on the income to expense ratio observation, it’s worth referencing the source:

“Annual income twenty pounds, annual expenditure nineteen nineteen and six , result happiness.

Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery”

― Charles Dickens, David Copperfield

Preordered for Germany. Looking forward to read the book.

Keep on making a ruckus!

You just wrote a part of my life,,,,, lot of similarities keep the great work

As always, terrific and salient thought leadership, Scott. I’ll be sharing with my college-age sons. Thank you.

People don’t like to acknowledge that spending very little is a way to accumulate money.

Thank you, thank you, thank you, thank you, thank you and THANK YOU

So true….and I wish I would have had the wisdom to find/follow these “rules” when I was 25….

Thanks for this post! This was all I needed today.

Sir…You are a great writer! Great writers, performers in general, the great ones especially…they all say that they are shit…makes them work their craft until they master it! I want to receive Monday emails just so I can be enlightened…To old and have made to many mistakes to put your advise to good use…But!…I can pass it along like I know what I’m talking about!…Thanks Prof G!

This is a powerful article and reflects my own experience. I’m going to try to summarise it in more simple wording for my 18 year old granddaughter.

I’m still laughing in sheer delight! My NYC banker nerd son brought your columns to my attention here in flyover country. I was just thinking, this man needs to write a(nother) book…and you did! At 80 I know time is my friend when it comes to being rich and getting richer every year. Just for the hell of it, to see if I can. It was the tortoise who won the race. IMHO Being a rebel is your best advice to date. Good going, Professor. From my vantage point, I gently suggest that the best for you is yet to come. Congratulations on your good common sense!

Well done, Scott! You are right about so many things, especially about how getting a first class education was easy in California at one time. Now it’s around $550/unit (not course, unit!) at Cal States. I’m forwarding this column to my grandkids whose burn rates surge past their incomes. I hope they pay attention to you!

Bummer about your Dad being a leafs fan!

Thanks for trying to help us stupid paupers.