MeWork

I’ve lost a lot of other people’s money. The most stressful times in my life have been when people believed in me and invested tens (if not hundreds) of millions in my company or idea, only to see their capital go up in smoke. I’ve also made a lot of people a lot of money — but only in America would someone with my (lack of) pedigree be given this many swings at the plate.

To be a truly great investor or operator/CEO, you need to be a bit of a sociopath: You have to be able to sleep at night even as you lose other people’s hard-earned money or lay people off. Working with OPM (i.e., Other People’s Money) is often phrased as a positive, but the real luxury is to be in a position to lose your own capital. If things go wrong, it’s a private failure.

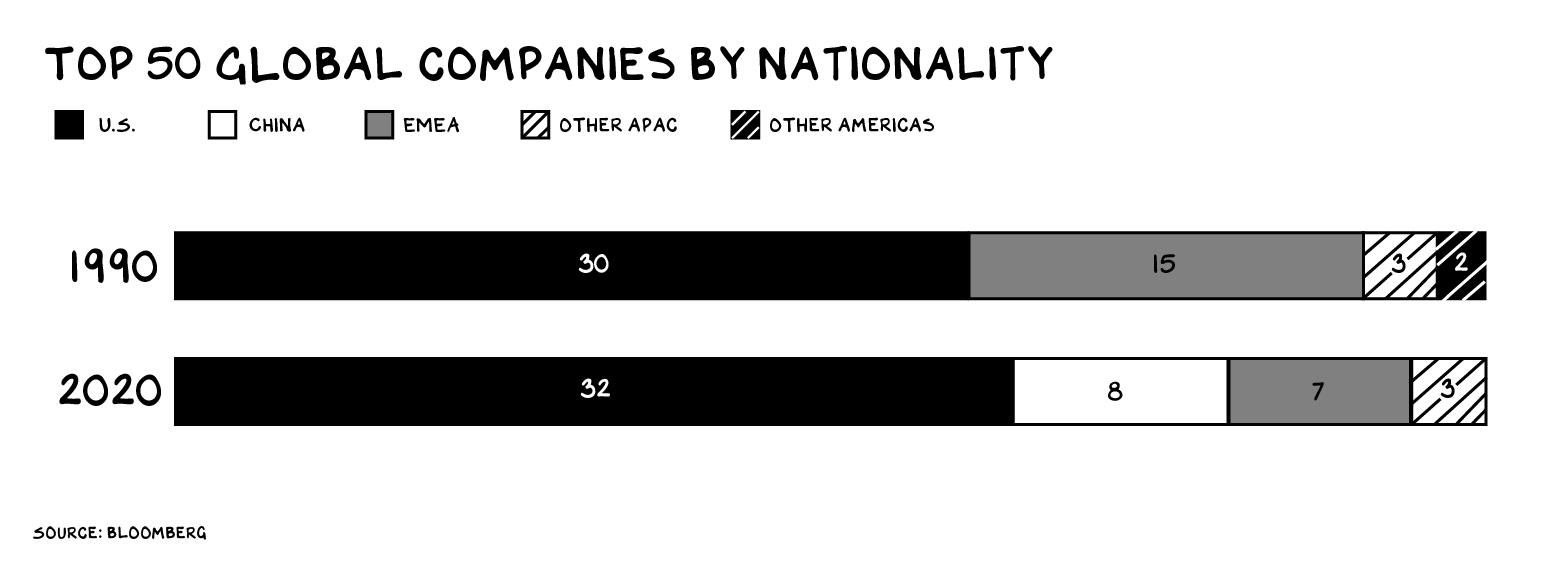

The willingness to risk capital on a captain and harpoons (the 19th century whaling sector was proto-venture capital) has always been a key ingredient in the secret sauce of the U.S. economy. But the secret is out. While the U.S. still produces the most unicorns, and the most mega-corporations, China is gaining … fast. Interestingly, despite the rhetoric re China challenging U.S. hegemony, it’s European innovation that has drowned in the rising red tide. But that’s another post.

We should celebrate billion-dollar successes, so long as they come at the risk of failure — the whaling captain and the entrepreneur earn their wealth in part thanks to their willingness to come home empty-handed, or not at all. However, there’s a new class of billionaire in America. Meet the MeWork generation, which makes their fortunes despite returning to harbor with less than they embarked with.

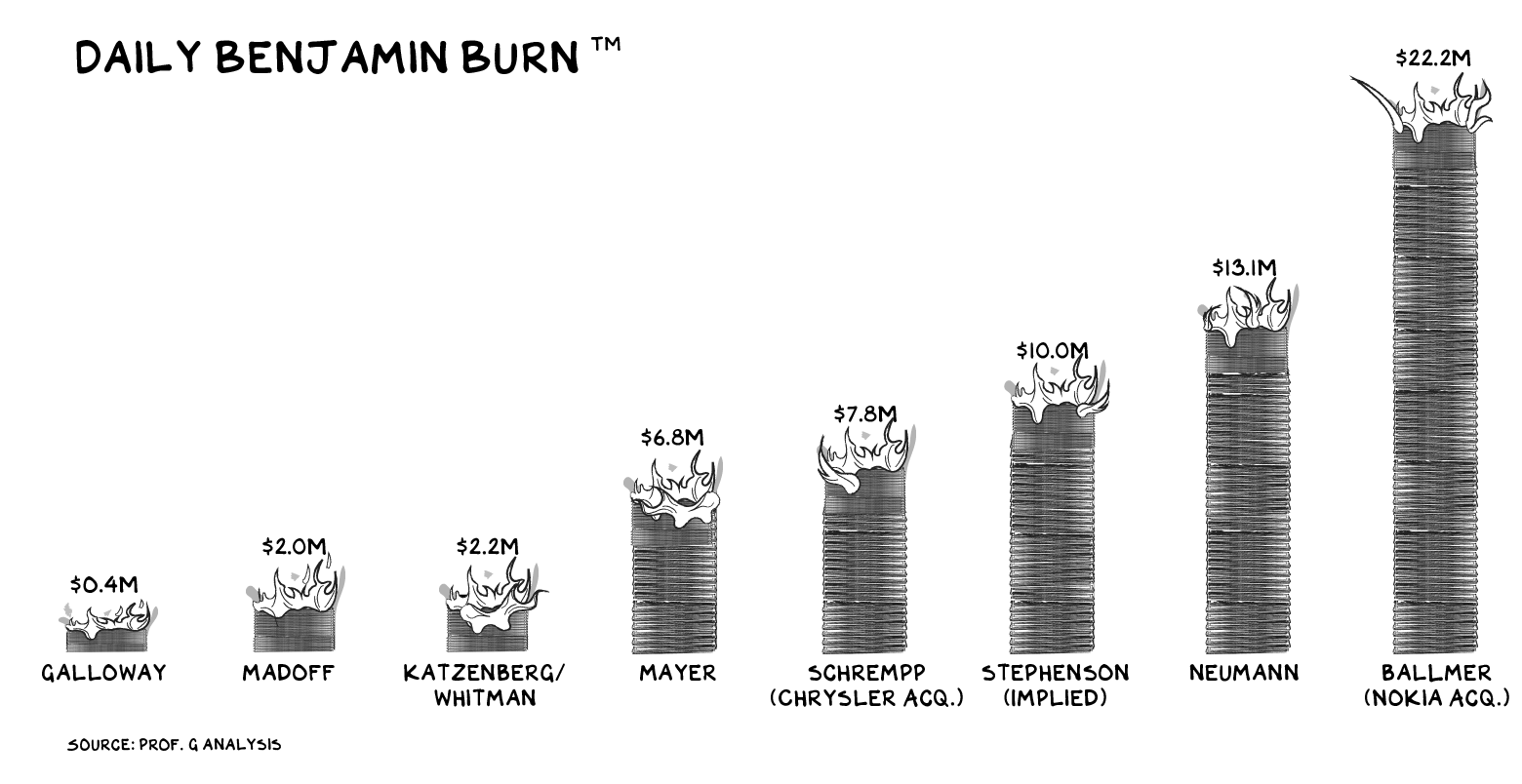

To help identify members of the MeWork generation (they can be any age), we’ve devised two metrics: the Daily Benjamin Burn™ (DBB) and the Earn-to-Burn Ratio™ (EBR). The first is how much money an executive lit on fire per day during their tenure. The second is the percentage of those lost Benjamins they siphoned off for themselves — think of it as a commission on destruction. In an efficient and fair (dangerous word) market, the EBR ratio would be zero. If we can measure someone’s burn in daily stacks of 100-dollar bills, they’ve created no value and should get no compensation. Spoiler: That’s not what happens.

Daily Benjamin Burn™

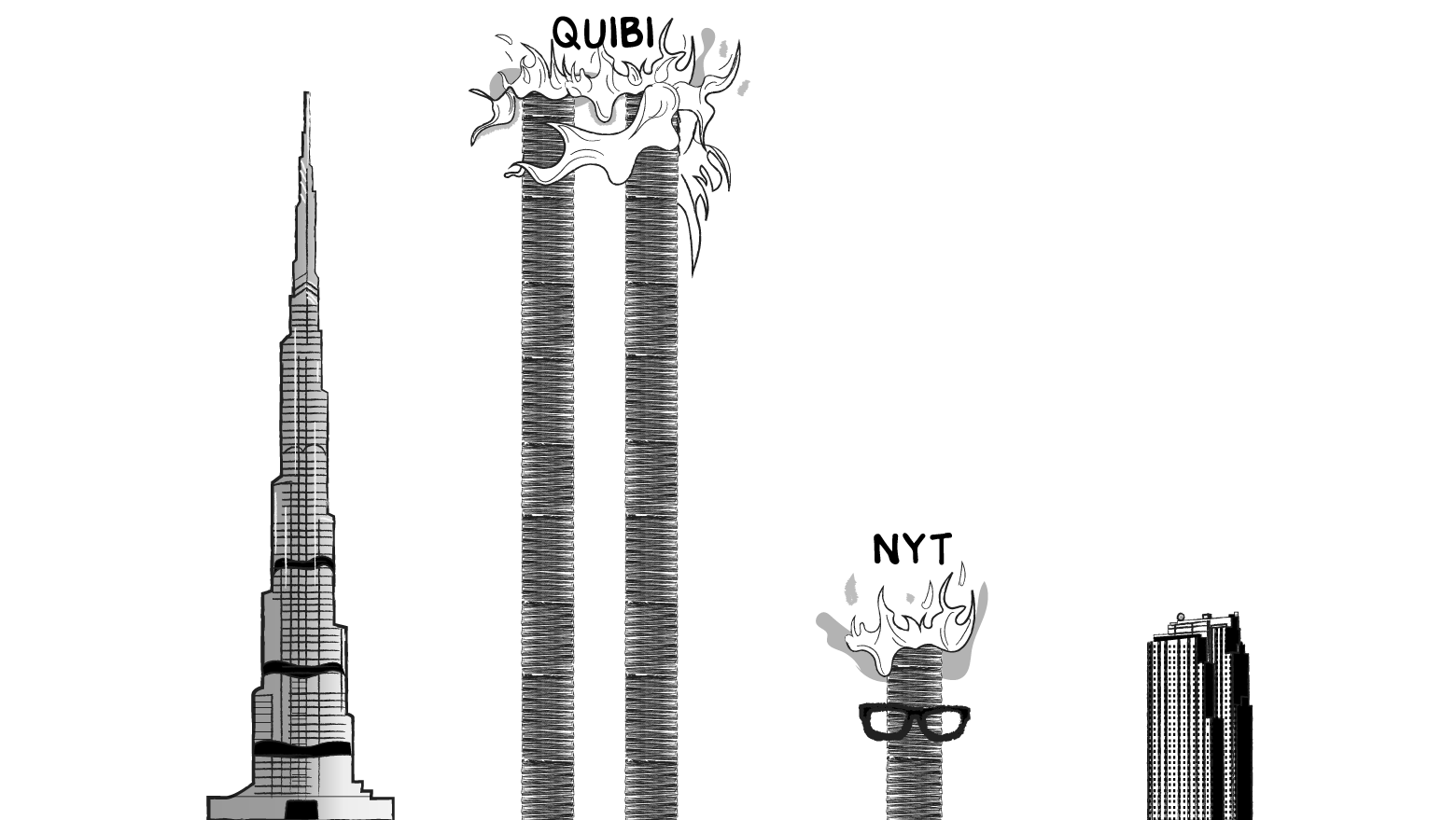

What does the DBB look like in practice? A lot like Quibi. That likely won’t mean anything to you, unless you’re one of the dozens and dozens of people who subscribed to the short-lived short video service. In 2018, Jeffrey Katzenberg and Meg Whitman raised $1.75 billion, launched a bad app with worse content, and shut it down six months later. Roku combed through the rubble and found $100 million, so Jeff and Meg immolated $1.65 billion in 750 days, or $2.2 million per day. If you stacked that $1.65 billion in 100-dollar bills, you’d have a pile over a mile high, about two Burj Khalifas, the world’s tallest building.

Eating My Own Benjamins

In 2008, I raised $600 million from a hedge fund, became the largest shareholder in the New York Times Company, and ran an activist campaign against the Gray Lady. They put me on the Board, where I ranted about the evils of Google, advocated for the divestiture of non-core assets, envisioned sunlit uplands of subscription revenue and … lit Benjamins on fire. During my 24-month tour of duty watching the Great Recession kick ad-supported media in the groin, I managed to turn $600 million into $350 million, for a DBB of about $350,000. The stack of Benjamins I lost would have reached only to the top of 30 Rockefeller Plaza. Only. Jesus …

I. Want. To. Throw. Up.

Earn-to-Burn Ratio™

Jeff, Meg, and I all made an old-school mistake. We failed to find a greater fool (e.g., the public markets, gullible board members, SoftBank) to secure a mega payout for our Bonfires of the Benjamins. I was paid approximately $500,000 in board fees and a retainer from the fund; I speculate that Jeff and Meg pocketed more (their compensation remains private). But none of us took home millions.

That brings us to the Earn-to-Burn Ratio™ and the Hall of Fame for broken compensation.

EBR Hall of Fame

In 2012, Yahoo replaced its CEO with an executive from Google: Marissa Mayer. But the new CEO made a series of poor decisions, including canceling the company’s telecommuting policy while working from home herself and paying $1.1 billion for a porn site, Tumblr. (Note: Six years later, Yahoo sold Tumblr for $3 million.)

When Mayer took over, Yahoo (not including a 20% ownership stake in Alibaba) was valued at $14.4 billion. In July 2016 the company sold itself to Verizon for $4.5 billion, and Mayer was gone. That’s $9.9 billion turned to ash in four years (or 13.5 Burj Khalifas), for a DBB of $6.8 million. Mayer’s compensation began with a $30 million signing bonus and went up from there, totaling an estimated $365 million, giving her a $250,000-per-day commission for destroying $7 million per day of other people’s money. That’s an EBR of 3.7%. Shocking, sure, but not the gold standard.

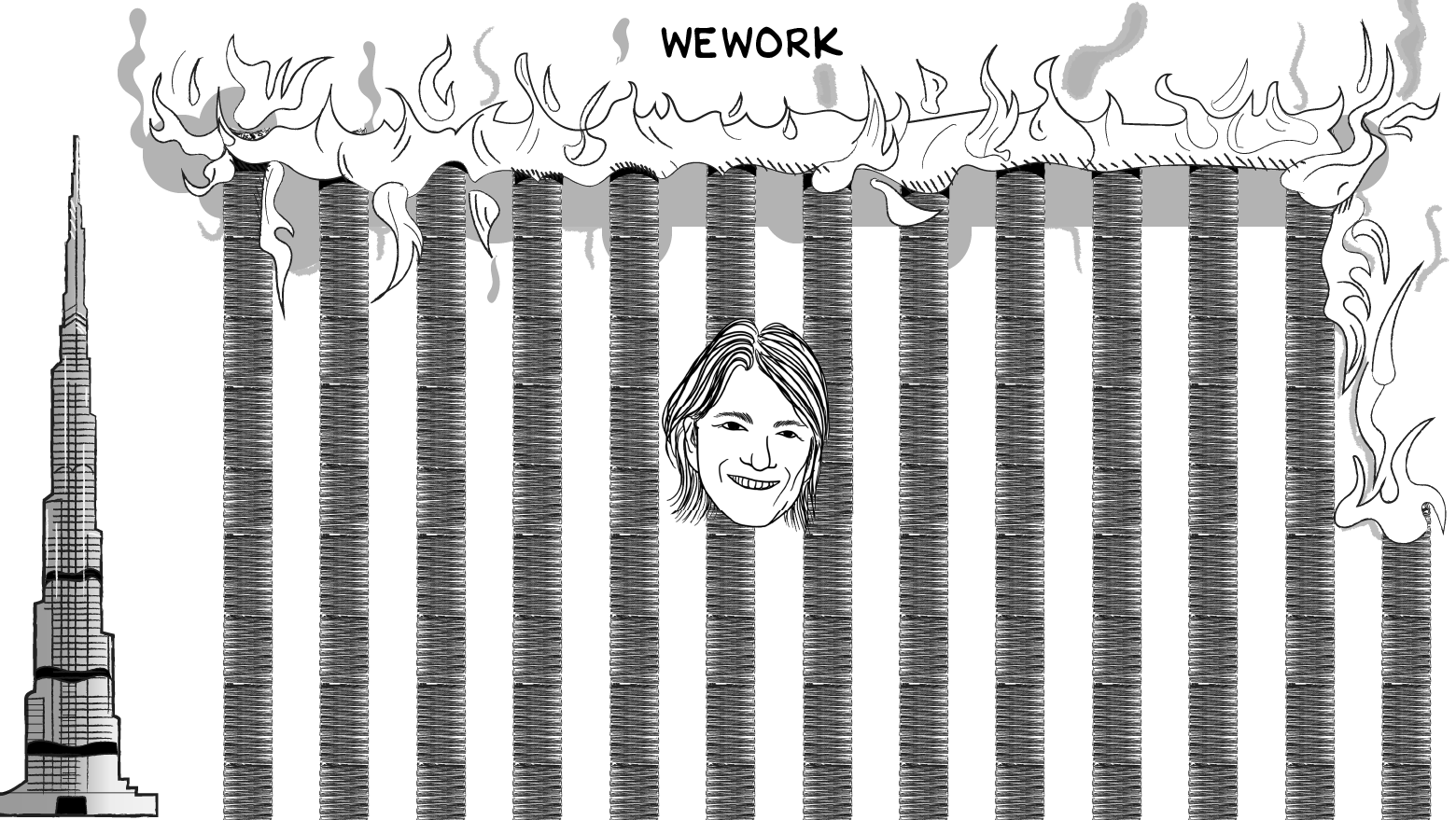

Adam Neumann founded WeWork in 2010, but he didn’t start burning Benjamins at epic scale until SoftBank began shoveling billions into the WeWork furnace in August 2017. By the time Neumann was fired in September 2019, SoftBank had invested $10.3 billion; a few months later it wrote off $9.2 billion of that. That’s a $13.1 million DBB on SoftBank’s money alone, or like flying a decade-old Gulfstream G450 (I browse planes at night — pathetic) into a mountain … every day. Impressive, but only half the story. Neumann’s compensation for this value destruction was complicated by his ouster and a subsequent lawsuit, but we estimate he made off with around $1.02 billion, most of it coming out of SoftBank’s deep pockets. That’s $1.5 million per day during those two years: an EBR of 11.1%.

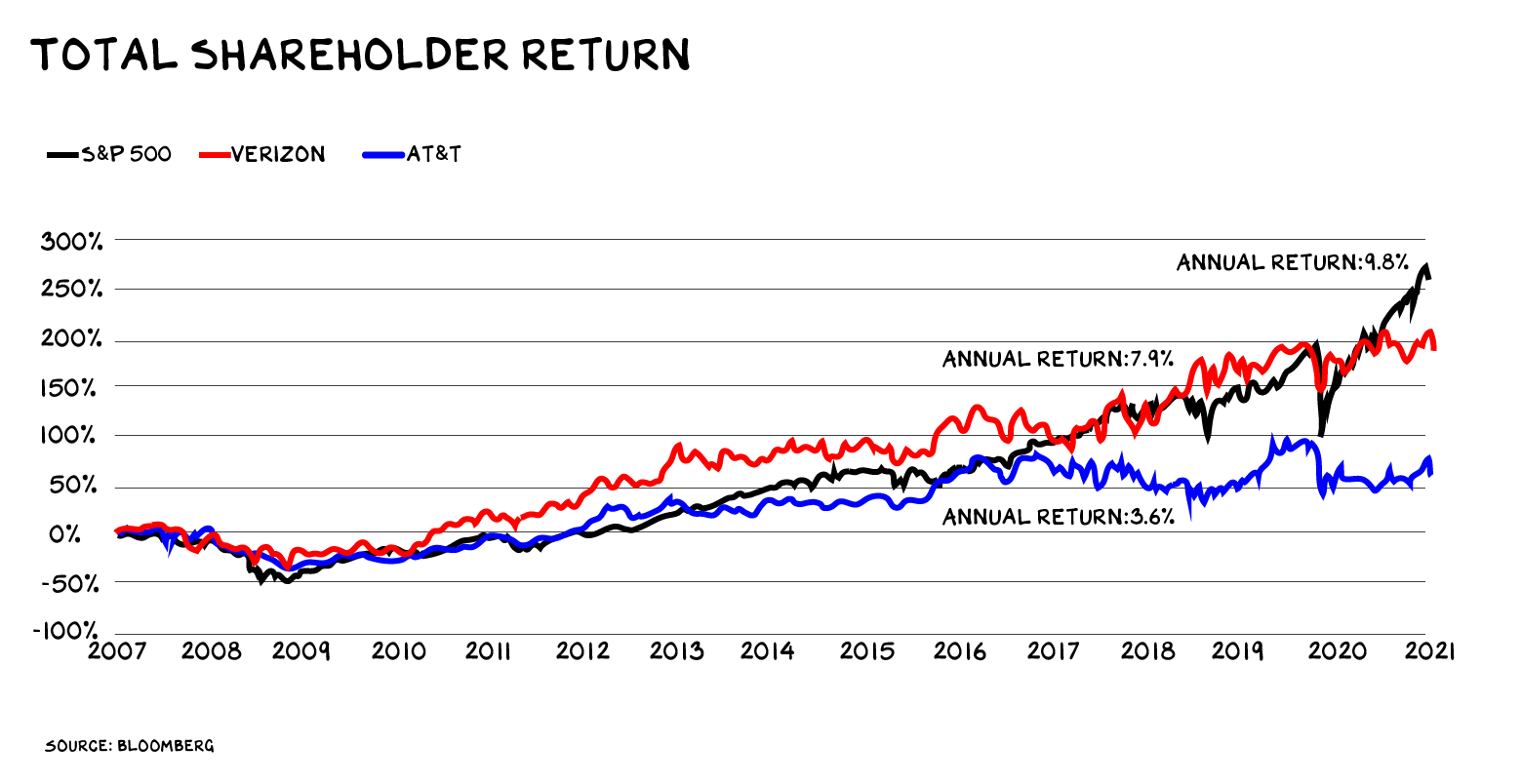

Joining Mayer and Neumann on the podium is Randall Stephenson, who ran AT&T from 2007 to 2020, when his chief lieutenant, John Stankey, took over. If you owned AT&T stock in 2007, you’ve collected $26 per share in dividends since, but you’ve also watched the share price drop from $39 to $29, for an aggregate annual return of 2.5%. This was a period when S&P 500 companies as a whole returned 9.8% a year — much of it on the back of AT&T’s own mobile and data networks — and AT&T’s competitor Verizon returned 7.9% to its shareholders. How did Stephenson manage this? Among other mistakes, AT&T spent $67 billion to buy DirecTV (a pending massive write-off), blew $4 billion when it failed to acquire T-Mobile, and spent another $108 billion to buy WarnerMedia, which Stankey just sold to Discovery. To his (partial) credit, Stankey may have managed to net out the Warner deal as a wash.

So while Stephenson didn’t destroy capital outright, he was a poor steward. Had AT&T eked out even a 4% return from 2007 to today, it would have made an additional $50 billion for shareholders. That’s an implied DBB of $10 million. How did the Board respond to Stephenson’s 13-year-long sideways run at the iconic firm? His total comp was at least $250 million, including a $64 million pension as a parting gift. That’s an EBR of “only” 0.5%, but still a huge payout in the face of mediocre performance.

Honorable Mention

In April 2014, toward the end of Steve Ballmer’s controversial run as CEO, Microsoft closed the $7.2 billion purchase of 1999’s leading mobile handset maker, Nokia. Just 15 months later, Ballmer was gone, and the company wrote off $10 billion for the failed acquisition — the deal was so bad it ended up costing Microsoft more than it paid, mostly due to severance for laid-off Nokia employees. That’s an incredible $22.2 million per day, the highest DBB we could find. (Ballmer only made $1.65 million his last year at the company, so a minimal EBR.)

Burning Benjamins doesn’t just happen in the U.S. In 1998, Daimler-Benz acquired Chrysler for $35 billion in the largest industrial merger ever at the time. After nine years of culture clash and billions in losses, Daimler unloaded 80% of Chrysler to a private equity firm for $7.4 billion, valuing the company at $9.25 billion. That equates to an impressive $7.8 million DBB.

How do these corporate money losers compare to the largest and longest-running Ponzi scheme in history? Bernie Madoff ran his fake fund for nearly 30 years, costing investors an estimated $19 billion. The date his fraud began is disputed, but assuming it was 1980, that’s a DBB of just under $2 million per day. A massive, decadelong legal project has repaid most of these losses through fines and settlements, and Madoff died in prison, but only after a multi-decade run paid for by the destruction of thousands of people’s economic security.

MeWork

Growing up, I loved to watch my dad pack for business trips. He smelled of Aqua Velva and draped his Izod sweaters over a Ram Golf bag. He’d iron the mammoth collar of his Pierre Cardin shirts, fold them around a piece of wax paper, and lay them into his Hartmann luggage like newborns. It was ceremonial, just as when he’d wear his kilt. Elegant yet masculine. During one of these pre-business-trip ceremonies, when I was about 8, my mom walked in. I looked at my dad’s stuff and asked, “How come dad is so rich, and we’re so poor?”

My dad loves this story and laughs out loud when he tells it. But it wasn’t funny. He’s been married — and divorced — four times. There was some financial stress, there was incompatibility. But the real fissure was that there were two Americas … under one roof.

Whether we’re executives, parents, or citizens, we need to ask ourselves: Have our interests diverged from those of the people who matter most to us and society? Do our spouses, children, neighbors, employees, and countrymen win and lose in reasonable harmony? Are we part of a family, part of a nation? Or have we become the MeWork generation?

Life is so rich,

P.S. There’s just over one week until registration closes for the Innovation Strategy Sprint with my former professor, Dr. Sara Beckman. The Section4 team put a short video together with more information about the Sprint format and content. Check it out and register.

43 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

Absolutely a fan of your madness scot! 😊

There was a good point in here about linking incentive comp with solid management, but the overgeneralization of “burn” = bad undermines your credibility: “In an efficient and fair (dangerous word) market, the EBR ratio would be zero.”

If the EBR was zero, there would be no point to venture capital and all great businesses would be bootstrapped. And yet, we both know that the vast majority of massively successful companies were VC-backed.

It seems too obvious to need stating, but cash burn is good when the non-cash benefit is higher, such as in successful brand-building (Netflix), product innovation (Salesforce in its early years), or customer acquisition for high-retention businesses (Snowflake). Done right, burn becomes earn.

Great article, really enjoy all of your content!

@profgalloway fun read. Was sent to your article by a friend who noted a month prior I’d proffered my own two custom metrics for financial assessment, citing Neumann & Mayer, too (https://geo-snelling.medium.com/big-money-grows-our-languaging-should-too-12e5d772f281) Indeed, as you explain as well, we need better linguistic tools to identify and quantify money firestarters, but what then? Rational actors will risk/burn/risk and seek to avoid consequence. Is your answer to make their record more public, so we (rather, company boards) allow them fewer risk/burn cycles?

Can someone explain the first graphic for me? How is “top 50” defined? More importantly, why does it only show the years 1990 and 2000, but not 2010 or 2020? And why top *50*? The top 100 distribution by market cap looks much more like the 1990 graph (I.e. far more EMEA companies), quite possibly because the nature of EMEA with so many national and cultural barriers means it’s much harder to form huge monopolistic conglomerates…which is a good thing?

Who does the illustration for your articles!

Great analysis – loved it. But so hard to contexualize these massive numbers. How does this burning show up in average Joe’s (my) pocket book? Is it the low minimum wage? Is it price of goods? It has to come from somewhere? Or are they just printing paper and burning it? Baseball is easier — pay a player millions and price of tickets, hot dogs and t-shirts go through the roof and way too many commercials if watching. Is there similar correlation with these guys? Would appreciate your thoughts, keep up the great work!

Most of this is fair but Quibi was more of an example of spectacularly bad timing in a capital-intensive industry. In hindsight – who saw the pandemic coming when they launched a mobile-only service? I worked for Meg at another company, and her track record for creating shareholder value elsewhere – including recovering what others had burned – is stellar.

Sounds like you’ve got some unresolved issues with your dad.

so good.

the two americas may have a lot to do with gender.

thank you.

Well Scott. Maybe ask your self that question. Something about camels and needles comes to mind. And something else about pots and kettles.

I see hundreds of fund managers who are sitting in their jobs (claiming 10,20,30 years experience) despite enmasse underperforming benchmarks. >80% of the Mutual fund and Hedge fund industry doesn’t generate any value. They are only enriching themselves. Which is why they always keep those cushy jobs as being less competent or frankly incompetent is more welcome. Speaking of diversity most of the women and men who are benefiting by playing this card are the same people who are already in the privileged system and giving themselves promotions and fatter paychecks.

And yet, Marissa still sits on the Walmart board of directors. I do wonder what she adds to the mix there?

The noise around Marissa had little to do with her ability or experience. It was a big event for the left and the feminists who had ‘one of their own’ running a major tech company. She graced dozens of magazine covers, including women fashion pubs. If you want an image instead competence, highly likely you will get a bad CEO.

I wouldn’t say “the left” rather it was liberals. The real left considers the ID-pol nature of a ‘Female CEO’ (etc.) being a good thing as a liberal distraction from the class struggle.

Ah, the right wing is always good for a bit of misogyny. While Mayer didn’t have a good run at Yahoo, prior to Yahoo she designed something called “the Google homepage,” which to this day continues to be one of the biggest consistent moneymakers on planet Earth.

If we want to talk about a true serial failure, let’s address the right wing’s hero Donald Trump. Countless business failures and business bankruptcies, endless defaults, and a disastrous single-term presidency… yet the alt-right continues to insist that he is some sort of success story. The lack of self-awareness by both Trump and the lunatic right on this point is profound.

The most equitable economic bloc is the one drowning, unable to support the world’s worst off, and no longer leading the advances we need to manage climate damage, control diseases or feed the world. We can and must do better at protecting our most vulnerable and nurturing all who have both talent and desire, but we should be careful to avoid failing prescriptions.

Scott, i think you are focusing on the right thing. Burners vs Earners. I believe we have to go back to the old school of celebrating the earners. The ones who contribute to society. The ones who promote equity and fairness in their pay and honour the true heroes, the employees who make it happen. It’s an old concept – care. Care for the community, care for employees, care for the environment. Just care more and take less.

Success in 🇺🇸 has always been based on MeWork. Your success is based on a system that doesn’t provide the social net other G7 countries do. The tens of millions that are in poverty, that are uneducated that are unemployed and untrained suffer while the corporate or the 1% do not have to pay the cost of support. 🇨🇦 May have higher tax rates but everyone has health care, pain maternity leave , free / affordable education etc.

I wouldn’t tout Canada as some sort of paradise — its health system has failed miserably in vaccinating citizens, it has some of the world’s highest living costs, and it was the first G7 to normalize white supremacist politics (in the form of the Parti Quebecois demand for a white ethnic nationalist “pur laine” state).

“European innovation that has drowned in the rising red tide. But that’s another post”. Can you write it ?

This commentary is one of the best (honest too including his own ) – if any one earning at tail end of the distribution of earnings should realize it is chance/luck – so extreme low earning (min wage $7.25/hr) or 300 times the average worker salary are not justifiable scientifically

Hello Professor Galloway – My last day job had me as a partner in the San Francisco office of a retained executive search firm. I have followed and really enjoyed your assessments of executives. In today’s email you forgot to analyze the spectacular disaster of a certain billionaire real estate executive who recently left a high-level position in the public sector. I look forward to your future take of that most remarkable executive person. Jeff Adams @jcadams Berkeley CA.

Absolutley brilliant!

Agree!

Scott, this news letter is phenomenal, I am 44 year old business man & Entrepreneur and I love your content and narrative, so fucking real. See you soon on the strategy sprint!

The DBB on the 3 collapsed Icelandic banks was something north of $99 million: $182 billion in balance sheets racked up and run to the ground in under 5 years. Easily beating Ballmer, Madoff, and every other fantastic example you give, Prof. Galloway. (Great metric, btw!) http://www.icelandssecret.com

… and all this in a country with fewer people than in your Manhattan neighborhood: 320,000.

… that’s a brand new 737 MAX 7 per day.

This commentary is another great expose of the hypocrisy of American Capitalism. Capitalists such as the ones you describe are vocal about the meritoriousness of their efforts on the way up but try to fix the game by the use of lobbyists and favorable legislation paid for by campaign contributions and circles of influence they organize once they get to the top of the pile. As this article states, they also manage, in most cases, to assure that it is not they who suffer the most from the failure of their exploits, a problem that can be fixed to some degree by limiting TAX DEDUCTIBLE executive compensation, thus shifting losses to the investors, who might then think more about how they invest since more of the lost money comes out of their personal pockets. There are a host of “fixes” available to ensure that the form of “managed capitalism” we practice is managed in such a way as to make those who scream the loudest about how the investor class should be treated under the law responsible for the societal impact they have. While many of those calculations are debatable, anything that puts the burden of the negative consequences on those who lead the pack and benefit the most will likely minimize, to some degree, the depth and scope of those failures on the rest of the public who are not the Masters of the Universe. Honest failure is no shame so long as those who bear the brunt of those failures understand at the get-go the consequences of their gamble. In most cases, it is the least fortunate among us who are fleeced in the process.

No doubt the Comments will be primarily aimed at errant CEOs and their compensation. “Someone has to do something!’. How many will mention the people who throw a baseball for $20M a year? Or rush Quarterbacks for the same? How about the average NBA player salary plus fees for convincing inner city poor that they cannot be cool without the $200 sports shoes they happen to endorse? All the above can justify their salaries/stock/fees by turning around a company, adding significant shareholder value, or winning a Superbowl. Otherwise, they are just overpaid and underperforming. But, only the CEOs are bad guys. Will the Commentors see the forest or just the selected trees that reinforce their opinions?

Pro athletes are really employees of the teams owned by the billionaires. Their careers are all too often short can end at any time. You’re also only referring to the less than 1 percent of athletes who are able to cash in for the big bucks.

One other thing – NFL contracts are NOT guaranteed.

Just sayin’

CEOs are really also employees of the companies, owned by billionaire hedge funds/mutual funds. And, their tenure can be limited. Average tenure of a biotech CEO is about 18 months. And, CEO contracts can be overridden by a #metoo event, real or made up. Left has perfected the Kavanaugh attack in the media.

As a first time entrepreneur bootstrapping my business this is just mindblowing. I don’t think I could ever pull this off – but also actually didn’t want to.

Just watched the wework documentary for the 2nd time today and it had me thinking.. How can these high flying execs and ceos engage in value destruction instead of creation and still walk away with participating trophies in the form of insane severance packages.

Don’t forget what Elop did to Nokia. Appalling!

One of your more remarkable and insightful posts Professor Galloway!

A-greed! Defenestrate all the ESG categories and instead vote for limiting CEO-to-worker compensation ratio. Including benefits etc.

Limit CEO compensation? While we are at it, limit NBA compensation to a ratio of the beer sellers salary. Rappers cannot make more than a ratio to the guy who cleans the studio. Actors to the pay of the set caterers. See how well that would go over.

I think the point is, CEOs that FAIL abysmally, costing shareholders/investors 100s of millions or billions should not walk away with 8 or 9 figure parting gifts. Pro athletes generally have to perform to continue to reap their millions.

Long list of athletes who had big contracts and didn’t deliver. Ask Red Sox about Pablo Sandavol. Blame Board of Directors, not the CEOs who were good negotiators or bs’ers

The performers either generate wins or revenues. Even if the CEO’s perform poorly they walk away with obscene exit packages. Now that index managers like Vanguard are actively voting let them explain excessive compensation.

Just curious about Jeff at GE.

https://www.pornhub.com/view_video.php?viewkey=ph5cf166995f388