Four Retail IPOs

Person of the Year

I make predictions, which is a shitty business. If they come true, circumstances leading up to the event make the prediction seem less bold. If they don’t, the Twitter troll army comes for you. On a risk-adjusted basis, bad idea.

Like that’s going to stop me.

Time’s 2021 Person of the Year, and likely recipient of the Nobel Peace Prize, will be Frances Haugen. Lawmakers, academics, journalists, philosophers, and Borat have all railed against the global menace that is Facebook. And for good reason. The KGB, CCP, and Iranian Ministry of Intelligence could not have dreamt of a more perfect weapon. An ordinance that spread death, disease, and disability across the U.S. via an unnatural increase in vaccine hesitancy, catalyzed an insurrection at the Capitol by people fed a steady diet of misinformation, and contributed to a decline in the mental health of America’s youth. And … we financed it.

Many sounded the alarm. But all we’ve done is put on a masterclass re the difference between being right and being effective. Ms. Haugen’s rollout (multichannel, branded, coordinated) is the first time it feels as if we’re fighting Panzer tanks with tanks, vs. on horseback.

But that’s not what this post is about. Let’s sit back and watch Breaking Bad season 9, starring Ms. Haugen, and stay out of the way.

What to talk about? I know: Dresses. Specifically Rent the Runway and some other recent retail IPOs.

Last week we filmed the pilot for our upcoming show on CNN+. I arrived, no joke, in the above outfit and nobody at CNN said a thing. I have found my people. The ensemble is the outline for this post — Warby Parker, Rent the Runway, Allbirds, and the Swiss shoe company On. Note: Search your emotions. After absorbing the above pic, you are disturbed … but compelled. Anyway, why do I dress in drag? A: Because it makes me happy.

Shade

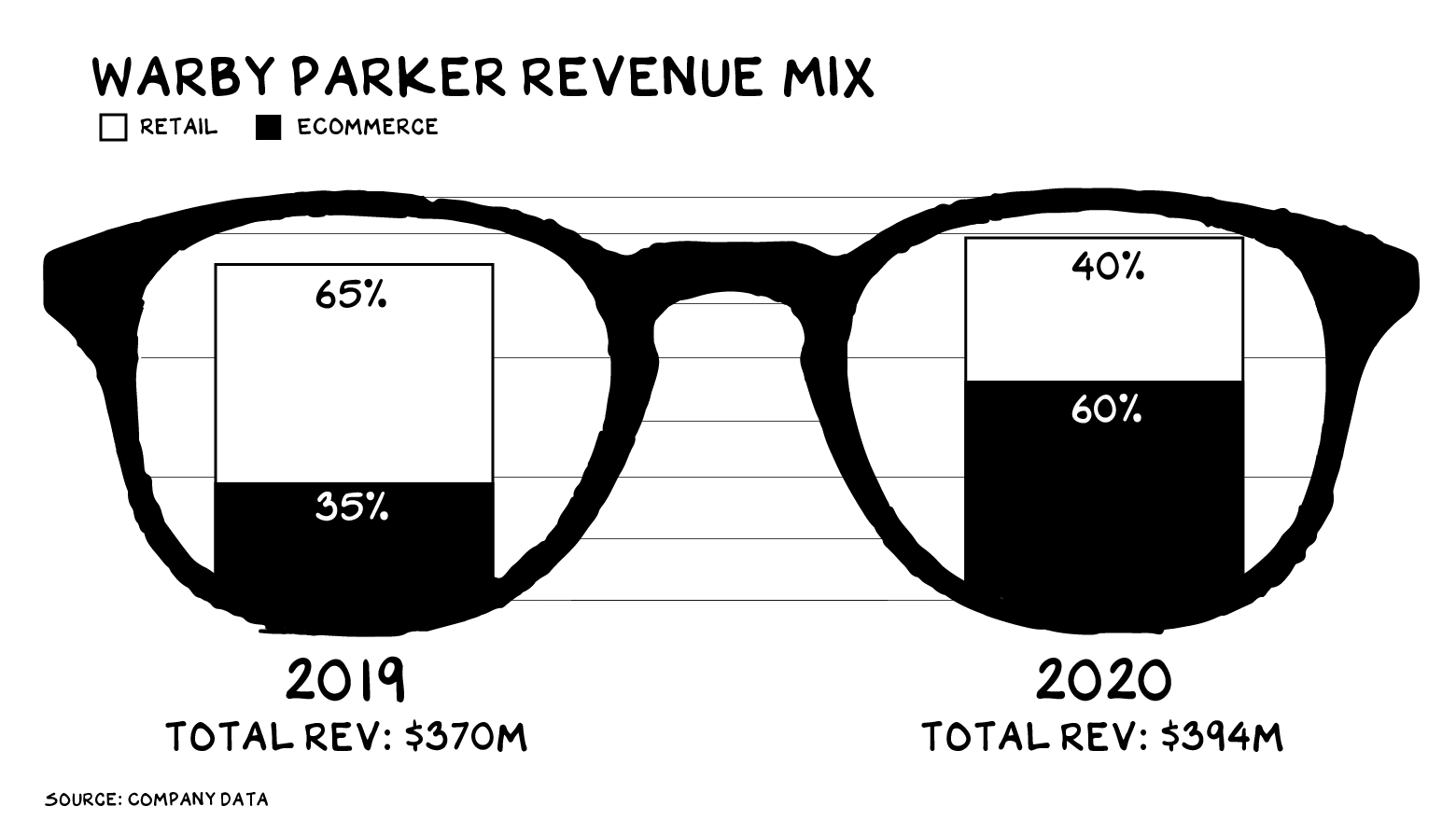

There’s a reason Warby Parker’s direct listing was well received last month. Numbers. By every metric, this is a strong business. The glasses retailer has a Net Promoter Score of 83, 2 million+ active customers, and a gross margin of 60%. In 2020, Warby’s customer acquisition cost was $40 on an average order of $184 … and 42% of the firm’s customers made a repeat purchase. In addition, when the pandemic throttled its physical retail channel, Warby expanded its e-commerce business — the company started online, enabling consumers to try on glasses at home and return the ones they don’t want.

The challenge — and opportunity — for Warby is the industry is concentrated. Luxottica, the Milan-based eyewear heavyweight, has been eating anything in its path. (Think: Ray-Ban, Oakley, Oliver Peoples, Persol, Ilori, and Sunglass Hut.) In 2018, Luxottica registered three-quarters of glasses sales in North America. But the Monster of Milan suffered a 17% sales drop and a 90% decline in profit due to the pandemic. Warby is a digital native, with direct consumer relationships, which has yielded an enduring advantage. Disruption is less a function of the innovator’s skill than of how fat, happy, and lazy the incumbent is. Warby is positioned to disrupt, as Luxottica is the mother of all unearned margins. There are few businesses as big, or as dependent on brand equity, or that have worse distribution. Think about where you buy sunglasses. The only worse retail experience is a gas station. BTW, Tesla is a great car, but people miss the real consumer benefit: exiting the gas station ecosystem, where it feels as if you could pick up a rare form of cancer or get shot.

My Shoes

Two high-end sneaker companies are venturing into the public markets: On, which had a banner IPO in September, and Allbirds, which filed for an IPO in August. Both have similar strengths and face similar challenges, but On is the (much) better bet.

There’s not a lot to distinguish between the companies on paper. Allbirds has a stronger NPS score of 86, vs. On’s 66. But On’s 59% gross margin tops Allbirds’ 51%. On is growing faster: From 2019 to 2020 its net sales grew 59%. Allbirds registered 13% growth.

That slowing growth is troubling, and it might be why Allbirds scores high on another measure: Yogababble. (Shiv’s favorite business cat term, natch.) Allbirds’ original prospectus was filed as an SPO — a “Sustainable” Public Equity Offering. This wasn’t your standard IPO, the company claimed. “Historically, businesses have primarily focused on maximizing stockholder value,” but a sustainability framework meant Allbirds was an “exception to the rule.” Until it wasn’t: The company later amended its prospectus to include no mention of an SPO. Allbirds (and its lawyers) likely realized you go public on Wall Street, not Woke Street. Folks, you make shoes.

And there’s a hint of the squishy metrics — reminiscent of WeWork — that have become rife in the SPAC market. As Professor Daniel McCarthy highlighted in the Prof G Pod, Allbirds reports “contribution profit,” which is gross profit less any variable costs associated with selling the product. This is a useful metric, especially for a company projecting strong growth, as it accounts for costs that are harder to minimize through scale. But the only thing Allbirds deducts from its gross profit to determine contribution profit is credit card processing fees. Something they don’t deduct is store operating costs — but stores don’t scale like software. To sell more shoes through stores, you need to operate more stores. Warby, by contrast, does deduct store opex when it reports its contribution profit. On doesn’t highlight contribution profit at all. This doesn’t make a huge difference — only 11% of Allbirds’ sales came through its 27 retail stores in 2020 — but it’s a red flag that speaks to a management team that’s reaching.

Like Warby, both shoe companies are entering a concentrated market, in this case, a 60%-player, Nike, and a strong No. 2, Adidas. But unlike Warby, neither built an innovative model to disrupt the incumbents. They’re relying on brand strength and product innovation. Good luck.

The companies diverge on branding. Both got off the ground with word-of-mouth, community-driven marketing, but Allbirds has transitioned to what it calls “full-funnel” marketing. That’s Latin for “we raised a ton of cash, and we’re now pouring it into television and print.” In the first six months of 2021, Allbirds spent 22% of its revenue on marketing. On spent 13%, and its S-1 makes clear they’re sticking with their strategy.

Our view: Allbirds’ organic growth is sputtering, and management is buying transitory growth to support the stock price … until management can sell. The era of premium margins for mediocre products with Don-Draper-like TV budgets is over. Design, merchandising, distribution, and supply matter more. Brands still matter, but branding is a new ballgame. On’s voice holds together better.

Red Dress

There’s a lot to love about Rent the Runway. It was co-founded by two impressive women, and the concept is powerful. One problem: It’s a shitty business …

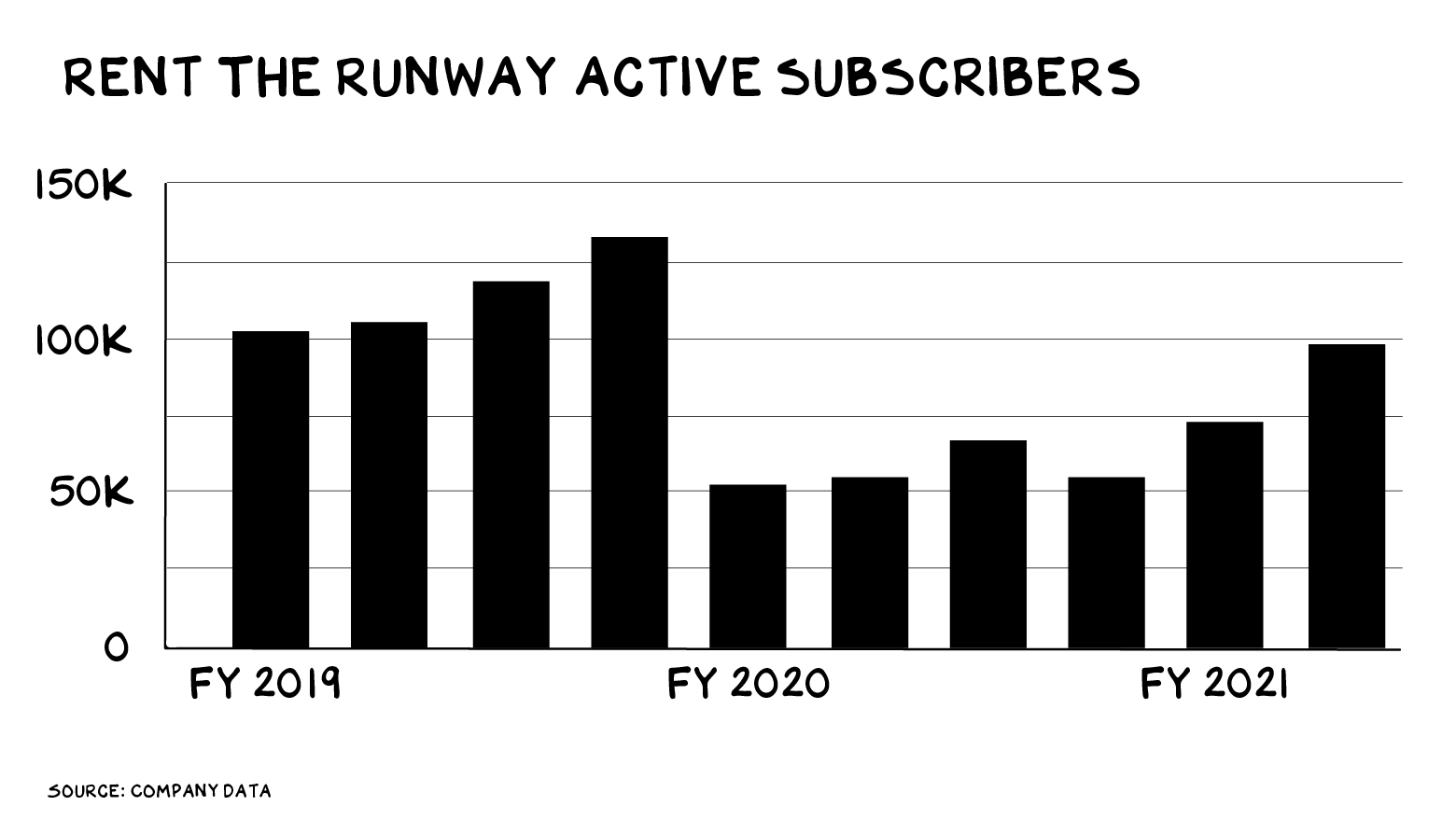

Rent the Runway’s active subscriber base was cut in half last year. As lockdowns have eased, it’s begun climbing back, but it still has substantial ground to cover to return to where the firm was two years ago.

The company glossed over this in its financial summary by emphasizing the number of “total subscribers,” but a footnote revealed that this number includes those who have “paused” their account. In other words, half the “total subscriber” base isn’t paying.

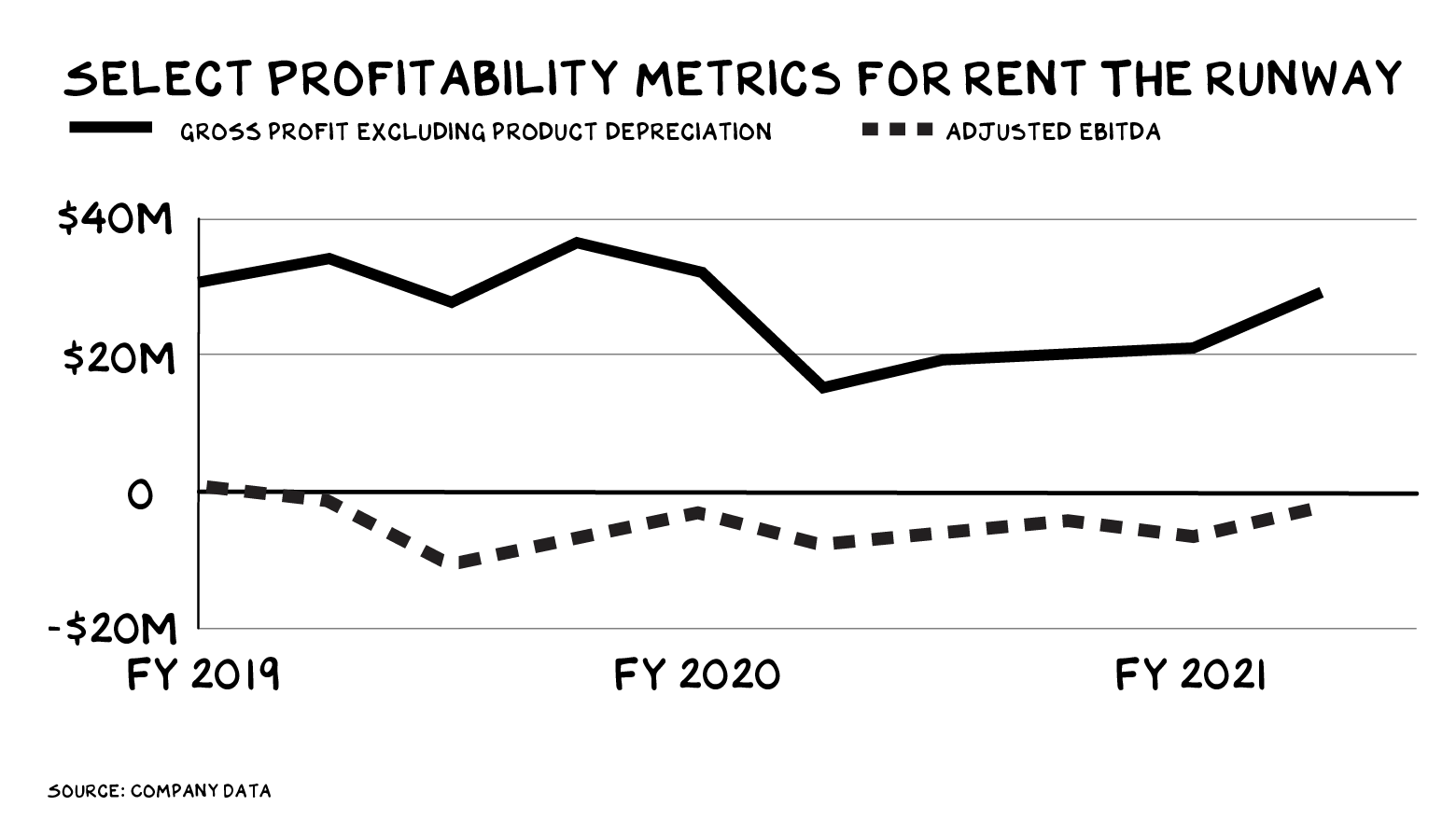

If “total subscribers” is the company’s concealer, RtR’s profitability metrics are its botox. First, it creatively adjusted its EBITDA, though even with those “adjustments,” RtR’s earnings are negative. Next, the company broke new ground in creative accounting. Companies including WeWork and Aspiration have concocted variations on EBITDA to smear lipstick on bad numbers. RtR has moved this tactic up the income statement to the gross profit line, reporting “gross profit excluding product depreciation.” That means they’re removing their primary cost of goods sold — the cost of the clothes they rent — from their, well, cost of goods sold. These are delicate goods subject to the vagaries of fashion, not factory equipment. In a section of the S-1 titled “Key Business and Financial Metrics,” this novel measure improved RtR’s gross margin from 27% to 51%. Those are healthy retail gross margins — except that another 24% of real economic cost is lurking down the income statement, plunging EBITDA to negative territory.

The company also boasts (in an enormous font) that 88% of its customers are acquired organically. Impressive if true, but this is difficult to believe, as its customer acquisition cost is $55. Consider the math: If 88% of your customers are acquired for $0 but your overall CAC is $55, then you’re spending $458 for every customer acquired through paid channels. Something’s off.

But the real tell is the company’s private financing history. Last fall, RtR struggled to raise $125 million of debt and equity at a $750 million valuation. That was a downgrade from 2019, when it achieved unicorn status. But 2021 is going down as the greatest bull market for private companies in history. There’s an ocean of capital pouring into late-stage venture companies right now, and if RtR was anything other than a solid manifestation of greater fool theory, the firm’s existing investors would have stuffed another $200 million to $300 million into it. (Warby and Allbirds both announced monster private rounds in 2020.) RtR’s IPO is the last helicopter off the roof of the American embassy in Saigon. Investors left behind are going to experience a hostile market.

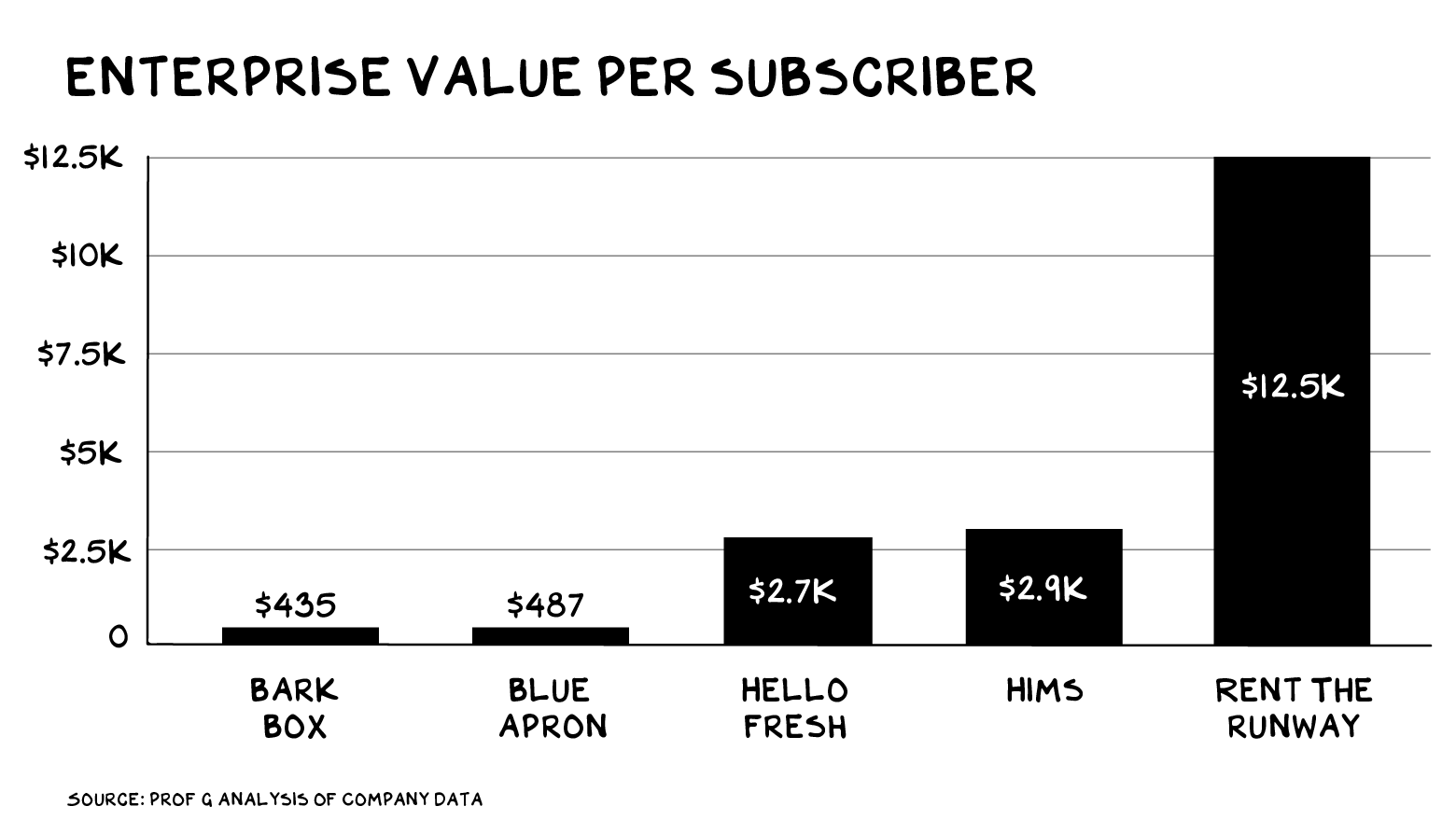

RENT jumped 17% in its first two hours of trading, but the shares soon began a downward march that won’t end until the equity reaches single digits. Between Wednesday’s peak and close of business Thursday, the equity was down more than 20%. It’s still overvalued. Thursday’s close pegs the company at roughly $1.2 billion. But RtR has less than 100,000 active subscribers, so this valuation implies each subscriber is “worth” more than $12,000. That’s an order of magnitude more than the market values subs at comparable businesses. (Even if you include “paused” subscribers, it more than doubles anyone else.)

Rent the Runway’s business model distills to this: Deliver $200 worth of service but charge $100. It’s a great service (and an inevitable downward slide should make RtR an acquisition target for Amazon, Shopify, or another player), but it doesn’t add up to a viable standalone business — the firm incurs losses matching its revenue. In sum: Don’t rent the runway. Sell it.

Regression to the Mean

Fall is the best time of year, except in Florida, of course. Dry, crisp, light, and there’s a breeze that delivers a bite of winter. A season saying in hushed tones … I’m coming. But it feels as if a bomb cyclone may also be near. Metaverses … Shiba Inu coins … and a Trump SPAC worth billions. We’ll see.

Consumer IPOs, a 56-year-old in drag, and Frances Haugen. Something meaningful, something joyous, and someone profound, respectively.

Life is so rich,

P.S. My final Brand Strategy Sprint of the year is open for registration. 94% of previous students said the course positively affected their career growth. Join us.

This is an amazing article…funny and enjoyable to read. I can completely relate. I believe that relationships and experiences are what life is all about… and businesses that can do that well will survive and maybe thrive during a pandemic. When times are difficult and people are troubled…those relationships get stronger. The Tesla factory is cool… but cold at the same time.

How do you create the charts? I like the design.

I wish I could unsee you in the red dress.

Awesome writeup. I love these ones… straight facts no politics.

I guarantee attribution would show that Rent The Runway organic number is way off due to overlap. You’re dead on Scott.

Did you rent that red dress?! I agree with the RtRW analysis . ..another consideration- who wants to wear used clothing in the middle of a global pandemic?

If 88% of your customers are acquired for $0 but your overall CAC is $55, then you’re spending $458 for every customer acquired through paid channels.

Could you please let me know the equation and how you arrived at this? As you can tell, am bad at Math. Thanks in advance.

$55/12% (0.12) = $458

The liberal elite are very disconnected from the American mainstream. China, Russia, and Iran have absolutely nothing to do with populism, Fascism, vaccine hesitancy, conspiracy theories, or anything else. These are threads that have run through the United States since the founding, built on gullibility, poor education, and being badly served by elite institutions. Facebook had nothing to do with theism, the Satanic Panic, McCarthyism, Red Scares, Great Awakenings, Know-Nothings, or the Salem Witch Trails. Superstition, racism, and reactionary peasants are endemic to American culture and history.

Hi Scott, I don’t always agree with what you write but it is always food for thought , so keep it up 👍🏻 However, you are fully right to vaccinations against Covid ✌🏻❤️

All the best

John

Hmmm, I’m thinking the Allbirds are the best accessory to the red dress. I don’t know, maybe I’m just partial to the red, white, and blue!

I listen to Pivot podcasts on Sunday mornings (sorry, but I have to be tethered these days) and love them. Just got on board here, and what a shock. Red is always a bold choice, and a clear warning. I won’t be offering much, in that I’m trying to learn. I will say that Zenni’s race to the bottom on prices makes sense for the consumer who probably has to change prescriptions annually. Quality….feh. Since when is disposable an issue for America? Finally, being old, I have the memory of watching my forebears by their specs in Woolworth’s right off the display. Thanks for your insights.

Refreshing. Makes life more buoyant to read business news that is not boring. Also so insightful – seemingly. Red dress – good for you – good for CNN.

I’m not convinced Warby Parker is doing as well as you say. In 2019 they had a net operating profit after tax of $3 million, on $370 milli9n of revenue. In 2020, they had a net operating profit of NEGATIVE $40 million, on $394 million of revenue. So they spent an extra $43 million to get only $24 million in additional profit? And this is even with the additional gross margin they should be getting by the shift of sales from retail to e-commerce? It sounds like they are throwing money at online marketing to gain e-commerce customers, but as I can tell you as a co-founder of a small e-commerce brand, online market isn’t as cheap and easy as some people make out…

I wonder how much Warby Parker’s rapid expansion plans played a part in the loses in 2020. The company opened 30 stores in 2019, is on track for 35 in 2021. One can assume they were planning around 30 last year. Build outs and rent/utilities in the expensive retail areas where they operate must account for a decent portion of that loss in addition to COVID.

Would love to hear your thoughts on Zenni, as they seem to be handing WP their ass on a plate in terms of prices. WP was cheaper than local opticians a decade ago, but now the online glasses market is getting very crowded and Zenni is racing prices to the bottom. For sure, luxxotica’s days are numbered, but I’m not convinced WP is set to inherit all the gold.

To quote from the Beatles’ movie A Hard Days Night: “Take off that wig, Lennon … it suits ya.”

I was convinced the ‘bomb cyclone’ for the market was near. But, not so much now. People have cash stashed away; well people that retail IPOs and Democrats care about anyway, the rich/young. They will go on a buying binge once stores are fully stocked and car lots filled. They will load up on any pro-ESG stock/fund. These trends will go for a while, who knows how long. I am long any stock ESG hates, especially energy. One of the top financial searches is the term ‘stagflation’. That will die down and when people stop worrying about it. Maybe gas lines or a winter of blackouts will start the panic and a return of ‘stagflation’ Google searches. Meanwhile. the market continues up, cash and bonds are trash. Green anything, Crypto anything.

“Think about where you buy sunglasses.” I buy Oakley online. How is this different from buying WP online? News flash, you can also find Ray-Ban on Ray-Ban’s website, on Amazon, and a few dozen other websites. How is this different than buying WP online?

I do wonder if the whistleblower was an overweight, 45 year old man with poor eyesight instead of a young, attractive, smart lady what the response would be. Maybe it would be the same but the other whistle-blowers (Vindman, Snowden etc) sure weren’t treated the same. On another note, I agree with everyone. Scott is the best.

Google “Glen Greenwald Frances Haugen” to figure out who she really is.

Re: the photo – I see that timestamp there. Makes me think edibles were involved!

Eyewear has always been one of the world’s biggest consumer rip off businesses until now. God bless Warby Parker! It’s probably go-to-hell time for all of the chains and little optical mom and pops out there. Remember Diane Von Furstenberg Eyewear? What a joke, but they were laughing all the way to the bank….Times change, life’s so great!

This post was fire Prof G!!!

Warby Parker’s digital try-on thingy is awesome, but their styles are so boring!

@Polly – I agree. Warby lacks the endless aisle of eyeglass style and color combinations. Their quality is better than other online private label eyewear retailers (ex: EyeBuyDirect, Zenni) but they have more variety. They need to work in style drops to get more site visitors and more buyers. Also have a slight stock-out issue that makes it difficult to get many try-ons and to buy some styles at all.

Really love your posts, as well as show. They always provide refreshing insight and are just great fun to read. That said, I could swear on your show you downplayed Warby Parker’s growth opportunities. I’m a fan of the brand, having bought several pairs of glasses from them. But I agreed with you on growth. On the one hand their customer service is stellar. And I got a strong sense that they really value their employees as well as their customers. That makes me root for them. But how much can they grow their relationship with me based on an item that following the first month “new pair of glasses” patina is something I forget about for the next few years. Regardless, keep the great posts coming, and the terrific guests and thoughtful interviews.

Caption: Would you buy a used car from this man?

Real whistleblowers like Edward Snowden and James O’Keefe don’t get the red carpet treatment by media and government. Project Vertias interviewed several big tech whistleblowers who got no MSM attention. Frances Haugen is represented by the usual DC law and PR firms with the goal of giving the government more power over free speech. Given that our AG has branded parents who protest at school board meetings as domestic terrorists, we all know where this is going…

you are 100% correct. Scott can’t see obvious things anymore b/c he has a very partisan brain. she is NOT a “whisteblower” in fact she is talking about things she doesn’t know about or didn’t work on (eg research docs on other products). this is 100% STAGED roll out. see glenn Greenwald’s substack for an actual in depth reporting article

Greenwald is one of the few real journalists left. CNN rots the brain, at least Scott is cashing in on them. The only viewers they have left are stuck at airports. Mind blowing fact – Brian Stelter is only 36.

You mean the parents who have physically threatened/assaulted school administrators for insisting on vaccinations, as has been policy (small pox, polio, rubella etc) for the past 50+ years? You mean those “patriots”?

Although you are pretty cute dressed as a guy, I LOVE that no one said a thing!!!!

https://www.youtube.com/watch?v=ELQvABuxUNM&list=RDELQvABuxUNM&start_radio=1

My God, you’re a badass.