Bank

My north star(s) for philosophy, management, and politics are Star Wars, The Sopranos, and Game of Thrones, respectively. The Iron Bank (GoT) is a metaphor for today’s financial institutions, if present-day banks didn’t need bailouts or to invent fake accounts to juice compensation. Regardless, it was well known throughout Braavos that The Iron Bank will have its due. If you failed to repay, they’d fund your enemies. So today’s Iron Bankers are the venture capitalists funding (any) incumbents’ enemies. If this makes VCs sound interesting/cool, don’t trust your instincts.

Lately, I’ve spent a decent amount of time on the phone with my bank in an attempt to get a home equity line, as I want to load up on Dogecoin. (Note: kidding.) (Note: mostly.) If Opendoor and Zillow can use algorithms and Google Maps to get an offer on my house in 24 hours, why does it take my bank — which underwrote the original mortgage — so much longer?

How ripe a sector is for disruption is a function of several factors. One (relatively) easy proxy is the delta between price increases and inflation, and if the innovation in the sector justifies the delta. Think of the $200 cable bill, or a $5.6 million 60-second Super Bowl spot, as canaries in the ad-supported media coal mine.

Another, easier (and more fun) indicator of ripeness is the eighties test. Put yourself smack dab in the center of the store/product/service, close your eyes, spin around three times, open your eyes, and ask if you’d know within 5 seconds that you were not in 1985. Theaters, grocery stores, gas stations, dry cleaners, university classes, doctor’s offices, and banks still feel as if you could run into Ally Sheedy or The Bangles.

It’s hard to imagine an industry more ripe for disruption than the business of money.

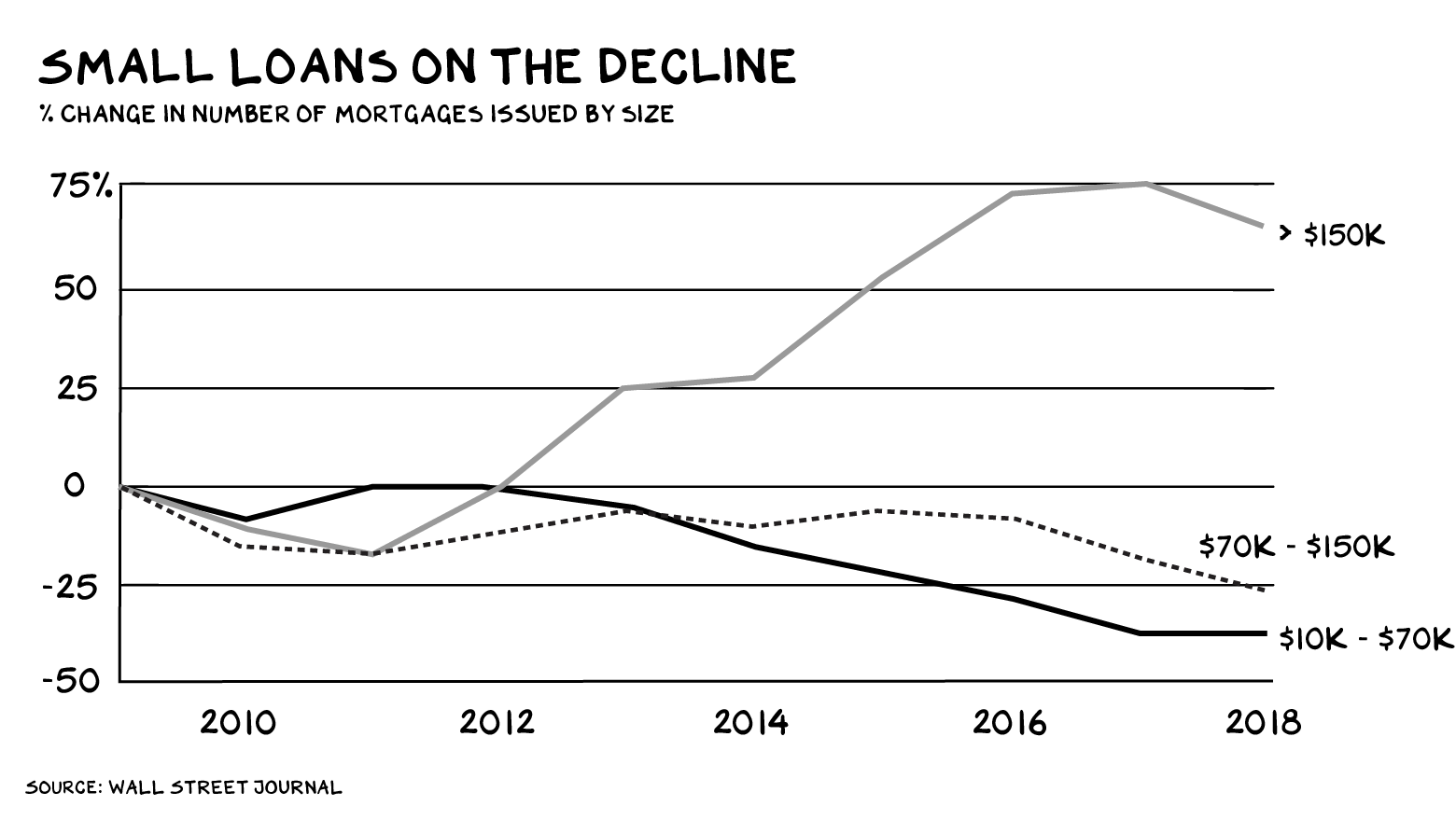

Let’s start with this: Twenty-five percent of U.S. households are either unbanked or underbanked. Half of the nation’s unbanked households say they don’t have enough money to meet the minimum balance requirements. Thirty-four percent say bank fees are too high. And, if you’re trying to get a mortgage, you’d better hope the house isn’t cheap.

Inequity is a breeding ground for disruption, leaving underserved markets for insurgents to seize and launch an attack on incumbents from below. We have good reason to believe that’s happening in banking.

Insurgents

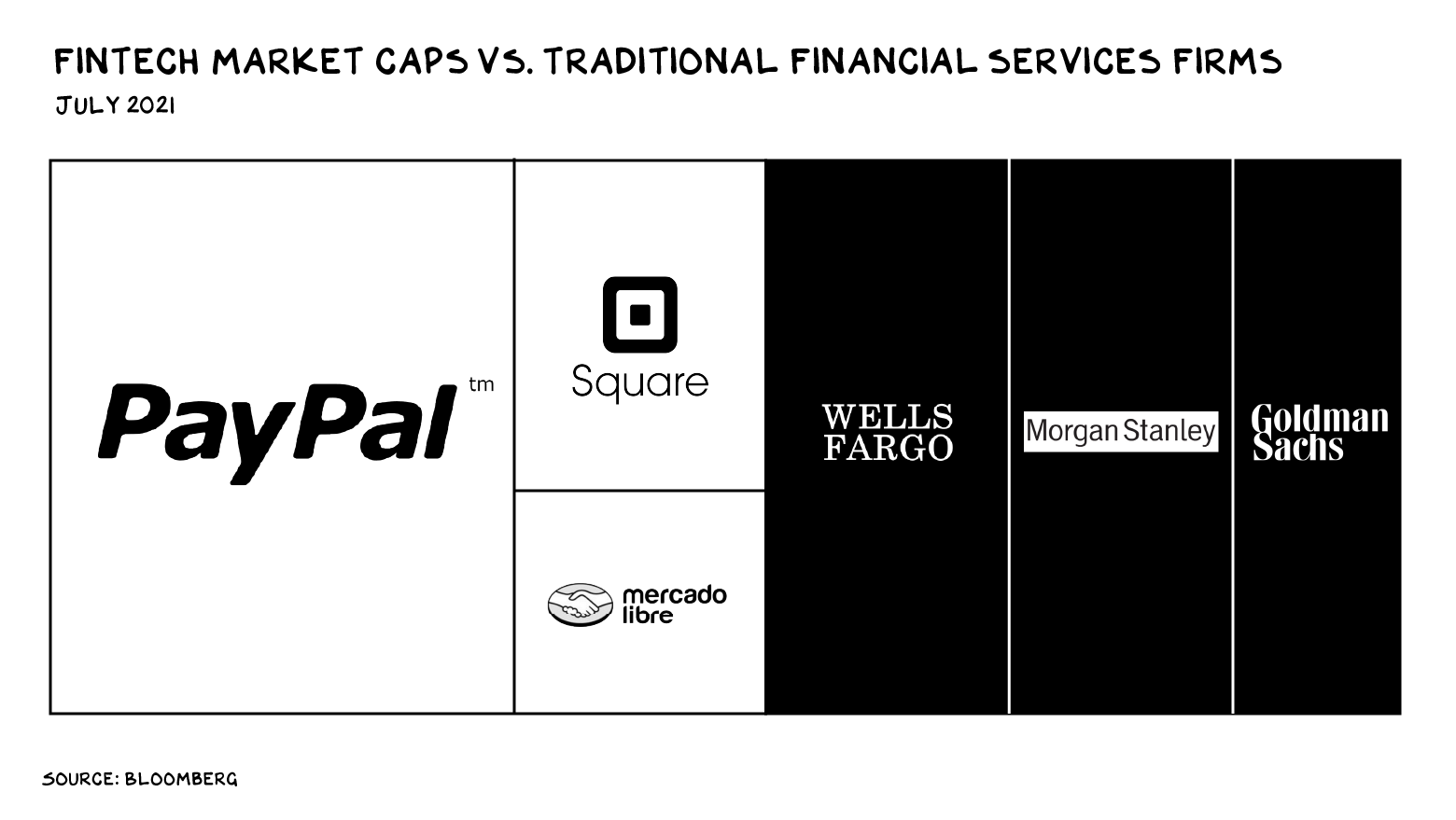

A herd of unicorns is at the stable door, looking to trample Wells Fargo and Chase. Fintech is responsible for roughly one in five (17%) of the world’s unicorns, more than any other sector. In addition, there are already several megalodons worth more than financial institutions that have spent generations building (mis)trust.

How did this happen? The fintechs are zeroing in on everything big banks aren’t.

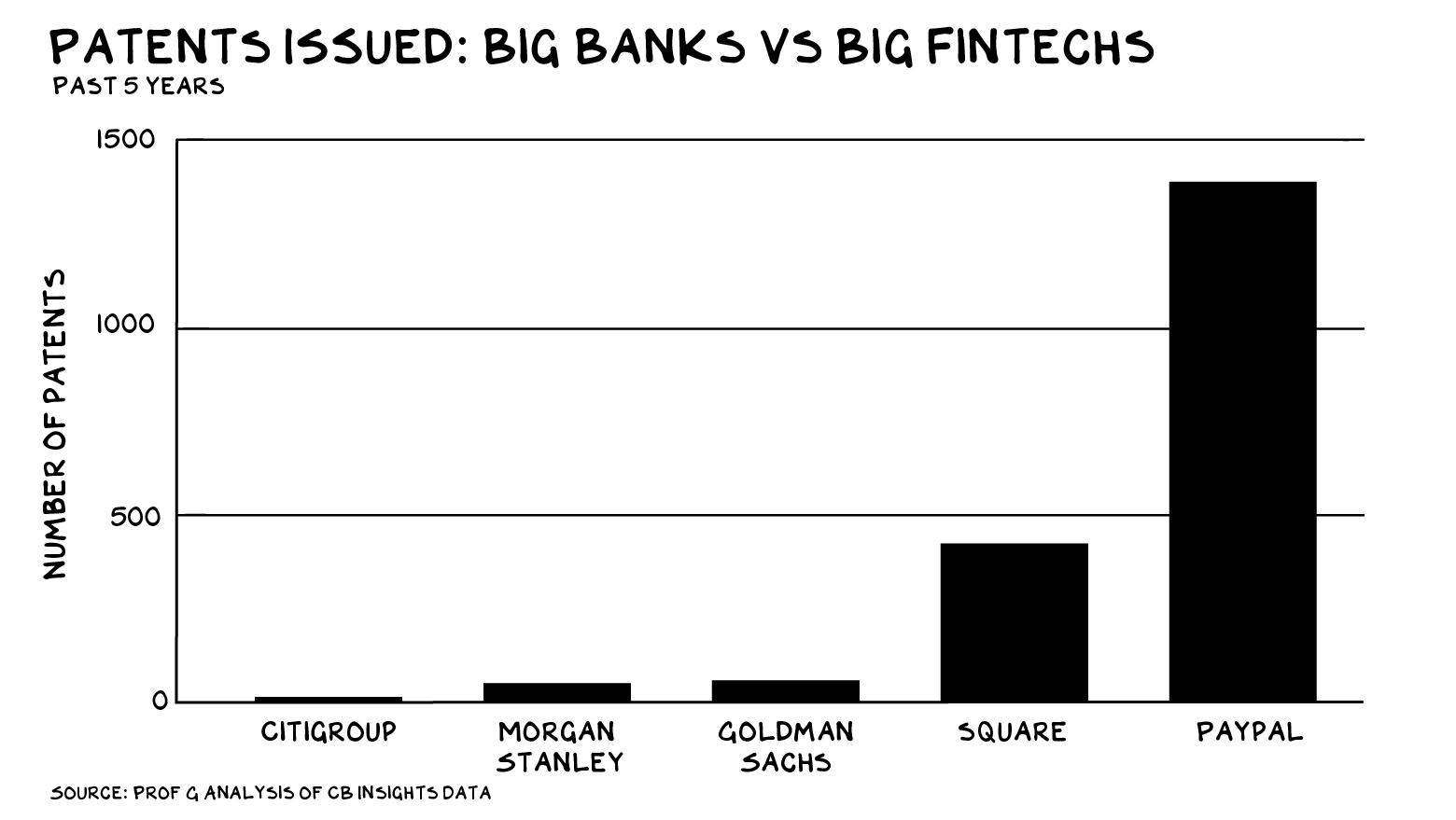

Example #1: Innovation. Over the past five years, PayPal has issued 26x more patents than Goldman Sachs.

Example #2: Cost-cutting. “Neobanks” offer the basic services of a bank, with one less expensive and cumbersome feature: the branch. A traditional bank branch needs $50 million in deposits to generate an adequate return. Yet nearly half (48%) of branches in the U.S. are below that threshold. Neobanks don’t have that problem, and there are now at least 177 of them. Founders frame these offerings as more progressive, less corporate. Dave, a new banking app, offers a Founding Story on its website (illustrated with cartoon bears) about three friends “fed up” with their banking experience, often incurring $38 overdraft fees. Fed up no longer: Dave provides free overdraft protection and has 10 million customers.

Example #3: Less inequity. NYU Professor of Finance Sabrina Howell’s research found fintech lenders gave 18% of PPP loans to Black-owned businesses, while small to medium-sized banks provided just 2%. Among all loans to Black-owned firms, Professor Howell found 54% were from fintech startups. Racial discrimination is the most likely explanation, as lenders faced zero credit risk.

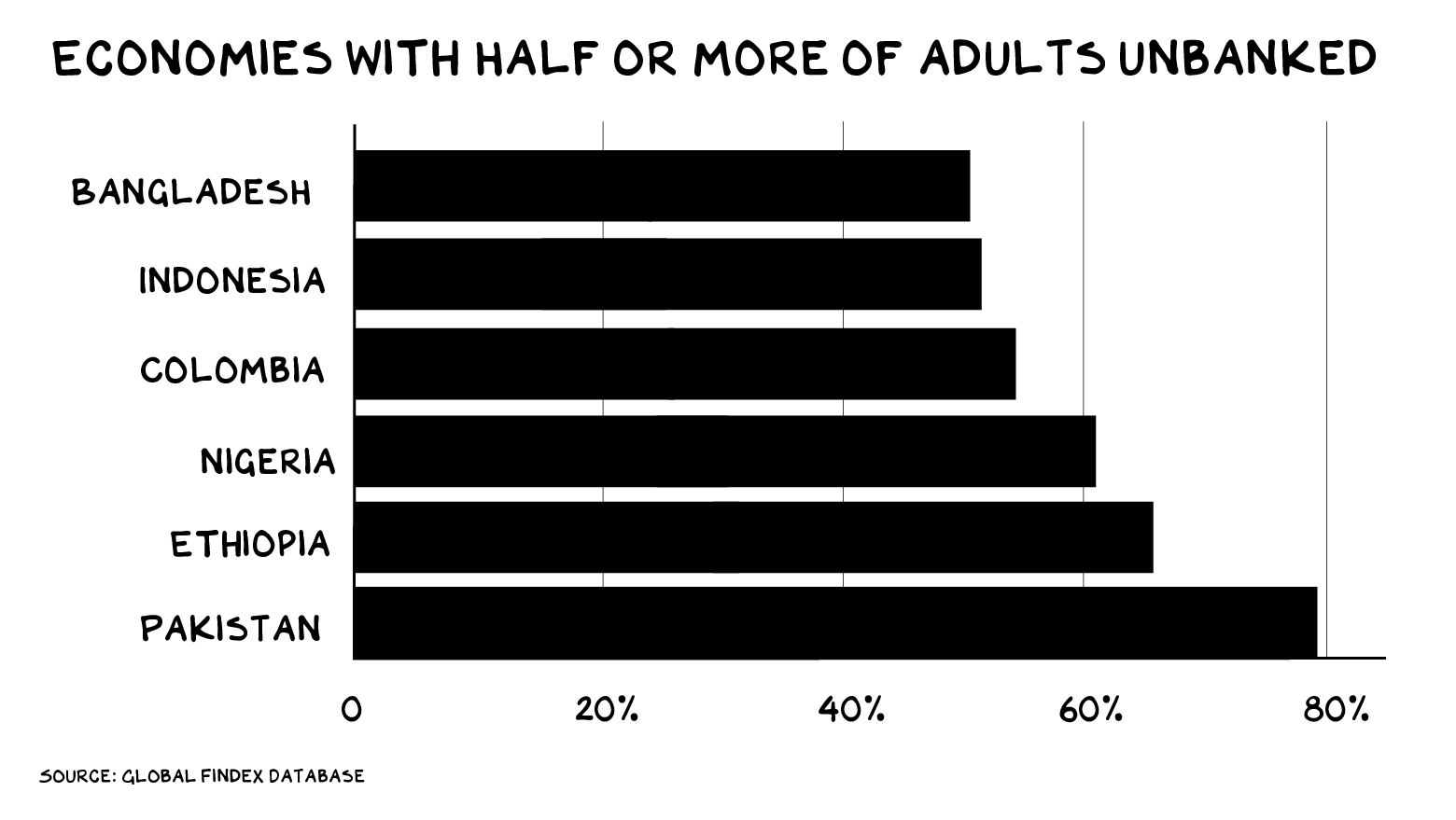

Example #4: Serving the underserved. Unequal access to banking is a global botheration. Almost a third of the world’s adults, 1.7 billion, are unbanked. In Argentina, Colombia, Nigeria, and other countries, more than 50% of adults are unbanked.

But innovation is already on the horizon: Take Argentine fintech Ualá, whose CEO Pierpaolo Barbieri I spoke with on the Pod last week. In just 4 years, more than 3 million people have opened an account with his company — about 9% of the country — and over 25% of 18 to 25-year-olds now have a tarjeta Ualá (online wallet). Ualá recently launched in Mexico, where, as of 2017, only 2.6% of the poorest 40% had a credit card. This is more than an economic issue — it’s a societal issue, as financial inclusion bolsters the middle class and forms a solid base for democracy.

Interest(ed)

Chase savings accounts are offering, no joke, 0.01% interest. Wells Fargo? The same, though if you keep your investment portfolio with Wells, they’ll double that rate to 0.02%. Meanwhile, neobanks including Ally and Chime offer 0.5% — 50 times the competition.

There is also blood in the water for fintech unicorns that have created a debit, vs. credit, generation: The buy-now-pay-later fintech Afterpay has more than 5 million U.S. customers — just two years after launching in the country. As of February, its competitor Affirm has 4.5 million customers.

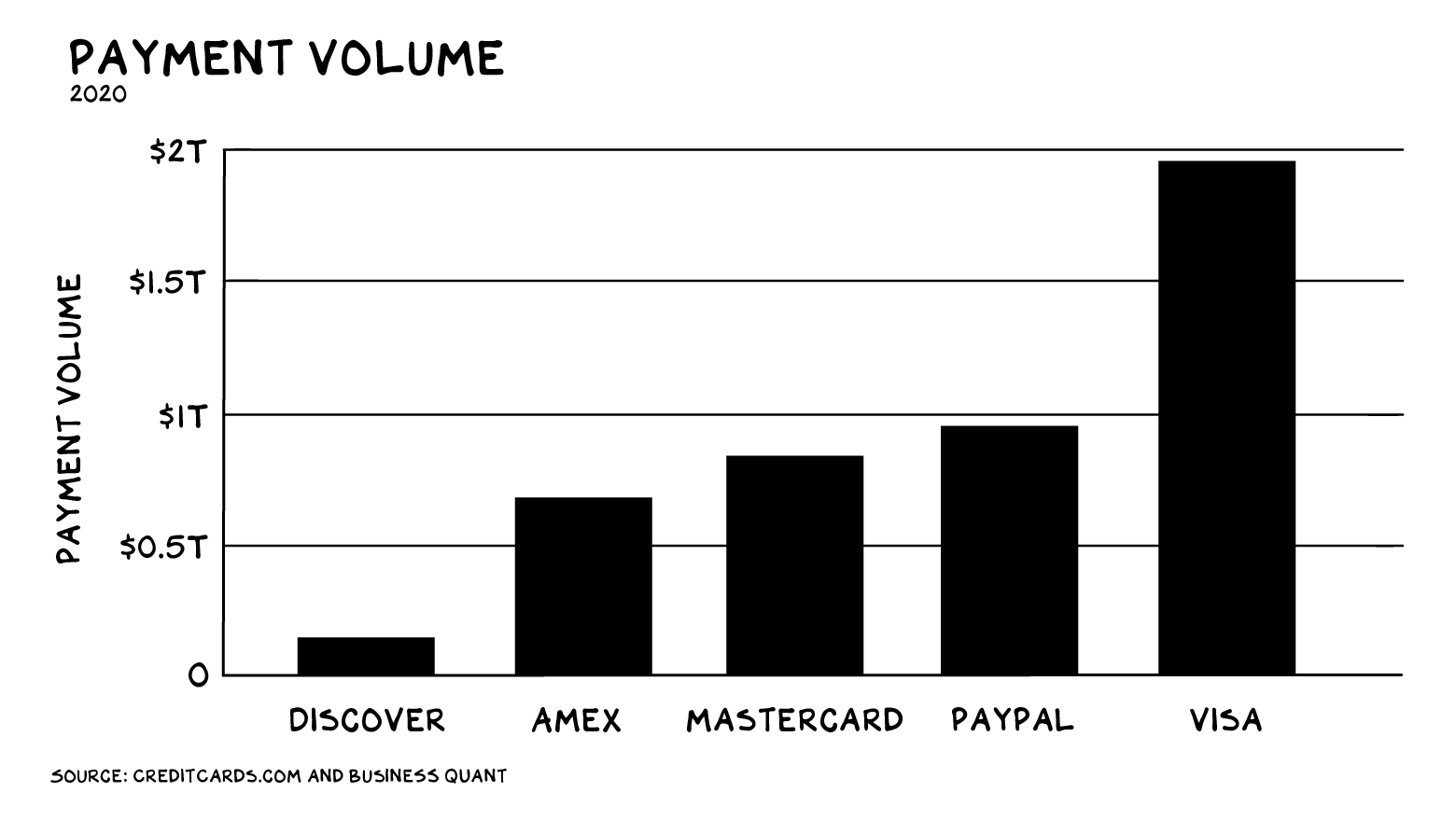

Unicorns are also coming for payments. The megasaurus in this space is PayPal, which has built the first global payments platform outside the credit card model and is second only to Visa in payment volume and revenue. Square’s Cash app is capturing share, and Apple Cash is also a player, as it’s … Apple.

Square, Apple, and a host of other companies are taking the “partnership” approach, bolting new services onto the existing transaction infrastructure. Square’s little white box is a low-upfront-cost way for a small merchant to accept credit cards. It’s particularly interesting that Apple teamed up with Goldman Sachs instead of a traditional bank. Goldman is looking to get into the consumer space (see Marcus), and Apple is looking to get into the payments space — this alliance could be the unsullied fighting with air cover from dragons. It should make Wells and BofA anxious.

The Big Four credit card system operators (Visa, MasterCard, Discover, and American Express) are still the dominant payment players, and they have deep moats. Their brands are global, their networks robust. Visa can handle 76,000 transactions per second in 160 currencies, and as of this week it had settled $1 billion in cryptocurrency transactions.

Still, even the king of payments sees dead people. In 2020, Visa tried to buy Plaid for $5.3 billion. Plaid currently helps connect existing payments providers (i.e. banks) to finance software such as Quicken and Mint. But it plans to expand from that beachhead into offering a full-fledged payments system. Visa CEO Al Kelly initially described the deal as an “insurance policy” to neutralize a “threat to our important U.S. debit business.” In an encouraging sign that American antitrust authorities are stirring, the Department of Justice filed suit to block the merger, and Visa walked.

Beyond Banking

Fintech is also coming for investing with online trading apps (Robinhood, Webull, Public, and several of the neobanks) and through the crypto side door (Coinbase, Gemini, Binance). Insurance is under threat from companies like Lemonade (home), Ladder (life), and Root (auto).

In sum, fintech is likely as underhyped as space is overhyped. Why? The ROI on your professional efforts and investing are inversely proportional to how sexy the industry/investment is, and fintech is … boring. Except for the immense opportunity and value creation — for multiple stakeholders. “Half the world is unbanked, but we need to colonize Mars,” said no rational investor ever.

Re investing in fintech: What has, and will always be, a good rap? The guy/gal who owns the bank.

Life is so rich,

P.S. This fall, I’m sharing my decades of experience building up, working with, and understanding the world’s best brands through my edtech start-up, Section4. Join me to learn about Brand and Strategy.

45 Comments

Need more Scott in your life?

The Prof G Markets Pod now has a newsletter edition. Sign up here to receive it every Monday. What a thrill.

Interesting article, as always. What this overlooked however is the financial model of banks. They take in deposits (liabilities) and pay some interest on them. Then they lend that money out in loans (assets) at higher level interest rates than they pay on deposits. The margin between those rates is where most bank revenue comes from. The unbanked and underbanked don’t have much to deposit, and usually don’t qualify for loans. This makes them undesirable and unprofitable customers for most banks that are not using VC money to subsidize client growth.

You should cover the Indian UPI traffic, that has its own critical mass. Its helping a lot of unbanked, bank!

Dear sir

We have respect and we have now which the mony yet looking transfer Islamic bank account no 20501940100213512 branch thakurgaon Bangladesh .we have request kindly if is true your fund then can direct transfer Islamic bank account above the bank.please since money is not transfer then my have/we have cannot received take fund implemented Nabajug Unnayan Sangstha thakurgaon Bangladesh.

Thank you for regards

Your faithfully

Bijoy kumar sarker

Nabajug Unnayan Sangstha

Thakurgaon Bangladesh.

Hi Prof G, as always amazing clarity in your writing and great podcast. While I agree with many of your points, when it comes to FinTech vs Traditional banks it’s definitely worth pointing out that offering a much higher interest rate or vastly enhanced UX doesn’t make for a sustainable competitive advantage – it’s simply VC subsidised user acquisition. Banks could relatively easily offer these features and rates but know it is not sustainable nor profit making – which is why you see many of these features and offers rolled back to be in line with traditional banks the moment the new players gain scale. The same happens with their level of digital support offered (great in the beginning and equal if not worse post scale).

This isn’t only true in FinTech but also in many VC heavy models such as Uber (now more expensive than cabs) and AirBnB (with cleaning fees and insurance making booking more expensive than hotels)

I agree with most of what the author said. Big banks are ignoring the needs of the smaller (ie, non-upper or upper-middle-class) families and businesses. This is also on top of the fact we’re being priced out of the housing market and many other markets, as well.

Big banks would like to pretend we don’t exist, even if we’re making above-average incomes and are otherwise excellent bank customers.

I also understand the problems with unbanked and under-banked, especially in terms of the fees and lack of representation these banks give the working classes, but…

It should also be noted that the “neobanks” offer no way of depositing cash, which is something many people still need to have done. (Think of those who wait tables, are in other service industry professions, or are too poor and/or otherwise unable to take credit card payments.)

Praising PayPal in terms of its lending–while ignoring the fact it’s an aggregator that has been sued and otherwise engaged in some Very Unethical business practices–sells short the other points the author was trying to make. (Square is also an aggregator that has faced similar problems. As someone who works in fintech, I see these from our clients.)

Both Square and PayPal can go after these smaller clients entirely because they are often predatory in their practices. They are countless instances of both freezing their clients’ account with little or no warning, charging outrageous fees for transactions, or finding excuses to avoid promptly giving their clients money that is due.

Fintech is on the cutting edge of how payments are accepted because we know that the payment industry–being driven by working-class people–is constantly evolving. The pandemic only rushed certain trends. As more business is not being done face-to-face and as cash is becoming used less often (expected to be less than 4% of all IN-PERSON transactions over the next 4 years), we have to make banking accessible to the masses.

PayPal froze my account and banned me from using their service and I simply asked them a question. Then they wouldn’t let me close the account so I could delete or protect my credit card information. They smugly told me, “Read your membership agreement” and then hung up on me. The rich really do make the rules.

I believe the US market is huge but also take a dive at the European market as they also have HUGE players like Adyen (much more integrated and offer something better than Square or Stripe) who are total disruptors to the status quo.

When you say the traditional banks face zero credit risk do you imply that the FDIC backstopping bad loans is not risk?

What world do you live in… I like my banking institutions to be responsible with money not social justice warriors, these startups are welcome to do what they will with their money as long as they are not underwritten by the government.

This was referring to PPP loans. All PPP loans were guaranteed by the government.

It’s fun watching old guard companies with mahogany board rooms commit suicide trying to placate shareholders by increasing sales and profit by exploiting their customers. After all, what is a customer but a target! Come on Fintech, Edtech, Medtech, Insurtech! What’s the worst that can happen – you’re acquired to neutralize the threat? At best you make even more by democratizing (there’s that word again) stuff that’s narrowed the focus to targeting the top 10%!

Hello Professor Galloway,

I’d love to hear your thoughts on last night’s Frontline episode about the Fed and QE.

I would so like to join in that point of view re last night’s Frontline prg.

Great article Scott, I find tremendous value in your posts, blogs, and YouTube videos. Thank you very much for your work.

Hope you’re enjoying Iceland still Scott. I drove round it a few years back with my teenage boys – stunning place. Are you calling in to London before heading back?

Fintech has been the flavour of the month here in Australia for a few years, but the big 4 banks here (like your Chase and Wells Fargo) are fleecing the tiny population dry with outrageous banking fees. Neobanks have not managed to cut through – the big 4 cartel banks even managed to keep Apple Pay off of our phones for nearly 2 years. Even with a banking license, Neobank Xinja completely failed because they did not offer credit (read credit cards). Interestingly, Xinja could not “afford” to pay interest to the few who chose to use the service. The banks here are funded by debt + outrageous fees for basic services including ATMs. Yes we wake up in 1985 every single day. Australians are deeply in debt – home loans and credit cards – way more than our US counterparts. Out of this cesspit – Afterpay emerges. No surprise for its popularity in US.

Xinja probably not a good example. Bad management from the start, went from bad to worse when they started believing their own hype.

What fintechs in Oz are hindered by is the amount of regulation and red tape. The regulators did try and make it easier with the use of a reg tech sandbox but even this isn’t without its headaches as is the limited banking licences.

Open banking should’ve been the panacea to some of those woes but again the Big 4 banks made a mess of that…where’s that timeline again? Also have a look as to who is heading these “new” neo banks. Majority of the time they are all ex-big 4 bankers with an axe to grind and the usual connections – looking at you Judo Bank!

Then there is also the fact that the Big 4 in Oz are also scooping up all this new “innovation” by creating their own “fintech” subsidiaries or “innovation labs”.

The one surprise fintech making a go of it in Oz is Up Bank but even then their stymied by having to rely on a major bank for their licence.

Nevertheless it’s an interesting field and hopefully it can only lead to better competition and better consumer outcomes.

Good read – although I’m surprised to not hear about Stripe in this – and they are so much more than “Payment Infrastructure for the Internet”

Great insights on the peripherals of finance/banking. Thank you Prof SG.

Can please any one inbox on finding sustainable ways of raising finance/capital to expand an already existing business? I’m an educationist and school owner here in Zambia Central Africa. Out school Proed Academy provides much needed educational and feeding services from Pregrade-Olevels but we can only reach a fraction of people due limited funds. Any help on the raising the funds to cater for educational needs in underserved communities will be welcomed. Please inbox me.

info.proedacademy@gmail.com

While DeFi rapidly recreates the complexity, confusion and risk inherent in the existing model, others are seeking Neo, or Narrow Banking, just an account and a payment rail.

As usual Scott provides more insight into everything than most degrees in a 5 minute read

could the US post office be of help here? If allowed to.

For some background, I am a Covid divorce collateral damage. My ex and I had enough and because we are financially secure, had a very civil exit. But now at 54 year old, been in the marketing business for 30+ years years, how can a “semi exec”(director level) find the inspiration to get him or her self motviated into marketing. Since COVID all I can think about is retirement. Lucky to have worked as a marketing slave in product/digital marketing for S&P 500 global companies, (ex Disney, Yahoo, Campbell, Heinz, Fin Tech) and now out of inspiration, void of drive, and really finding underappreciated as a marketer???? What is the path or path(s) or fresh new ideas to monetize my 30+ years of experience. Are there new avenure or role or industries I can monetize my talent. Curious…

You can start a blog, YouTube channel, and monetize your knowledge in this field.

The concepts “businesses that help communities thrive should themselves thrive” and “an informed customer is our best customer,” are, unfortunately, not closely held principles in many companies.

They are to us. We’re building a FinTech on it. We’re looking for a few good banks committed to those same principles to demonstrate their potential.

Scott, we hope to show you strong examples to the contrary … they’re out there!

Thank you for your good work.

Just wanted to say thank you to Professor Scott Galloway. I am about to turn 40 and am from a bible belted and financially strapped (east TN) part of the this incredible country and with limited access to education and insight (hi speed internet still can’t broadcast through mountains lol) to the financial mkts of the world, like Prometheus you have and continue to bring fire to the people. And for doing so, I thank you.

~Artis

What about access to affordable credit in America? Over 75m people in the U.S. use 400%+ APR short term loans to finance their daily lives because they don’t have access to mainstream financial services! Because this person typically runs out of money on the 20-24th day of the month, s/he then resorts to predatory lenders (Payday, Title, Pawn, Checkcasher, etc.) that charge ridiculous rates and fees for access to quick cash. Research from PEW, the CFPB, the FDIC, Mehrsa Baradaran, and so many others shows these predatory lenders trap LMI consumers in a debt spiral that almost impossible to escape.

For generations, communities of color have been excluded from mainstream financial services, opening the door for the short term predatory lenders that cause economic blight and social inequity.

I’d love to understand how you @profgalloway (or anyone reading this) see this systemic problem being solved!

Feel free to email me at gjwilliamson14@gmail.

Great article. Another interesting juxtaposition is the big banks’ attempt to enter the P2P space by creating the consortium Zelle. I’m sure Prof G you have plenty to add about this approach in trying to answer the meteoric rise of Venmo. One of the telling metrics is the level of engagement when you compare monthly transactions to that of the average Venmo user to the Zelle user, which I believe is approaching 5X.

Zelle is whipped cream on sh*t. Everyone using it has a bank account & is not adroit enough to see how it doesn’t address the unbanked market in the US or elsewhere.

It is hilarious how the disingenuous Jamie Dimon cries about Fintech, saying they aren’t regulated. They are regulated 50 state DFIs and the CFPB. He is only really accountable to the OCC and FDIC. He can tell the CFPB to bite him. The biggest scam in the US is that Visa and MC require you to be an FDIC bank to issue a card. That is the scam.

Prof G – you’re my hero in all things marketing and strategy, but how can we have a serious conversation about the future of banking without talking about DeFi? Do you really think capital markets will still characterized by centralized authorities, custodians and intermediaries by the time my tall sbx costs $5?

Good stuff. Big and regional banks are pretty well hostile to startups, especially with non US resident founders. They hide behind the Beneficial Ownership clause stemming from the Patriot Act saying >50% equity needs to be US resident or resident alien. I’ve had Chase and Capital One insisting that both UK founders be present to open an account in complete oblivion of the COVID travel restrictions! Took ~2 days to open an account with Mercury Bank. However, online banks are v barebones and there is concern that they you are placing money into a seemingly black hole.

Totally agree Fintech is disrupting the market but I do like a brick and mortar when there are issues. Nice to speak with someone in person and know my deposits are safe with a reputable bank. Concerned Dave and other fintech start ups could go belly up and I would lose my deposit. Love Prof G though and everything you write about.

Right on, Professor. Last week, Citi Bank, which has a goodly amount of my money (7 figures worth), advised me that my investments there were not enough to stay in my current private banking group (as the new minimum is now $25 million, more than they have of my money), and in addition they were raising the fee to manage my portfolio from 50 (basis points) to 100, double the price. I told them I thought their business model was poor. Instead of funding their clients, or new prospective clients, with loans to buy businesses or properties, they are raising fees, hosting endless gigs for exclusive clients that I have no interest in attending (or funding), and paying the folks in their management groups huge salaries to do nothing much at all, customer-wise. Instead, they are selling obscure products that no one can understand (the latest being ‘structured notes’, which not even my accountant could understand, even after a zoom on the subject). I will move elsewhere, of course, but it seems a shame that a major bank doesn’t really get it, and the fact that their stock is down no surprise. My nephew in Fintech went public via a SPAC last week, so I suppose eventually we will all be moving our funds online to these sorts of companies, though I must say I am satisfied with Vanguard’s business model: low key, low fees, and owned by its shareholders.

Very interesting, professor.. What are the most perspective fintech companies from your point of view?

My main objection to fintech is lack of supervision and deposit insurance.

Its all fun and games till someone puts out an eye.

Home equity loan? Why you looking at Controller.com?

I tend to agree. I would look at the like of CreditKarma – they have a whole picture of consumers financial wellness…they are positioned well.

Yeah, CK is good at being the “Kayak” or “Expedia” of financial tools but doesn’t move the needle when it comes to actually advancing financial inclusion or expanding financial mobility.

Check out this fintech called Otto (https://ottocredit.io). They seem to be going about it the right way and will move the needle when they launch.

Stunning disregard for non-local effects is central to the fecundity of “disruptive” innovations by which venture capitalists ensure Scott won’t ever need to resort to little blue pills. Plllleease … Trump’s over leveraging the economy via tax cuts differs only in that it is more easily observable. Is there no self-interested limit to ever greater velocity of money just as soon as it can be accomplish (i.e., is there wisdom in wielding the ability to that purpose)? Hezbollah and other criminally minded actors in Russia and beyond are hoping the world bankrolls more FinTech innovations, much as home builders delighted in Barney Frank and Chris Dodd’s perfidy on our behalf, of too distant memory for too many to fathom. Seriously, “in the right measure” please … cannot rail against the next generations’ difficulties accumulating wealth without understanding root causes …

Your fixation to ridicule Elon Musk at every opportunity makes you look envious and petty, you are so much smarter than that. The day you can put together a mass car manufacturing business and a reusable rocket company then you will understand what it is to walk in his shoes. However, I do enjoy your articles.

Having worked for the second biggest lender in the US for several years, I can tell you that this is an oversimplification. There are lots of regulations for conforming loans and there aren’t easy ways to streamline the process of checking all the boxes since they require input from so many different places.

I just got denied for a refinance despite having more than a million in equity and enough money in my bank account to pay off the loan in cash. This is just the price we pay for a secure banking system that will prevent another mortgage crisis. What the CFCB has done may be a hassle for you and me but it will keep the predatory mortgage business from sinking our economy as long as these regulations are in place.

You can thank Countrywide.

Assets have very little to do with lending, as real estate loans are normally non-recourse. They can’t take your money if you don’t pay. They can only take the house. If a non secured loan, they have to sue you if you don’t pay. Too much hassle.

Peter, I agree. Scott, great article, as always…BUT…in addition to Peter’s comments that the big banks are handcuffed in so many ways, the disruptive fintechs almost ALL lose money right now. They are simply funded by unlimited VC dollars for years, losing gobs of dollars, and then they go public and make the VC’s rich, while the “little guy” buys the stock at IPO and eventually loses a bundle. Meanwhile, the big banks aren’t allowed to lose money for so many reasons. The VC game is, to a large degree, a scam on the little guy. Of course, a few startups hit it big (i.e. paypal), but for the most part, many of the hot fintechs today will crash and burn in a few years.

Yesterday, Wells Fargo announced they will be getting out of the unsecured line of credit business after they and others stopped giving out home equity LOC’s last year.

Perhaps they are concerned that the risk of these loans is not worth taking. Will these consumers be able to service their debt when Gov’t stimmy $ dries up and rent/student loan payments resume? Broadly household savings rates seem to be doing very well, but perhaps within the data traditional lenders are able to see just how vulnerable a portion of their cliental seeking credit actually are? Maybe SOFI and other fintechs will gain these clients, but it may come at their own peril.

The old guards of banking were villainized (rightfully so) for their indiscriminate lending practices that led to the GFC. Only time will tell if we are at the point of time when fintech takes the lead or hangs itself. Potentially through loan loses and indiscriminate lending practices more in line with predatory lending to people lacking financial literacy than the democratization of banking.

We shall see

Hey Javier, I really enjoyed your thoughtful comment. You seem to have a good pulse for the current market (traditional and fintech). What is your professional background? I run a fintech that provides affordable and accessible credit to underserved communities and am interested in speaking with you.

John, Thank you for the kind words. I am probably not qualified to help you as I am a tradesperson by profession. Albeit with an interest in investing, macro trends, and an amateur student of history.

To quote Mark Twain “A banker is a fellow who lends you his umbrella when the sun is shining, but wants it back the minute it begins to rain.”

I have no doubt that there are many underserved by the big banks. Some because they are “too risky” well others just not profitable enough to bother.

My hope is that those that serve these people do not set the game up to be a lose-lose. Giving someone a small loan and a chance at a more prosperous life is great. Lending for more risky ventures to those that may not be able to understand the repercussions of a business failure can be disastrous for all parties involved. Best of luck