The Epstein Tax

The Epstein Tax

Audio Recording by George Hahn

America’s greatest asset is its optimism — an attitude that’s unleashed unparalleled wealth and validated the thesis that anyone can achieve the American dream. But here’s the glitch in the matrix: Capitalism is the belief that there should be winners and losers, that incentives drive innovation and prosperity. And they do. But the gilded few amass power and use that power for regulatory capture to expand their wealth … a lot.

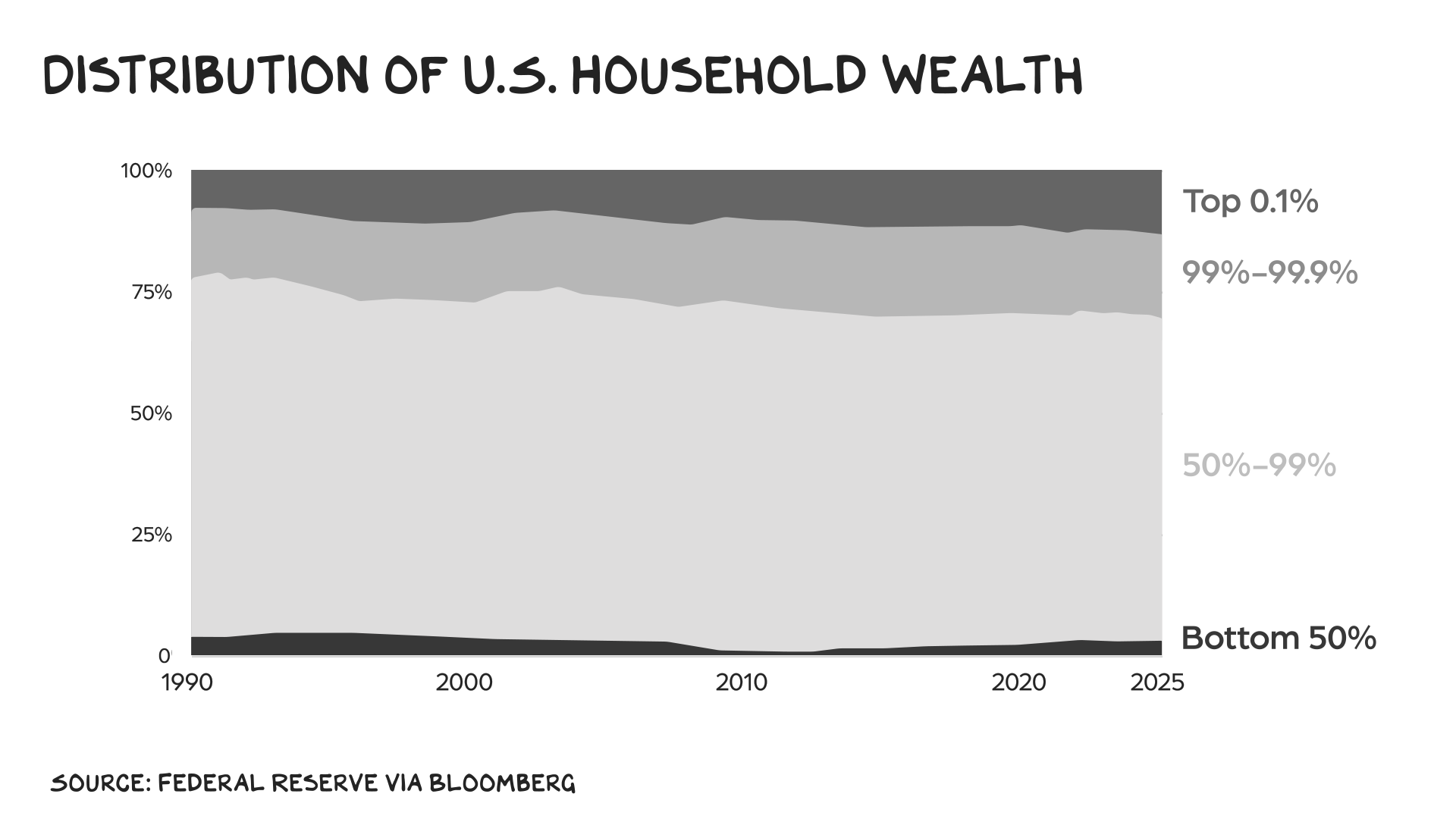

The Gini coefficient is a measure of inequality popular among economists. Zero indicates everyone in a society has the same; a score of 1.0 means one individual owns everything. In the U.S., we’re higher than 0.8 — about the level seen when the French were separating people from their heads. The superwealthy have amassed vast fortunes without fear of mobs arriving with pitchforks. U.S. policies, turbo-charged by a 2010 Supreme Court ruling that opened the gates to unlimited spending on elections, have widened the gap between the haves and the have-nots. As wealth concentrates, billionaire political spending rises higher, securing policy outcomes that further concentrate wealth. The chaser is inflation, which transfers still more wealth from earners, whose purchasing power erodes, to owners, who are insulated.

A reckoning is underway, ignited by the mountain of Epstein documents, which are giving the public a window into the rarefied world where the 0.01% are protected by the law but not bound by it, while the rest of us are bound by the law but not protected by it. Among hundreds of names appearing in the files are three of the nation’s best-known billionaires: Donald Trump, Elon Musk, and Bill Gates. Americans are fed up, not just with the depravity of some people in the Epstein class, but also with the massive wealth they continue to accumulate while the working class struggles. We aren’t talking about beheadings today, but modern-day guillotines are on the way: shame and taxes.

$2 Trillion

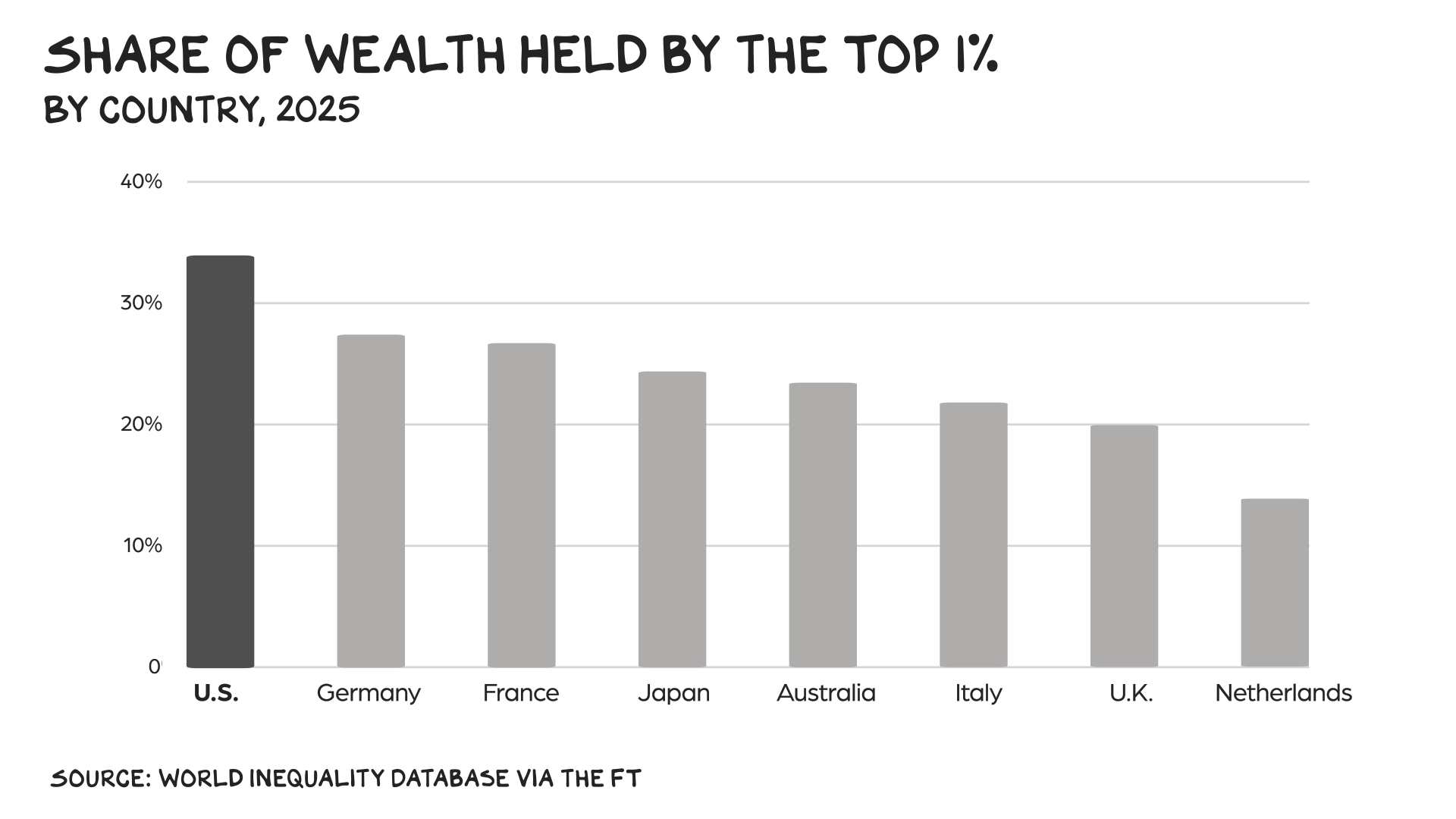

The top 1% control almost one-third of the nation’s wealth, their biggest share since World War II. The top 0.1% increased their wealth by 40% in the last three years. But UC Berkeley researchers say the top 400 paid only an estimated 23.8% of their income in taxes from 2018 to 2020 — a smaller percentage than the average American — down from 30% between 2010 to 2017. It’s not just an American phenomenon. Last year, the world’s 500 richest people added more than $2 trillion to their collective net worth, according to the Bloomberg Billionaires Index.

Governments around the world are putting the rich on notice, hoping to address this disparity, plug fiscal holes, raise money for defense, and address the challenge of aging populations. A few examples:

- In California, a proposed tax on billionaires would require those with a net worth above $1.1 billion to pay a one-time tax equal to 5% of their assets.

- New York City Mayor Zohran Mamdani has called for a 2 percentage point increase in income taxes on people earning more than $1 million a year.

- U.K. Chancellor Rachel Reeves used the budget to shift some of the burden onto wealthier people, targeting higher-value property and investment income.

- In France, left-leaning parties unsuccessfully pushed for a tax that would have required people with fortunes of more than €100 million to pay a minimum tax of 2% annually on their assets. Narrower measures were enacted instead.

Revolution

Wealth taxes are a tempting way to tackle inequality. They’re also an obvious means of raising revenue. In America, $5 trillion of receipts and $7 trillion in spending is (again) a transfer of wealth from earners to owners, as it’s inflationary. This isn’t sustainable. Fiscal strain in the U.K. prompted 30 economists to sign an open letter calling for a wealth tax to raise tens of billions of pounds. Voters also like this idea: Three quarters of British adults backed the idea of a 2% tax on wealth above £10 million.

But there’s a problem; wealth taxes don’t work. In 1990 a dozen OECD countries had wealth taxes. By last year, only three remained, in Norway, Spain, and Switzerland. Most of the measures collected little revenue and failed to meet their goals, sparking concerns they could stifle innovation and growth. In some cases, the superrich packed their bags and fled.

If the megawealthy don’t leave the country, they’ll deploy accountants and lawyers to value their assets at 40% of what tax authorities believe they’re worth. How are you going to value a stake in a small business? If you don’t have the cash sitting in your bank account, will you have to sell assets to pay your bill? Wealth taxes in the U.S. would also face challenges on constitutional grounds. Targeting people’s assets may violate private property laws while creating massive administrative complexity.

Capital vs. Sweat

Finding flaws in wealth taxes is easier than coming up with solutions. But there are commonsense ideas we should adopt to ensure the superrich and large corporations pay their fair share. One is tackling the carried-interest loophole, which allows private equity and venture capital managers to be taxed at the capital gains rate of 20%, well below the top rate of 37% for ordinary income. Taxing carried interest as ordinary income could raise about $15 billion over the next 10 years. That’s not a game changer, but it’s a start.

Capital isn’t more noble than sweat. There’s no reason someone should pay a 37% tax on their income while the wealthy pay much less when they sell stocks. In 2021 income from capital gains accounted for 39% of pretax income for the top 1%, compared with less than 1% for those in the bottom three quintiles.

Buy, Borrow, Die

If you want to climb into the upper echelons, follow a three-step strategy: Buy, borrow, die. While wages are taxed when they’re earned, assets are taxed when they’re sold. The wealthy often borrow against stock holdings and other assets, which grow more valuable over time, rather than selling them, deferring their tax liability. As long as interest rates are lower than the rate of return on the assets they hold, billionaires can spend more on houses, yachts, or even islands, while enjoying significant wealth appreciation. In 2011, a year in which Jeff Bezos was worth $18 billion, he reported so little income that he received a $4,000 child tax credit. Americans with more than $100 million of wealth held an estimated $8.5 trillion in unrealized capital gains in 2022.

One idea: When the rich borrow and use their assets as collateral, they should pay tax on the difference in the value of that stock or property between when they originally bought it and the day it’s pledged. Treating borrowing as a taxable event could raise more than $100 billion over a decade.

IRS Tax Gap

A hobbled IRS is a massive tax cut for rich individuals and large corporations, amounting to the most regressive tax in recent history. Auditing lower- and middle-income tax returns is easy; holding wealthy taxpayers with high-priced lawyers accountable requires a lot more resources. The tax gap, the difference between the amount of taxes owed and the amount collected on time, surged to almost $700 billion in 2022. Most of the taxes owed stem from underreporting of income by richer taxpayers.

An $80 billion increase in IRS funding planned under Biden’s Inflation Reduction Act (since rescinded) would have alleviated some of the pressure, netting more than $600 billion over a decade. Instead, the agency faces even more pain after losing more than a quarter of its workforce. If we want to move the needle on wealth inequality, strengthening IRS enforcement is critical.

Alternative Minimum Tax

In 1969, Congress learned that 155 taxpayers with incomes exceeding $200,000 had paid no federal income tax in 1966. So legislators created an early version of the alternative minimum tax, which essentially compares an individual’s income before and after they claim certain deductions and embrace all the loopholes. After a portion of their income is exempted, the taxpayer must pay tax on whichever amount is greater. Legislation in 2017 didn’t eliminate the tax, but it limited its scope, dropping the number of taxpayers affected from more than 5 million to 200,000.

We should have an individual AMT, with people above a $1 million threshold taxed at 40% and those over a $10 million threshold taxed at 60%. I estimate this could raise hundreds of billions per year, while only affecting the top 0.2%, or 275,000 taxpayers.

More Time With Family

As the tax debate heats up, billionaires inevitably start to focus on spending more time with their family — as long as they live in a low-tax state. In 2023, Bezos announced he was moving to Miami after almost three decades in Seattle to be close to his parents. His family must have used all the face time to persuade him to sell billions in stock in a state that doesn’t tax capital gains. In 2022, Washington state imposed a new 7% capital gains tax on sales of stocks or bonds of more than $250,000.

Boiling Point

Now Mark Zuckerberg is in the process of buying a property in Florida, triggering speculation that he’s unhappy about the proposed new tax on California billionaires. You think? The Meta CEO has benefited enormously from taxpayer-funded investments in education and infrastructure in the Golden State. If he wants to peace out to Florida, fine, but when he sells tens of billions of dollars in stock, he shouldn’t be able to escape tax on the massive wealth he accrued while living in California.

Billionaires can run, but they shouldn’t be able to hide.

We don’t need a revolution. We need a functioning IRS, capital gains taxed as income, and the death of the carried-interest loophole. The guillotine isn’t coming, the 1040 is. At a minimum, let’s stop pretending the system is broken by accident. It’s working exactly as designed — for those at the very top.

Life is so rich,

P.S. Kara Swisher and I are coming to Minneapolis. Catch the first ever Resist and Unsubscribe LIVE event, on March 8 at 7 p.m. at the Pantages Theater. Tickets are available here, with proceeds to benefit the Immigrant Law Center of Minnesota.

58 Comments

Scott Galloway

Professor of Marketing at NYU Stern School of Business and host of the Prof G and Pivot Podcasts. For Scott Galloway speaking inquiries, email speaking@profgmedia.com

Your discussion of income equality and the possible tax remedies was excellent, and we generally agree with your positions. In particular, you did a good job of identifying the “lowest hanging fruit” for raising taxes and improving equity, and also pointed out some of the pitfalls of the CA wealth tax proposal, etc.

One minor point….The Gini coefficient is a popular measure of inequality but we think that your comparison to the period of the French Revolution is a bit dramatic. We would argue that it is not the difference in income or wealth that makes people rise up and revolt, but instead it’s when a large portion of society cannot get their basic needs met, which we acknowledge is a point that we seem to be at or approaching. This inflection point could occur whether the Gini coefficient is .6 or .9. Regardless of the French Revolution hyperbole, I thought your Friday piece was great.

A recommendation….we think you would be more effective in making your points and certainly reach a wider audience if you would temper your political opinions and stick to economics and markets, areas in which you are quite good. Your political ranting (and salty language in your podcasts) sometimes distracts from your otherwise intelligent economic analysis.

Thanks for listening!

The IRS has been repeatedly hobbled by the GOP. Senators and Reps say they do it to prevent IRS “abuse” of taxpayers. But they really do it to allow key donors to evade taxes. The wild tax evasion now happening is in addition to the steady reduction of top marginal income tax rates over the last 45 years.

We need to reflect more on the Eisenhower years in the 1950’s. Although the individual tax rate for income above the top bracket was 90%, the economy flourished because workers were well paid and their spending drove up profits for business. We had a president who saw that a strong healthy nation required policies that steered a fair share of wealth to workers rather than to people who already were quite wealthy.

Work-at-home opportunities offer unmatched flexibility and a better work-life balance, but success isn’t automatic. It takes discipline, self-motivation, and strong time management. Want to learn how to make it work for you? Click here to discover the best way

to start——-——– come.ac/NetPay6

the poor stay poor, the rich get rich, that’s how it goes.

Scott – Talarico won the primary in Texas but needs your help to win the general. I find his message so compelling and it’s going to create an incredibly needed conversation about morality. But his economic message is practically non-existent and his net worth is listed as $170K. It is not enough as a Democrat to only talk about redistribution in a general election – there must be a balance between creation and redistribution. Like so many Ds, Talarico assumes that creation will always exist and his job will be to redistribute. But people in Texas (and the rest of the US) won’t trust someone who takes all of their hard work for granted and puts a ceiling on what they can achieve. Please go help him – Crockett would never had a chance to win the general but Talarico does. But he needs someone who actually understands business and economics to help him craft a modern Democratic message that embraces growth as well as redistribution.

A time of reckoning will come for the Epstein class. The more barriers they erect; the harsher it will be. I spent my peak earning years in the military (23 years) and I am angry as I watch my adult children struggle and worry about the future these greedy pricks are leaving for my grandchildren (17 – 1 years old).

Great commentary, Scott. You missed a large point – we have a spending problem. If the government taxed the 500 richest folks at 100%, we’d be able to fund the government for about two months. The wealthy are ok with taxes, but who spends it and how is the problem.

Generally, love the podcast as well as Raging Moderates, but have a question on one of the points discussed in this one. They mention the GINI coefficient for the US is around .8. But when I google search for US GINI, I don’t see anything reporting that. The data that I can find (Economist, OXFAM, World Bank…) all show US in the .4 to .5 range. Still in the very unequal range, but no where near the .8 that Scott refers to.

Great comments on wasteful government spending, oh that must have been another blog I read. Forgot, you’re the marketing guy….. Your solution is easy, just tax more that always works.

Without debating the right right rates for super wealthy, I don’t see how you can state that the average American pays a higher tax rate than the super wealthy (which you state is 23.8%).

See the simple analysis outlined below.

For a married couple filing jointly in 2026 with an income of $125,000, one child, and taking the standard deduction, the estimated federal income tax is $8,464. This results in an effective tax rate of approximately 6.77%.

Tax Calculation Breakdown (Tax Year 2026)

The following calculation uses the 2026 tax year parameters, which are reported on returns filed in 2027.

Adjusted Gross Income (AGI): $125,000

Standard Deduction: -$32,200 (for married filing jointly in 2026)

Taxable Income: $92,800 ($125,000 – $32,200)

2026 Marginal Tax Brackets (Married Filing Jointly)

Based on the taxable income of $92,800, the couple falls into the 12% marginal bracket.

10% on the first $24,800: $2,480

12% on the remaining $68,000 ($92,800 – $24,800): $8,160

Total Tax Liability (before credits): $10,640

Tax Credits

Child Tax Credit: -$2,200 (for one qualifying child under 17 in 2026)

Final Federal Tax Owed: $8,440 ($10,640 – $2,200)

Summary Table

Category Amount

Gross Income $125,000

Standard Deduction (2026) $32,200

Taxable Income $92,800

Total Tax (before credits) $10,640

Child Tax Credit (2026) $2,200

Estimated Total Federal Tax $8,440

Effective Tax Rate ~6.75%

There is also social security and Medicare tax of 7.65% that is paid on earned income ( 15.3%) if the person is self-employed. This is why the uber-wealthy pay themselves $1 of salary.

“The 0.01% are protected by the law but not bound by it, while the rest of us are bound by the law but not protected by it.” What a world to live in. Appreciate you so clearly and eloquently calling out what’s happening. Absolutely admirable, particularly knowing you would willingly and happily be affected by these changes for the greater good. Hats off to you, Scott. Keep going!

I love the idea of triggering a cost basis reset when stocks are used as collateral for borrowing (the massive loophole billionaires use today) which would then trigger a taxable event in the case of capital gains.

My question though is how to structure a rule such that it only impacts those billionaires looking to avoid taxes. For example, I know many investors trade on margin. In other words, they use the stocks they have in their portfolio as collateral for borrowing they use to then buy more stocks. This new rule would makes things get complicated quickly as investing accounts don’t grant cash when margin is enabled – rather there is some number they can buy up to based on the value of their portfolio.

There may also be the case where companies borrow money and use marketable securities on their balance sheet as collateral. They may be more looking to optimize their capital structure rather than specifically looking to avoid taxes. How would those be handled?

Good article. The inequality gap is our #1 problem along w growing national debt. Both parties seem to be avoiding both issues

Thanks so much for this fact-filled analysis. It’s high time that the billionaires are held accountable for paying their fair share of taxes. Please tackle, if you would, the issues of Board of Directors and compensation committees who are constantly funding more lucrative packages for execs that are getting crazy out-of-control. BoD members are all part of the corporate clubs that merely exist to pat friends on the back and pay them so that they can get paid a lot as well. Enough is enough.

Have you looked at the Tobin Tax. Introduced in 1972 by nobel laureate James Tobin. The idea being a tax of about .01% on currency transactions. Had the benefits of raising large amounts of revenue while curbing volatile currency markets. Would love to get your thougts.

It’s interesting to watch people that used to mock pizzagate now posting about Epstein.

It is not about giving more money to the government. It is about me getting more money before taxes. So it is about me having more freedom to make money and spend it efficiently. So sorry, Professor G, you bark the wrong tree.

Still, the data is, as always, well documented.

The Epstein files aren’t just exposing individuals—they’re exposing a system where the ultra‑wealthy operate by different rules. The documents show how deeply Epstein was connected to powerful figures like Trump, Musk, and Gates, even if they’re not accused of crimes. People are fed up with a world where the 0.01% are protected by the law but not bound by it, while everyone else is bound by the law but not protected by it. The reckoning won’t be violent—it’ll be public accountability, transparency, and tax policy catching up to decades of inequality.

Bless u Scott. You’re like a persistent drop of water falling. eventually it will create a stream and then hopefully it keeps growing in tools to use to create equality. We’re listening, hopefully people that make decisions will listen too.

Want to change tax policy? YOU have to vote. Contact your elected officials and demand an overhaul of the tax code. Canceling Amazon doesn’t change the tax code.

You have to make your voice heard and vote.

Instead, maybe fix the Fraud, Waste and Abuse of the Billions in Taxpayer $$$ flowing to States via Medicaid (Federal $) that don’t audit, manage or even hide the fact they steal the money for NGO’s, Maine Community Foundation and other fraud perpetrated by the Governor and her Liberal backed grift and pure theft of Billions. MN was just the iceberg. Really makes hard working taxpayers want to double down…Not! When will you academic liberals get serious about DOGE and create value instead of only zero sum games to extract from those creating wealth and the jobs the working class needs. This is why Dems are in trouble…

You could take all the billionaires wealth and still only fund the US government for less than a year. Houston, we have an enormous spending and fraud problem. There might even be overlap!

I would hope that the right and correct thing would be done.

Not sure how long this craziness is sustainable!

Maybe the revolution isn’t such a bad idea.

An excellent analysis, wide ranging, informative. Thank you …. but …

Many actually think there are going to be elections this fall?

Do you think the Republicans going to stand around and get wiped off the face of the Earth?

No they’re gonna have martial law and riot police and military and everything else.

Anything to stop these elections to keep them from getting wiped out

“We don’t need a revolution. We need a functioning IRS, capital gains taxed as income, and the death of the carried-interest loophole.”

Good luck with that, in today’s post Citizens United world, where we are now actively Gerrymandering out in the open, Congress will continue to enjoy their 80% re-election rate despite their sub 20% approval rate. As long as the vote is the only tool the population will put into action, why should they bother? They will vote to fixes you suggest about the same time they vote to cut their own salaries, end Citizens United, or abolish gerrymandering effectively. Maybe some shiny new guillotines will convince them to do otherwise.

Prof G,

Always a pleasure to read you and your team’s articles. They deal with the complexities and challenges of the issue, while offering constructive ideas on how to ameliorate those same problems.

I love that you also are taking a page out of Heather Cox Richardson’s playbook and providing some historical context around wealth disparity and tax evasion (love the GINI index comp for 1791). I make the same comparison myself adding 1848 and 1918.

Great stuff, and please keep it coming.

D

This array of solutions need to launch. Hopeful for midterm sensibilities

And Please billionaires – stop escaping taxes and moving to Florida…

P.S. Professor G, I give your Algebra of Happiness to young men throughout the year. 20 to date.

I missed the part where you went deep on cutting spending. Cut the spending, cut the spending, cut the spending. You and so many others bark at the moon about taxes, taxes, taxes. No appropriation should be passed without a legal/formal/stated method of its payment. All bills proposed should include a way to reduce spending associated with it by 10%/year. Businesses and families in our country cannot print money like our federal government! I challenge you to do better. This is C+ work at best. Your next email should show how we SIGNIFICANTLY reduce spending.

While most agree on cutting spending, the failed experiment that was DOGE, proved that the blanket statement of cutting spending is something of a farce. I welcome the argument, but as this article was specific on which areas to approach, Lets be more specific on where tangible cuts should be made.

I’m not opposed to any of Prof G’s suggestion but a better fix, to me, is to just raise the federal minimum wage. If the minimum wage had kept up with inflation then it would supposedly be over $12/hr instead of the current $7.25.

There’s just one problem, man: the pie didn’t stay fixed. It frigg’n exploded.

You know the “true” Gini isn’t a single number. You can’t cherry-pick the scariest wealth figure, blur it with income, invoke guillotines, and call it education dude. The French poor in 1789 lived in sh*t mud huts, ate moldy bread, owned one set of rags, and had zero ladders out. No safety net, no education, no mobility. Birth = destiny.

Today’s US households below the poverty line? Calories on demand, phones with the sum of human knowledge in their pocket, free public school, community college, military, trade programs, mentors, and a real shot at going from nothing to everything.

I know, because I lived it and in it. A10×50 trailer as a kid. Still in a (slightly nicer) trailer when I graduated high school. Enlisted, found mentors, worked hard, caught some luck, and chose to operate from abundance instead of resentment. Today I’m fortunate to be in the top 5%. Not because the system handed it to me, but because the system let me build it.

Imagine if young me had today’s you as a mentor — preaching scarcity, fixed pies, regulatory capture doom, and “modern guillotines.” Would I have even tried? Or would I have stayed a bitter and resentful young man in that trailer?

America’s greatest asset is still that optimism you opened with. The belief that the pie can keep growing and anyone can grab a bigger slice by creating value. It still is our choice.

“We need a functioning IRS, capital gains taxed as income, and the death of the carried-interest loophole.”

Scott – you keep making this statement, but it makes no sense due to redundancy. If capital gains are taxed as ordinary income, there is no such thing as “the carried-interest loophole” since the benefit of the loophole is to have what should be ordinary income taxed at long-term capital gain rates. The easy answer is to tax capital gains at the same rates as ordinary income (at which time carried interest is irrelevant) just like the tax code was structured after the tax reform act of 1986 under Reagan. Ironically, there was no preferential rate for capital gains under Reagan and Geoge HW Bush – the preferential long term capital gain rate was signed into law by Clinton, along with the repeal of the Glass-Steagall act. These two laws signed by Clinton account for much of the explosion of the wealth gap in the US.

Exactly go back to limits on money in politics. Lobbyist, PACs, etc have an outsized impact on policy and or deregulation

Also more equity could be realized with the elimination of stepped-up basis and other tax avoidance with inherited wealth..that could raise several hundreds of billions in tax revenue. Much of real wealth is never taxed!

Great work Prof G thank you for keeping us informed and focused.

This is not just a “wealth inequality” story. It’s a law and order story. The right has shown no signs that it is going to stop french-licking Mangorangutan’s back door. And the Dems are showing no signs of ceasing the enablement and averting their stare at Donald J. Himmler, Goebbels doppelganger Stephen Miller, and their band of scurvy men. Pretty much most of the institutions of record are on board, as well as a critical mass of the legal infrastructure, the military, corporations, etc. It’s going to take “A Mighty Wind” (h/t C. Guest) to bring this house of turds down, and I don’t see it happening. My guess is that, if the torch and pitchfork crowd ever get their act together, Trump will be given a villa somewhere that the law can’t touch him and everyone else will plead, “I VUS JUST FOLLOWINK OHR-DERS!” We need a modern-day Nuremberg tribunal in the Great Plains, then wall off Wyoming, lock them in, and hope for the Yellowstone caldera to blow. I do think we need a revolution, but it will be in the form of a national referendum; we need truth media to coalesce around some leadership; the sixty quintillion newsletters, blogs, podcasts, et al become white noise after a while and cancel each other out. The media has to extricate itself from the clutches of billionaires, and the laws have to be better written to do away with the on-purpose vagueness and “interpretation of what the forefathers meant” crapification.

Perfect post. Adds per comments below: (1) Cut spending! Particularly in the ‘War Department,’ the most wasteful and misguided use of money on the planet. (2) Eliminate the step-up in basis of estates on death. Also, don’t criticize Prof G for making suggestions that will increase his taxes by saying that he should voluntarily pay more now. We all should play by the set of rules; if the rules suck, change the rules; don’t play by another set.

Scott, are you paying your tax on long term gains at that 20%ish rate? If you think that is wrong, you can always voluntarily pay more to fix your “under-taxed” status. Be a leader and step up, and pay “the fair share you believe is rightful and that others should pay”. Walk your talk. Or are you one of them?

Agreed. this feels more like Scott wants to muddy the waters. WTF is the point of this? Its kind of a distraction from the problem

Approximately 47% to 54% of Democrats and Democratic-leaning independents believe they pay more than their fair share of taxes. As for the other half who don’t believe so, don’t expect them to be paying 1 penny more than they are obligated to.

Great article. Sane recommendations. Thank you for not locking your wisdom and insights behind a paywall

While I agree the ultra rich are under-taxed, I struggle with how to reconcile this with the irrefutable fact that the federal government is an often corrupt and careless steward of the finances they collect through taxes.

Apply progressive taxing to political donations. Exempt one standard deviation from the mean on the low end.

I like the ideas but don’t those proposals (bigger IRS, borrowing is taxable, and carried interest loophole) require changes at the federal level? NY and CA need changes that can be implemented at the state level.

Completely agree with your proposed policy changes with one addition. Eliminate the step up in basis at death, over a high threshold to minimize harm to small business owners and small farms. The games played to value an asset low to avoid taxes while alive than revalue the asset high after death to benefit one’s heirs needs to stop. Death is the one time a snapshot of an individual’s wealth or assets becomes available. Use the information.

T – you only get stepped up basis if the asst is included in the taxable estate. If the taxable estate is over the estate threshold, the taxpayer is already paying estate tax at a 40% rate. So the wealthy are not valuing the assets at a high level at death to enhance stepped up basis if they will otherwise pay a 40% tax on this higher value. Many articles insinuate that the wealthy (which I will define as those with taxable estates) somehow avoid paying estate taxes and get stepped up basis, but you only get stepped up basis if the asset is included in the taxable estate.

Add in the irony of Epstein’s supposed expertise in helping the super wealthy avoid taxes via his “consulting” services.

In a world awash in capital it no longer makes sense to tax income from capital at a fraction of the rate it taxes income from labor, and it isn’t just at the high income levels.

A married couple with $150,000 in income from wages and nothing else pays $27,703 in federal taxes. Their next-door neighbors with $150,000 in dividend income and nothing else pays $3,893 in federal taxes, or less than one seventh as much (at 2025 tax rates).

There’s a revolution brewing.

I’m a worker and I want my 5 points back.

From 1980 to now wages as % GDP fell from 65% to 60% while corp profits (owners take) doubled from 5-10%.

So workers struggle to pay bills while the owner’s stock market is on fire.

I want my 5 points back. Not complicated.

Better still get back the 10% inflation suffered under Joe Biden.

Agree, me too. It is not about giving more money to the government. It is about me getting more money before taxes.

I appreciate the policy focus here, but there’s a disconnect between the accountability you’re calling for and the silence around people in your own orbit.

You mention Trump, Musk, and Gates appearing in the Epstein files, then pivot to tax brackets. But Peter Attia (someone you’ve platformed on your podcast) appears 1,700 times in those same files. His emails with Epstein span 2014 to 2019, years after Epstein’s conviction, and include crude jokes and mentions of wanting to visit his island.

This matters because of what you’ve built your brand on: teaching young men better values. How do we reconcile that with publicly supporting someone who cultivated a friendship with a convicted sex offender for access to elite circles? Someone whose business model ($100K+ longevity packages) exclusively serves the ultra wealthy you’re arguing should pay more?

You write that “shame” as a modern guillotine only works if we’re willing to actually apply it. But selective accountability isn’t accountability. It’s just another way the powerful protect their own.

The tax solutions you propose are necessary. But if the shame you’re calling for doesn’t extend to people in your professional network when they’re implicated in the Epstein files, we’re not having an honest conversation about accountability.

Will you address Attia’s Epstein connections on Pivot or stop following him on Instagram?

Just to be clear, the US does have a wealth tax; it’s called property taxes (real estate taxes, ad valorem taxes).

1. If you own property directly, the value of that property is taxed annually; and, if you rent property then part of your rent goes to pay the owners’ property taxes.

2. The amount of your property taxes are the result of the assessed value which increases with the market and the property tax rate set by the local political authority.

Assessed value X property tax rate = property taxes

As you can imagine both assessed value adn the tax rate are fertile ground for mischief to increase total property taxes.

3. As the value of your property goes up — given the tax rate stays the same which it always does — then you property taxes also go up.

4. NYC — Mayor Mamdani is trying to increase NYC property taxes substantially to fund some of his fanciful programs — has not had a property tax rate increase since the 18.5% hike effective January 1, 2003 (under Mayor Michael Bloomberg), to address post-9/11 budget shortfalls.

Listening to you the last few months On Pivot and your podcast, I so appreciate your matter of fact analysis. The Epstein Tax resonated deeply with me and you articulate my deeper sense of what should happen…”We don’t need a revolution. We need a functioning IRS, capital gains taxed as income, and the death of the carried-interest loophole.” I am concerned the other may happen if we the American people are push too far.

What if we eliminate all the shelters and excuses, and tax everybody 13%. End of the year, we use it to grade Congress’ spending and if necessary raise it to 14%. Make all the accountants mad.

Work-at-home opportunities offer unmatched flexibility and a better work-life balance, but success isn’t automatic. It takes discipline, self-motivation, and strong time management. Want to learn how to make it work for you? Click here to discover the best way

to start——-——– ln.run/J_9ge